Introduction: Investors and the SDGs

This section:

- briefly describes what the SDGs are, how investors can contribute to the Goals and how the Goals can be useful to investors;

- explains how a focus on shaping outcomes in line with the SDGs, as outlined in this paper, differs from existing ESG incorporation approaches.

SDGs: The story so far

The 2030 Agenda for Sustainable Development was adopted on 25 September 2015 at the United Nations Sustainable Development Summit. The resulting Sustainable Development Goals (SDGs) established a globally accepted set of 17 overarching goals (underpinned by 169 specific targets, and 232 indicators by which they’ll be measured) for real-world outcomes in areas such water, health, poverty, gender equality and biodiversity (Figure 1).

The SDGs set expectations and track progress on key global issues. They build on other global agreements, such as in human rights, where the SDGs are grounded in the Universal Declaration on Human Rights, and on climate change, where the SDGs reference the United Nations Framework Convention on Climate Change (and progress against governments’ Paris Agreement commitments).

The SDGs set the global goals for society and all its stakeholders – including investors.

Figure 1: Sustainable Development Goals (SDGs)

What investors can bring to the SDGs

There has been some progress since the SDGs were agreed. According to the UN, extreme poverty and child mortality have fallen, and access to energy and decent work have increased. But as UN Secretary-General António Guterres says: “Overall, we are seriously off-track. Hunger is rising, half the world’s people lack basic education and essential healthcare, women face discrimination and disadvantage everywhere. One reason for the faltering progress is the lack of financing.”

There is a clear role for the financial system, and for signatories to the Principles for Responsible Investment (PRI).

The United Nations Conference on Trade and Development (UNCTAD) estimates that meeting the SDGs by 2030 will require US$5 trillion to US$7 trillion per year from the private sector. The financial system’s role in shaping outcomes in line with the SDGs cannot only involve new capital, it will require investors to redirect existing capital and be good stewards of the entities they invest in.

When the six Principles were established in 2006, the preamble stated that applying the Principles could better align investors to the “broader objectives of society”. In 2017 the PRI formalised the SDGs’ role in framing these societal objectives, committing to “enable real-world impact aligned with the SDGs”, and to contribute to “a prosperous world for all”.

What the SDGs can do for investors

Investors have long been focused on why environmental, social and governance (ESG) issues are relevant for their portfolios. From an initial focus from the mid-1980s on avoiding investments in activities that would cause harm or were deemed unethical, in the 2000s responsible investment emerged with a broader focus, taking in not only screening, but also sustainability themed investments and the integration of ESG factors into core investment decision-making processes (collectively known as “ESG incorporation”), alongside being active stewards of investees through engagement and voting.

However, expectations of investors from stakeholders – including beneficiaries, clients, governments and regulators – are shifting, driven by increased visibility and urgency around many issues – such as climate change, income inequality and human rights. The SDGs and the Paris Agreement demonstrate greater clarity from governments around their sustainability goals, and in turn the risks and opportunities created for investors, and the SDG-aligned outcomes that they can support. Several governments have also recognised that the SDGs can serve as a guide for responding to the COVID-19 pandemic: “Guided by the SDGs, we can redesign the power of community, society and global collaboration, to make sure that nobody is left behind.”

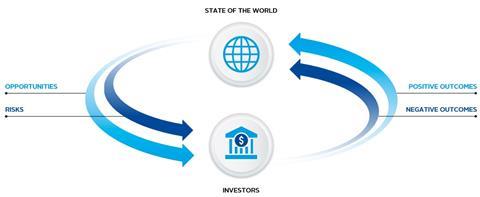

Focusing on SDG-aligned outcomes, including through collective action, can also feed back into portfolio performance, and into the resilience of the financial system itself. There is a continuous feedback cycle between (ESG) risks and opportunities and (SDG-aligned) outcomes: ESG issues create risks and opportunities for investors, whose actions shape outcomes on the world, which feed back into portfolios in the form of ESG risks and opportunities, and so on (Figure 2).

Figure 2: Continuous cycle of investors’ SDG outcomes, the resulting state of the world, and ESG investment risks and opportunities

This is particularly true for “universal owners” – large institutions that invest long-term in sufficiently diversified holdings across industries and asset classes that they effectively hold a slice of the overall market. For such investors, overall economic performance will influence the future value of their portfolios more than the performance of individual companies or sectors, incentivising them to support sustainable growth and well-functioning financial markets. A universal owner, and in turn their investment manager(s) and service provider(s), should view these goals holistically, seeking ways to reduce the company-level externalities that produce economy-wide losses, and ways to enhance positive, economy-wide outcomes. Further research is needed to understand if a focus on combining beta/macro/sectoral/cross-sectoral issues with shaping SDG outcomes reduces volatility and risks to economies, and leads to stronger risk-adjusted returns at the overall portfolio level.

In addition to understanding which potential financial risks and opportunities are likely to exist in (and in the transition to) an SDG-aligned world, a focus on SDG-related outcomes allows investors to:

- identify opportunities, such as through changes to business models, across supply chains and through new and expanded products and services;

- prepare for and respond to legal and regulatory developments, including those that may lead to asset stranding;

- protect their reputation and licence-to-operate (e.g. the trust of beneficiaries, clients and other stakeholders), particularly in the event of negative outcomes from investments;

- meet institutional commitments to global goals (including those based on client or beneficiaries’ preferences), and communicate on progress towards meeting those objectives;

- consider materiality over longer time horizons, to include transition risks, tail risks, financial system risks, etc.;

- minimise the negative outcomes and increase the positive outcomes of investments.

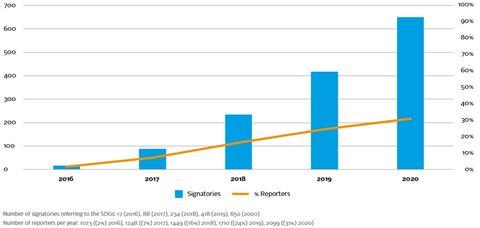

As a result, a substantial and growing number of investors, including PRI signatories, are now looking beyond how the outside world impacts their portfolios, and seeking to understand and shape their portfolios’ outcomes on the world. Many are doing this by making specific commitments to one or more of the SDGs (Figure 3).

Figure 3: Number of signatories (and percentage of reporters) mentioning SDGs in reporting to the PRI, 2016-2019

How a focus on SDG-aligned outcomes goes beyond ESG incorporation

Although the increasingly mainstream approaches of ESG incorporation may shape positive, real-world impact aligned with the SDGs, they do not get us as far as we need. (Even impact investing is limited, both due to being primarily focused on positive outcomes, and as it is typically implemented as a specific strategy in one part of the portfolio, rather than being used as a framework for shaping outcomes across the entire portfolio.)

A focus on shaping SDG outcomes involves broadening the approach from being an analysis of financially material ESG issues at an individual investee level, to also include a parallel analysis of the most important outcomes to society and the environment at a systems level (see Example: Clean water and sanitation below). These issues and outcomes overlap to some extent, but not fully, and this is part of the gap that needs to close to achieve the SDGs by 2030.

Further analysis and case studies are needed to understand how investors might:

- select the investment with outcomes best aligned to the SDGs, where financial returns between investment opportunities are equal;

- seek alternative sources of return (e.g. different asset classes and products) that can provide more SDGaligned outcomes, including through strategic asset allocation;

- focus on returns over a longer time horizon.

While some current legal and regulatory frameworks, and many modern fiduciary duties, require investors to consider how material ESG factors are incorporated into their investment decisions, most markets do not require investors to consider the reverse – how investment decisions affect ESG issues, nor the SDGs. Investors can engage companies, clients and beneficiaries on SDG outcomes to align investment mandates with contributing to the SDGs, as well as engage policy makers to align capital markets with contributing to the SDGs. A Legal Framework for Impact will explore how investors can manage their fiduciary duties and impact within existing legal frameworks.

Example: Clean water and sanitation

To illustrate the cycle of risks/opportunities and outcomes, we can look at an investor assessing an opportunity in a beverage company that produces water-intensive drinks and operates in a region under high water stress. The company sources water from a river basin that has been experiencing drought in the past two years, and there are other water users such as textile producers, farmers and local communities dependent on the water source.

If pursuing an ESG incorporation approach, an investor might only assess the immediate risks and conclude that the company has good governance systems, all the operating permits required, its products are in high demand and it has secured access to sufficient water sources. In this example, the investor takes the investment opportunity, which enables the company to continue or expand its production, causing further water stress and creating harmful effects on local communities and businesses. This in turn could create a feedback loop leading to a future investment risk – it could ultimately lead to increased CAPEX, OPEX, reputational risks and regulatory risks.

In an approach that also focuses on shaping real-world outcomes of the investment, this outcome on water stress would be something the investor assesses before it makes the investment decision and manages and monitors during the investment. In this case, understanding a specific SDG-related outcome not only contributes to the SDG of clean water and sanitation, it gives an early warning signal for a potential investment risk. The investor could still decide to make the investment, but engage the company with the aim of it becoming a net-zero user of water (i.e. adding the same amount of water back to the river basin as it is using), and engaging the regulator to better price water or to guarantee access for the communities within the basin.

Tightening regulation or rising water prices could also lead to this outcome-focused approach improving riskadjusted investment performance over time.

The following existing outcome metrics can be used (SASB FB-AB-140a): (1) total water withdrawn, (2) total water consumed, (3) percentage of both water withdrawn and water consumed in regions with High or Extremely High Baseline Water Stress.