The Paris Agreement and the Sustainable Development Goals (SDGs) will only be met if developed and emerging market stakeholders – such as governments, investors, multi-lateral organisations and local communities – work towards their advancement.

Although some progress has been made since 2015, a lack of financing remains a major barrier and it is most acute in emerging markets. The Organisation for Economic Cooperation and Development (OECD) estimates that there is a US$3.7trn[1] funding gap between the annual financing needed to meet the SDGs by 2030 and what is provided by current investment levels, with the COVID-19 pandemic creating additional capital needs and reducing existing funding.

Investors – including PRI signatories – can play a role in closing this gap by applying responsible investment approaches to their emerging market investments, such as ESG incorporation and considering sustainability outcomes, and by collaborating with local and international stakeholders.

Drivers and barriers to investment in emerging markets

Institutional investors choose to invest in emerging markets for several reasons, including:

- to gain exposure to growing economies;

- portfolio diversification;

- to have a real-world impact; and

- due to home bias.

Nonetheless, the funding gap indicates that there are significant barriers preventing greater investment flows.

Having a strong understanding of ESG factors and developing robust processes to assess how they apply in different contexts can help investors to overcome some of those barriers associated with emerging markets investing.

Some of the risks most cited – around political or social instability, or corruption, for example – stem from underlying issues such as inequality, health and safety, decent work, and gender disparities.

Investors with a strong grasp of these are therefore better placed to determine and manage the materiality of those risks in specific emerging markets, rather than relying on common (mis)perceptions to shape their positions.

This paper discusses how investors can apply responsible investment practices to manage risk and meet return objectives for clients and beneficiaries while working towards closing the funding gap. We consider the different roles that investors can play – from engaging with policy makers to working with investees.

Creating an enabling environment

Developing sustainable finance policy frameworks that can support climate and SDG-aligned capital markets is a core part of creating an environment that attracts and enables responsible investment.

Key challenges:

- The existence and implementation of sustainable finance policy frameworks varies widely between countries.

- ESG data provider coverage of emerging markets is weak.

Suggested actions:

- Institutional investors and multilateral institutions continue to engage with governments and local regulators on developing and implementing sustainable finance policy frameworks that align with the SDGs and the Paris Agreement.

- Standard setters, institutional investors, corporates and stock exchanges collaborate to improve capital market disclosure practices.

- Interested stakeholders collaborate to engage with ESG data providers to improve emerging markets data coverage and methodologies.

Asset allocation

While policy makers need to create an environment that enables responsible investment, asset owners can take steps to understand how their asset allocation decisions can support greater investments in emerging markets.

Key challenges:

- Asset owners can lack expertise to assess emerging market risks and opportunities.

- Sustainability outcomes and ESG factors are not widely considered in asset allocation.

- Mainstream and ESG index composition can be problematic for emerging markets, affecting asset allocation decisions.

Suggested actions:

- Support investment consultants and asset owners to develop strategic asset allocation frameworks that consider sustainability outcomes.

- Relevant stakeholders collaborate and engage with regulators, ESG data and index providers to expand emerging markets coverage and improve index and rating methodologies.

- Developed and emerging markets-based asset owners share their experiences to develop best practices.

Supply of investable opportunities

While asset owners often face constraints related to liquidity, regulations or a lack of expertise, there are investment products and structures – such as green/sustainable development bonds and blended finance – that can help them directly support key sustainability outcomes.

Key challenges:

- Accessing opportunities and bankable projects that:

- adhere to green/SDG standards;

- meet investors’ liquidity and risk constraints.

- Poor signposting of green/SDG investment opportunities.

- Not enough private capital mobilisation by multilateral development banks and other public institutions.

- Emerging markets-based managers face significant barriers to attracting commitments from institutional asset owners.

Suggested actions:

- Continue knowledge and capacity-building efforts to help institutional investors access:

- sustainable investment opportunities (such as green, social and sustainability bonds, blended finance);

- local partners, data and risk mitigation tools.

- Further align incentives between donors, development finance institutions and institutional investors.

- Investors seek out opportunities to participate in and/or support asset class-specific activities that aim to grow opportunities and capacity in emerging markets.

ESG incorporation and active ownership

Emerging markets investors apply responsible investment practices at the investee level to manage risks, unlock value and potentially generate more real-world impact than they can with many developed markets investments.

Key challenges:

- Cultural and structural differences in the understanding and application of active ownership.

- Insufficient local ESG and impact knowledge and experience, whether within the investment community or companies.

Suggested actions:

- Raise awareness about the different engagement approaches and how to identify critical sustainability issues in local contexts.

- International and local investors find opportunities to engage collaboratively, share information and develop best practice.

- Continue and enhance partnerships between development finance institutions and local emerging market partners (investors, government agencies, regulators etc) to provide ongoing technical support on responsible investment.

Next steps

Closing the funding gap while delivering return objectives in emerging markets requires investors, multilateral institutions, service providers and governments to take concerted, collaborative, long-term action across the areas discussed in this paper.

The PRI will assess how it can support such action by leading, facilitating or supporting relevant initiatives, particularly where greater collaboration between asset owners and investment managers is required.

The PRI would welcome feedback from signatories on the suggested actions and what we can do to support them as we look to further develop our work programmes in this area. Contact us at [email protected].

This paper has been developed in large part because of the significant shortfall in funding for the Sustainable Development Goals (SDGs) and climate change mitigation and adaptation in emerging markets.

Furthermore, it reflects our increasingly diverse signatory base (see Growing our relationship manager presence in emerging markets) and the focus on increasing support for responsible investment in emerging markets, as outlined in the Strategic Plan 2021-24.

The PRI aims to strengthen the responsible investment practices of local investors and support the development of sustainable capital markets; both are important building blocks for increasing flows of responsible capital to emerging markets. This paper is an initial response to that and lays the foundation for further work on responsible investment in emerging markets.

It has been informed by desk research, a review of key frameworks and guidance, and interviews with:

- developed and emerging markets-based asset owners and investment managers that invest in emerging markets; and

- development finance institutions and other stakeholders.

Defining emerging markets

There are various definitions used to classify emerging, or developing, and developed economies.[2]

This paper uses theInternational Monetary Fund’s classification of emerging and developing economies, which can be found in the Appendix. When the terms emerging markets or developing countries are used by organisations other than the IMF, we refer to their classifications.

The countries classified as emerging vary significantly across a range of factors, including historical and political trajectories, geographic location, population size and GDP. As a result, when highlighting examples of responsible investment practices, the paper necessarily makes generalisations that do not capture country-specific nuances.

Growing our relationship manager presence in emerging markets

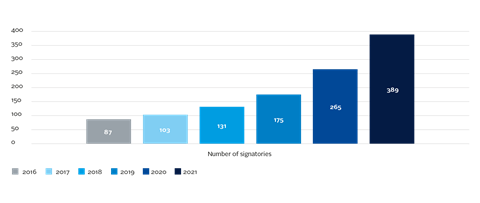

The number of PRI signatories based in emerging market countries has more than tripled in the last five years, growing from 87 in June 2016 to 389 as of June 2021.[3] To ensure these signatories are supported, we have expanded our local signatory relations coverage and now have representation in Colombia, Brazil, China, and South Africa.

Emerging market signatories to the PRI, June 2016 - June 2021

Why emerging markets matter to responsible investors

Key takeaways

- The Paris Agreement and the Sustainable Development Goals will only be met if developed and emerging market stakeholders work towards their advancement.

- Although some progress has been made, a lack of financing remains a major barrier. Investors can play a role in closing this funding gap by applying responsible investment approaches to their emerging market investments and collaborating with local and international stakeholders.

- Investors choose to invest in emerging markets for several reasons, including to gain exposure to growing economies; portfolio diversification and to have an impact.

- There are significant barriers preventing greater investment, including benchmark composition and construction; smaller capital markets and opportunity sets; risk perceptions; lack of data and expertise.

The Paris Agreement and the Sustainable Development Goals (SDGs) will only be met if developed and emerging market stakeholders – such as governments, investors, multi-lateral organisations and local communities – work towards their advancement.

Although some progress has been made since 2015, a lack of financing remains a major barrier and it is most acute in emerging markets.

Investors – including PRI signatories – can play a role in closing this gap by applying responsible investment approaches to their emerging market investments, such as ESG incorporation and considering sustainability outcomes, and by collaborating with local and international stakeholders.

PRI resources on the SDGs

Established as part of the 2030 Agenda for Sustainable Development, the SDGs set the global goals for society and all its stakeholders – including investors. The SDG Investment Case, published in 2017, explains why the SDGs are relevant to investors, why there is an expectation that they will contribute and why they should want to. Investing with SDG outcomes: A five-part framework outlines a prospective framework for action for any investor looking to shape real-world outcomes in line with the SDGs.

The UN Conference on Trade and Development (UNCTAD) estimated in 2014 that US$5trn – US$7trn was needed globally every year from 2015 – 2030 to finance the SDGs, of which US$3.5trn – US$4.5trn would be in emerging markets.

Investment levels at the time left an annual US$2.5trn gap. This has since widened by 50% to US$3.7trn[4], with the COVID-19 pandemic creating additional capital needs and reducing existing funding. For example, greenfield investment in a number of SDG-relevant sectors is now 20% below 2015 levels, according to UNCTAD.

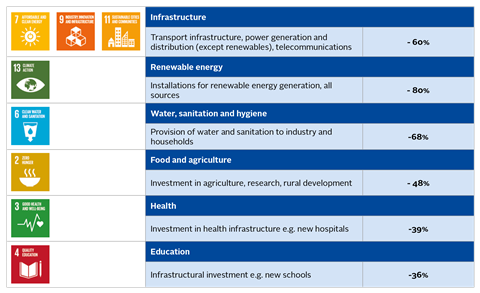

Figure 1 highlights the sectors where the annual SDG investment gap in emerging markets is greatest.

Figure 1: The impact of COVID-19 on investment in the SDGs. Source: UNCTAD SDG Investment Trends Monitor (2021)

Furthermore, a 2021 report by the Grantham Research Institute on Climate Change and the Environment, G7 leadership for sustainable, resilient and inclusive economic recovery and growth, estimated that US$2.6trn - US$3.2trn in annual global investments will be needed to deliver on the transition to a low-carbon economy, 75% of which will need to be targeted outside of the world’s seven largest developed economies.

Emerging markets financing sources

There are three broad sources of financing in emerging markets that this paper touches on:

- Domestic revenue mobilisation: through taxation and private savings, such as pensions. These contribute to local capital markets.

- Official Development Assistance: external government aid that promotes and specifically targets the economic development and welfare of developing countries.

- Private capital flows: portfolio flows from institutions, businesses and individuals – for example, foreign investors purchasing equity shareholdings and interests in debt securities. This also includes international trade and foreign direct investment.

Institutional investors choose to invest in emerging markets for several reasons, including:

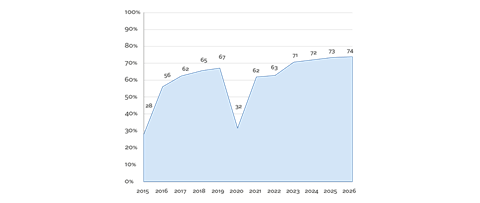

- To gain exposure to large and growing economies: Emerging market economies have seen their GDP grow faster than developed markets – on aggregate – in 27 of last 30 years, a trend that is forecast to continue.[5] As a result, emerging markets will continue to be a core driver of global growth, as indicated by Figure 2.

- To diversify investment portfolios: Most interviewees agreed that investors that are largely exposed to developed markets can improve their overall risk-adjusted returns by allocating to emerging markets, albeit countries within this classification are not entirely uncorrelated to developed markets due to the interconnected nature of the global economy.

- To have a real-world impact: According to the Global Impact Investor Network’s 2020 Annual Impact Investor Survey, 40% of impact investing assets are allocated to emerging markets. The industry grew by an annual 9% between 2015 and 2019, with an estimated AUM of US$715bn at year-end. More broadly, the greater development needs of many emerging markets, compared to developed markets, mean capital flows can have more potential to shape positive social and economic outcomes.[6]

- Due to home bias: Many emerging markets-based investors invest more locally than their developed markets-based counterparts, due to market familiarity, liability matching considerations and regulations requiring them to do so. For example, Regulation 28 of the South African Pensions Act sets a 70% threshold for assets to be invested domestically.

Figure 2: Contribution of emerging markets GDP growth to global GDP growth. Source: IMF (2021)World Economic Outlook: Managing Divergent Recoveries

Barriers to investment

Nonetheless, the funding gap indicates that there are significant barriers preventing greater investment flows into emerging markets:

- Global indices do not always reflect overall size of emerging markets: Emerging market economies represent a very small proportion of global public equity indices – just 12% of the MSCI’s All Countries World Index – despite comprising 57% of global GDP on a purchasing power parity basis. Market capitalisation to GDP ratios in emerging markets are also much lower. [7] Consequently, it is more difficult for investors to gain public markets exposure, and this is reflected in average allocations. [8]

- Capital flows are concentrated towards countries with least need: Market capitalisation-weighted benchmarks tend to direct institutional public market capital flows towards emerging economies with less capital shortages. For example, China, Taiwan and South Korea account for 65% of holdings in the MSCI emerging markets index , a widely used benchmark for pan-emerging markets listed equity funds, despite it covering 26 countries in total.

- Smaller capital markets and opportunity sets: Capital markets are often underdeveloped, especially for instruments such as sustainable or green bonds, and can be less liquid than in developed markets. Moreover, investment opportunity sets are limited – public markets do not provide deep access, and private markets are challenging, not least because individual opportunities are often too small for large asset owners.

- Concentrated ownership structures; limited corporate governance: Minority shareholder rights can be less secure while a higher prevalence of state-owned [9] or family-owned enterprises may also limit investment and stewardship opportunities.

- Perceptions of political and corruption risks are stronger: Investors and companies point to weak rule of law, regulatory instability, and higher levels of bribery in some emerging markets countries.

- Macroeconomic (in)stability and currency risks: Developed market-based investors have persistent concerns about macroeconomic instability and its impact on local currencies and exchange rate risks.

- Lack of data: Although also a developed markets problem, this is particularly acute in emerging markets. Availability ranges widely across different countries and becomes particularly scarce outside the large-cap universe.

- Lack of experience: Institutional investors often lack the resources and experience, particularly in private markets, to commit substantial capital.

This paper discusses how investors can use responsible investment practices such as ESG incorporation to identify opportunities and to manage risk and meet return objectives for clients and beneficiaries. It also highlights how a focus on sustainability outcomes can in some cases present solutions to the perennial challenges facing emerging market investors.

We consider the different roles that investors can play – from engaging with policy makers to working with investees.

Creating an enabling environment

Key takeaways

- Developing sustainable finance policy frameworks that can support climate and SDG-aligned capital markets is key to creating an environment that enables responsible investment.

- Many emerging market countries are developing policy tools related to corporate ESG disclosures, taxonomies and ESG incorporation duties.

- Further improvements are required: interviewees highlight a lack of consistent policies and regulations; coordination and resources, exacerbated by the COVID-19 pandemic.

- Some governments and institutions are increasingly using the SDGs and high-level climate goals to signal their commitment to building more sustainable economies and attract more responsible capital.

- Creating an enabling environment requires extensive collaboration with multilateral institutions, while the role of investors can extend beyond finance to providing expertise that can push emerging market sustainability efforts further.

Policy and regulatory frameworks

Creating an enabling environment to attract more long-term responsible institutional capital is an important step for emerging markets economies. Comprehensive policy frameworks that can support climate- and SDG-aligned capital markets are a core component of this, as set out in the PRI and the World Bank’s toolkit for sustainable investment policy and regulation .

Doing so can:

- enhance the resilience and stability of emerging market economies;

- improve market efficiency by clarifying and aligning investor and company expectations; including where considering sustainability outcomes is required or allowed;

- increase local ESG and sustainability standards, and encourage other countries to take similar steps; and

- increase the attractiveness of countries as investment destinations.

Priority elements of sustainable investment policy and regulation

Sustainable investment policy and regulation need to cover the following five areas:

- Corporate ESG disclosures, including alignment with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD)

- Stewardship (engagement and voting)

- Investors’ duties to incorporate ESG-related considerations in their investment decision making, to provide sustainability-related disclosures and to report on their ESG incorporation policies and performance targets

- Taxonomies of sustainable economic activities, defining common and clear criteria to classify projects or investments as green or sustainable

- National/regional sustainable finance strategies, that encourage and enable the low-carbon transition and the delivery of the SDGs

More detail on this can be found in A toolkit for sustainable investment policy and regulation (part 1) .

A growing number of countries are developing these policy tools – of the 750

sustainable finance policy tools tracked by the PRI

from 86 countries

[10]

, 253 can be found in emerging markets. Some examples are listed in Figure 3.

Figure 3: Emerging markets sustainable finance framework developments

|

Corporate ESG disclosures |

Countries including India, Chile and Malaysia have proposed and/or issued guidance on corporate ESG disclosures. |

|

ESG incorporation duties |

Several Latin American countries, such as Mexico, Colombia and Brazil, require local pension funds to incorporate ESG factors into their investment and risk analyses. |

|

Taxonomies |

More than 20 countries around the world, including China, South Africa and Malaysia, are working on sustainable finance taxonomies that will define the parameters of environmentally sustainable economic activities in their markets. Moreover, China is working with the EU to define a Common Ground Taxonomy under the umbrella of the G20 sustainable finance working group to highlight shared features of existing taxonomies, with a view to developing common standards. |

While the examples above indicate progress, it is also clear from our research that many emerging market governments need to introduce or strengthen sustainable finance policy frameworks.

Interviewees pointed to gaps such as:

- a lack of consistent policies and regulations that set a clear pathway to deliver on the Paris Agreement goals or on countries’ climate commitments. For example, China put 38.4 gigawatts of new coal-fired power capacity into operation in 2020 , despite the government’s commitment to be carbon neutral by 2060.

- a lack of coordination between key stakeholders and/or a lack of resources to hold laggards or rule-breakers fully to account. For example, in Brazil, the government’s funding cuts for official environmental and indigenous rights’ protection work is undermining positive action on climate disclosure requirements by the central bank and broader industry initiatives such as the Finance Innovation Lab .

The COVID-19 pandemic has exacerbated these gaps. Despite exposing critical environmental, social and governance issues, many governments have focused on short-term fiscal fixes ahead of long-term development needs.

Investors, businesses, international institutions and civil society have a role to play in supporting, incentivising or pressuring governments to improve their sustainable finance policy frameworks.

The SDGs and climate commitments

Some governments and institutions are increasingly using the SDGs and high-level climate commitments as a way of signalling their commitment to building more sustainable economies to investors. As noted above, in certain cases this has not yet translated into definitive or consistent action at the policy level. However, there are examples of how countries are aligning policy, financing plans and development strategies with the SDGs and climate goals to attract more responsible capital. These include:

- Kenya’s third Medium Term Plan under its social and economic development strategy – Kenya Vision 2030 – which seeks to align all policies and programmes with the SDGs.

- Colombia’s Inter-Sectorial Commission on Climate Change (CICC), which supports stronger government coordination and planning in relation to the country’s infrastructure needs to meet its climate change goals. Through the Ministry of the Environment and Sustainable Development and the National Planning Department, the CICC brings together ministries and regional authorities, government climate policy and national and sub-national action. There is also a clear remit for fostering dialogue with and communicating investment opportunities to the private sector.

Several countries have also issued green and sustainability bonds that link directly to development strategies and projects that are aligned with the SDGs and/or climate-related goals ( see Supply of investable opportunities for more detail ).

Multi-stakeholder collaboration and initiatives

Creating an environment that enables responsible investment is not just the remit of governments, and often requires extensive collaboration with multilateral institutions, including the World Bank and various development finance institutions (DFIs).

Such organisations have long been involved in providing technical assistance and financial resources to emerging markets – an increased focus on sustainability outcomes directly aligns – and gives impetus to – their core missions. Institutional investors can also play a role beyond finance to provide expertise on myriad issues to push the emerging market sustainability efforts further.

Examples of recent collaborative initiatives include:

- The International Finance Corporation-led Scaling Solar programme, which has helped build competitive renewable energy markets in several countries since 2015, including Zambia, Senegal and Uzbekistan.

- FAST-Infra , which aims to accelerate the flow of private investment to sustainable infrastructure in developing countries. The private-public partnership involves infrastructure investors, banks, DFIs and non-governmental organisations.

- The UN-convened Global Investors for Sustainable Development Alliance (GISD), which brings together several large global financial institutions and corporations, and works to overcome barriers and scale up financing for long-term investment, including in emerging markets.

ESG data in emerging markets

The need for meaningful and comprehensive ESG data is a theme that cuts across all elements of this paper. For emerging markets such data is often severely lacking, caused by weak or non-existent disclosure requirements and poor coverage by most major data providers, among other factors.

This represents a significant barrier to increasing responsible investment in emerging markets, making it more difficult to eliminate the gap between actual and perceived risk and to assess the ESG performance of investee companies and assets. [11] This has a negative effect not only on decisions around asset allocation, manager selection and different investment products, but also on the way that engagements can be conducted with investee companies or how assets and portfolio companies are managed on the ground.

Some progress has been made, albeit starting from a low base. Some investors are either building their own datasets and data assessment capabilities (see Developing an ESG rating system – China Southern Asset Management), or accessing free datasets provided by institutions such as the World Bank, to help identify potential opportunities or strengthen their investment decisions.

Developing an ESG rating system – China Southern Asset Management

China Southern Asset Management has developed an ESG rating system for Chinese bond issuers based on internal research and external data. The rating system covers sovereign, supranational and agency bonds, corporate bonds, and asset-backed securities across 52 ESG themes and 104 indicators. China Southern Asset Management uses artificial intelligence to mine data, capture and monitor ESG controversies, and to increase its ESG data coverage and diversity.

Further detail can be found in China Southern Asset Management’s shortlisted PRI Awards 2021 entry for Emerging markets initiative of the year.

Interviewees also point to evidence of progress among policy makers and stock exchanges:

- Financial regulators in Brazil and South Africa have developed corporate ESG disclosure rules, while Russian authorities are considering introducing these on a comply-or-explain basis.

- An increasing number of emerging market countries are also adopting the recommendations of the TCFD, including Mexico, Brazil and South Africa.

- The Sustainable Stock Exchanges initiative is working to develop model guidance on climate disclosure and has developed training programmes for stock exchanges on ESG issues more broadly.

Nonetheless, ensuring that ESG data on emerging market companies, sovereigns and assets is meaningful and comprehensive will require extensive, and intensive, collaboration by a range of stakeholders ( see Next Steps section ).

Asset allocation

Key takeaways

- Having a strong understanding of ESG factors and developing robust processes to assess how these apply in different contexts can help investors to overcome some of the barriers associated with emerging markets investing.

- The belief that emerging market investments can deliver greater real-world impact than investing in developed markets, alongside the potential for strong returns and diversification, is an additional factor in asset allocation decisions. Some asset owners view them as a way to deliver on the SDGs or climate goals.

- The use of ESG ratings within index construction can pose challenges for emerging market investments, as constituents often score lower on ESG issues than their developed markets counterparts.

While policy makers need to create an environment that enables responsible investment, asset owners can take steps to understand how their asset allocation decisions can support greater allocations to emerging markets.

Building knowledge and overcoming misperceptions

Having a strong understanding of ESG factors and developing robust processes to assess how these factors apply in different contexts can help investors to overcome some of the barriers associated with emerging markets investing.

Some of the risks most cited – around political or social instability, or corruption, for example – stem from underlying issues such as inequality, health and safety, decent work, and gender disparities.

Investors with a strong grasp of these are therefore better placed to determine and manage the materiality of those risks in specific emerging markets, rather than relying on common (mis)perceptions to shape their positions.

Ultimately, developing better knowledge of emerging markets will drive more informed decisions on what products, investments and managers can best meet their requirements. Our interviews revealed some of the ways in which asset owners are building the capabilities to do so, including:

- Establishing local offices in or around the countries they want to invest in, particularly if they view emerging markets as a core source of long-term growth. For example, the Canada Pension Plan Investment Board aims to have one-third of its capital invested in emerging markets by 2025 , and has built a significant presence in markets such as Latin America and Hong Kong to support that effort.

-

Collaboration with external parties

that have a longer-term track record in emerging markets or specialist investments. For many years, institutional investors have partnered with DFIs, in large part to benefit from their local knowledge and potential to de-risk projects. Other examples point to deeper levels of collaboration and bringing together expertise outside of the development finance world:

- STOA , a French entity that invests in sustainable infrastructure and energy projects in emerging markets, is a collaboration between the pension fund Caisse des Dépôts and Consignations, and Agence Française de Développement, the French development agency. The former provides the financial expertise, the latter primarily the sustainability knowledge and experience of emerging markets.

- A Canadian pension fund with a track record in infrastructure investing has partnered with a Latin American pension fund to share asset class expertise and local knowledge respectively.

Real-world impact

The belief that investing in emerging markets can deliver greater real-world impact than investing in developed markets is also evolving as a factor in asset allocation decisions, according to several interviewees, alongside more traditional considerations such as the potential for strong returns and diversification.

For example, some asset owners are making a direct link between emerging market investments and delivering on the SDGs or on climate change commitments.

This can take different forms. The Institutional Investors Group on Climate Change’s Net-Zero Investment Framework encourages asset owners to consider less familiar asset classes, such as renewable energy. Emerging economies that develop renewable energy industries can benefit from this, with India, Vietnam, Chile and Mexico already proving attractive for institutional investors. [12]

In Scaling Blended Finance , the Net-Zero Asset Owner Alliance (NZAOA), highlights greater investment in emerging markets as a critical means for its members to help meet their commitments to decarbonise their investment portfolios to net-zero by 2050.

“You can’t be an emerging markets investor without thinking about development goals – the high [political] risks make it essential to align your investments with the needs of the local markets.”

Private equity general partner

Strategic asset allocation and responsible investment

Although still a nascent practice, considering real-world outcomes and ESG factors during the strategic asset allocation process may lead asset owners to direct more capital towards emerging markets and as a result, can contribute to the SDGs and the Paris Agreement. [13]

Readers can refer to a series of cases studies that outline signatory approaches to responsible investment and SAA .

ESG data in emerging markets

The need for meaningful and comprehensive ESG data is a theme that cuts across all elements of this paper. For emerging markets such data is often severely lacking, caused by weak or non-existent disclosure requirements and poor coverage by most major data providers, among other factors.

This represents a significant barrier to increasing responsible investment in emerging markets, making it more difficult to eliminate the gap between actual and perceived risk and to assess the ESG performance of investee companies and assets.11 This has a negative effect not only on decisions around asset allocation, manager selection and different investment products, but also on the way that engagements can be conducted with investee companies or how assets and portfolio companies are managed on the ground.

Some progress has been made, albeit starting from a low base. Some investors are either building their own datasets and data assessment capabilities ( see Developing an ESG rating system – China Southern Asset Management ), or accessing free datasets provided by institutions such as the World Bank, to help identify potential opportunities or strengthen their investment decisions.

Developing an ESG rating system – China Southern Asset Management

China Southern Asset Management has developed an ESG rating system for Chinese bond issuers based on internal research and external data. The rating system covers sovereign, supranational and agency bonds, corporate bonds, and asset-backed securities across 52 ESG themes and 104 indicators. China Southern Asset Management uses artificial intelligence to mine data, capture and monitor ESG controversies, and to increase its ESG data coverage and diversity. Further detail can be found in China Southern Asset Management’s shortlisted PRI Awards 2021 entry for Emerging markets initiative of the year.

Supply of investable opportunities

Key takeaways

- There are examples of investment products or structures that can ensure responsible capital directly supports key sustainability outcomes, such as green/sustainable development bonds and blended finance, but their use needs to be expanded.

- Where asset owners prefer to access emerging markets opportunities through third-party investment managers, assessing their responsible investment practices can help establish their credibility.

“Institutional investors have clear potential to be part of the solution, but they lack viable means to access responsible investing opportunities at scale. What is often missing is the bridge for their huge pools of capital to flow into development projects.”

OECD (2021) Mobilising institutional investors for financing sustainable development in developing countries

Finding suitable investment opportunities is critical to increasing emerging market investment flows, but this is challenging as asset owners often face structural constraints, such as only being able to invest in investment-grade securities or lacking the resources and capabilities to be innovative with investment opportunities.

Having mismatched expectations regarding minimum investment sizes, risk vs reward and track record (when assessing external managers) can also hold some asset owners back from deploying capital.

Private equity: Finding opportunities to reduce ticket sizes

Interviewees highlighted private equity as an asset class that offers opportunities for those willing to take a creative investment approach, such as setting up specific structures to access smaller deals or managers. One asset owner has ringfenced US$500m to make impact investments and will deploy individual US$5m tickets to “get a seat at the table”. It also noted that smaller deals can sometimes generate better returns.

Nonetheless, more innovative approaches are being developed. Below we detail two examples of investment products or structures that were highlighted during our interviews as ways to ensure such capital directly supports key sustainability outcomes. We also outline some of the approaches that interviewees take when using investment managers to access emerging markets opportunities more broadly and the importance of ESG considerations in this context.

Green and/or sustainable development bonds provide one way for asset owners to access emerging market opportunities that support sustainability outcomes, particularly as bonds are still the principal way in which many emerging markets countries access capital markets.

These bonds ensure that funds are ringfenced for a specific purpose or outcome, which investors can use to set mutually aligned KPIs. Investors have transparency on what the proceeds are used for and see them as a means to improve governance in certain jurisdictions – for example, by building better understanding of the type of disclosure and transparency mechanisms required by international institutional investors.

More generally, the development of green and/or sustainability bond markets presents an opportunity to support knowledge transfer and capacity building on sustainable finance in emerging economies:

- A collaboration between the International Finance Corporation (IFC) and the Climate Bonds Initiative aims to support members to develop green bond markets by enhancing collective knowledge, capacity and awareness; developing technical resources, and supporting the integration of ESG factors into all stages of issuance and reporting.

- The Inter-American Development Bank has developed a Green Bond Transparency Platform that aims to support better practice in the green bond market in Latin America and the Caribbean, by:

- supporting the harmonisation and standardisation of green bond reporting for issuers; and

- allowing users to analyse where bond proceeds are invested and what environmental performance was realised.

Growing investor and issuer interest

Interest in green and sustainable bonds is growing among investors and issuers alike. Many interviewees highlighted their willingness to invest in these issuances, particularly when backed by or developed in collaboration with multilateral institutions. Recent examples include:

- Egypt, which launched its first-ever green bond in 2020 and earmarked the US$750m proceeds to finance public investment projects aligned to at least one of the SDGs, under a framework developed with the World Bank.

- Mexico, which announced a US$890m SDG bond in 2020 that will finance projects in some of its most vulnerable and poorest municipalities – identified through a geospatial study.

- The Asian Infrastructure Investment Bank, which will target sustainable development in all its new bond issuances. It will require annual reporting on a range of social and environmental impacts tied to the SDGs on all its investments at a project and portfolio level.

- Ecuador, which will finance investment in affordable and decent housing using a US$400m sovereign social bond – the world’s first – guaranteed by the InterAmerican Development Bank. This aligns with the country’s commitments to various SDGs.

As of December 2020, 15 emerging market sovereigns had issued a green, sustainable or social (GSS) bond, according to the Climate Bonds Initiative.

Figure 4. Sovereign GSS bond issuance in 2020. Source: Climate Bonds Initiative (2020) Sustainable Debt: Global State of the Market 2020

| Theme | Market | Country | US$ bn as of 31/12/2020 |

|---|---|---|---|

|

Green bonds |

DM |

France |

30.7 |

|

DM |

Germany |

13.6 |

|

|

DM |

Netherlands |

10.0 |

|

|

DM |

Belgium |

8.2 |

|

|

DM |

Ireland |

5.7 |

|

|

DM |

Sweden |

2.3 |

|

|

DM |

Hong Kong |

1.0 |

|

|

EM |

Chile |

6.2 |

|

|

EM |

Poland |

4.3 |

|

|

EM |

Indonesia |

3.1 |

|

|

EM |

Hungary |

1.9 |

|

|

EM |

Egypt |

0.8 |

|

|

EM |

Lithuania |

0.1 |

|

|

EM |

Nigeria |

0.1 |

|

|

EM |

Fiji |

0.05 |

|

|

EM |

Seychelles |

0.02 |

|

|

Sustainability bonds |

DM |

Luxembourg |

1.8 |

|

EM |

Thailand |

2.1 |

|

|

EM |

Mexico |

0.9 |

|

|

EM |

South Korea |

0.5 |

|

|

Social bonds |

EM |

Chile |

2.1 |

|

EM |

Guatemala |

1.7 |

|

|

EM |

Ecuador |

0.7 |

The COVID-19 pandemic has exacerbated government financing needs and sparked further interest in GSS bonds. According to UNCTAD’s World Investment Report 2020, the value of COVID-19 response bonds – issued to focus on relief provision and SDGs such as good health and wellbeing – reached US$55bn by mid-April 2020, already surpassing the US$13bn in social bonds issued in 2019.

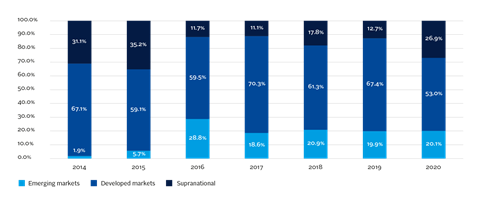

However, green and sustainability bond issuance from emerging markets remains relatively small as a proportion of overall issuance, as demonstrated in Figure 5. Of the US$700bn in GSS bonds issued in 2020 globally, only 20% (US$140bn) originated from emerging market countries, the vast majority of which came from China.[17]

Figure 5: Proportion of emerging market GSS bonds issuance (2014 – 2020). Source: Climate Bonds Initiative

Improving bond accessibility

Despite their interest, interviewees noted that poor communication from issuing countries means GSS bonds are not always easily accessible. Stock exchanges in several markets are taking steps to improve their visibility, however, by launching dedicated green or sustainable bond sections to showcase them, including Mexico, Chile, India, Nigeria, China and Indonesia.[18]

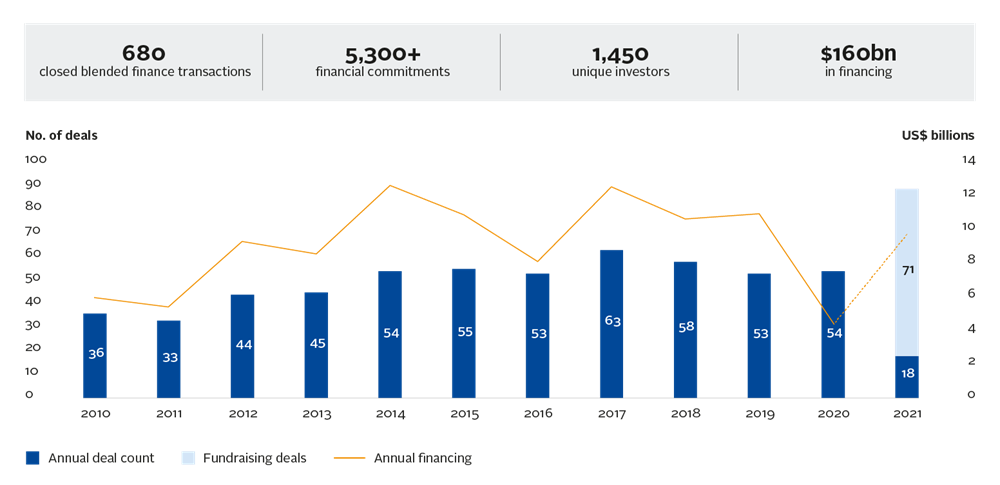

Blended finance

The strategic use of development finance to mobilise additional capital towards sustainable development [19] has attracted much attention for its potential to make projects and companies more investible.

Mechanisms such as first-loss guarantees, currency hedging and risk insurance can lower the risk for institutional investors, making blended finance an important tool for attracting increased investment to projects that contribute to the SDGs and climate goals, as recognised by the NZAOA and the GISD. The latter published a report in 2020, Renewed, Recharged and Reinforced: Urgent actions to harmonize and scale sustainable finance , calling for a global blended finance fund to be established to rapidly scale up investments that contribute to the SDGs.

However, despite the increased attention it has received, the scale of blended finance activities remains small ( see Figure 6 ) compared to overall financing needs. Research by Convergence , a global network for blended finance, highlights that more private capital needs to be mobilised through blended finance structures by multilateral development banks (MDBs) and other public institutions.

To this effect, the Business and Sustainable Development Commission’s Blended Finance Taskforce recommended that MDBs set ambitious targets for mobilisation, standardise products, reduce transaction times, pool assets and recycle them off their balance sheets, and create shifts in incentives and capabilities. These are all measures that could help improve the attractiveness of blended finance opportunities to institutional investors.

Figure 6: Blended finance flows 2010 – September 2021. Source: Convergence (2021) The State of Blended Finance 2021 .

The challenge here is not just financial – creating enough bankable projects to invest in is equally important.

For example, the SDG Investment Fund, a blended finance fund managed by the Danish development finance institution IFU, had total commitments of around €650m in 2018, but it had only managed to deploy 46% to active investments by its third year due to a lack of such projects. [20]

Bankable projects can grow if emerging market governments develop the market conditions to enable them – with technical support from multilateral institutions and other stakeholders, as discussed in Creating an enabling environment .

Manager selection

While some asset owners access emerging markets investment opportunities directly, others use third-party investment managers. Interviewees highlighted various approaches to doing so, including:

- Allocating to large investment managers and funds: Some asset owners prefer to invest in large emerging markets-focused funds run by some of the world’s biggest investment managers – such as KKR, which closed a US$15bn Asia-Pacific-focused fund in April 2021 , or Hillhouse Capital, which raised US$18bn for its most recent fund . They do so for several reasons, including cost considerations, to gain exposure to a broader range of investments and economies, or familiarity with bigger managers compared to smaller specialists. However, some interviewees expressed concern that this approach can exclude smaller managers and lead to more investments in larger companies rather than the small and medium-size enterprises that may have more urgent capital needs.

- Investing in funds of funds: Some asset owners prefer to use a fund of funds structure for their emerging market investments – even if they wouldn’t take this approach for their developed market investments – as it can provide highly diversified exposure to managers, markets and opportunities that they would otherwise not have access to.

- Allocating to managers with specific expertise: Others increasingly look to investment managers with specific regional expertise, rather than firms that cover all emerging markets, on the basis that they better understand those geographies and the ESG factors that are most material to them.

Regardless of their overall investment objectives, most interviewees emphasised the importance of assessing a manager’s responsible investment approach to establish their credibility. Although relevant to manager selection in all markets, it is considered particularly relevant in emerging markets, because strong ESG and sustainability capabilities can:

- better distinguish which factors are most relevant per country, given the diversity of emerging markets ( see also Asset allocation and ESG incorporation and active ownership sections );

- ease the reluctance that some asset owners have to invest with managers that lack an established investment track record; and

- offset the lack of quality emerging markets ESG data that is readily available, particularly if managers develop their own data and analytics beyond what third-party firms can provide ( see also ESG data in emerging markets ).

Manager selection, appointment and monitoring resources

The PRI has produced guidance for asset owners on embedding ESG requirements into manager search, selection, appointment and monitoring processes. These can be found at https://www.unpri.org/investment-tools/asset-owner-resources .

ESG incorporation and active ownership

Key takeaways

- Emerging markets investors apply responsible investment practices at the investee level to manage risks and unlock value. Some also do so to potentially generate more positive real-world outcomes than they can with many developed markets investments.

- The many tools and frameworks available to support investors doing so are relevant across jurisdictions. To be effective, an understanding of how they apply in varying local contexts is required.

- Several organisations are using sustainability outcomes to further assess individual investments – by using the SDGs or nationally defined contributions for example.

- Improving the ESG performance of investees through engagement is an important part of being a responsible investor – potential holdings should not necessarily be dismissed as laggards if they do not initially meet certain standards or criteria.

- There are several challenges to engagement in emerging markets and investors should consider how these can be mitigated so they can fulfil their duties as responsible stewards of capital.

Emerging markets investors – whether investment managers or asset owners – can apply responsible investment practices at the investee level to manage risks and unlock value.

Some investors also do so to potentially generate more positive real-world outcomes than they can with many developed markets investments.

Below we detail some of the considerations and challenges investors face when undertaking ESG incorporation and active ownership, and – where they do so – when looking to shape sustainability outcomes within those practices.

Assessing ESG factors

Most interviewees agreed that while key ESG factors are often assessed in the same way across many different developed markets, assessing them in emerging markets requires real understanding of each country’s nuances and contexts.

For example, labour standards can be considered reasonably homogenous across much of the EU but can vary significantly in emerging markets, including within the same region – indeed, 86% of the world’s informal employment is in emerging countries, the International Labour Organisation estimates .

“You need [to take] a nuanced approach in the implementation of ESG standards, as they can differ between countries [given their different] cultures, legislation, business integrity and corruption [risks]. It needs to be done on a case by case basis.”

Developed markets-based investment manager

Interviewees also highlighted that greater emphasis is often placed on social and governance factors than environmental factors – that in turn requires investors to adopt different approaches to understanding and managing these critical issues.

For example, in Latin America, many economies and companies depend on ‘dirty’ industries such as mining, oil and gas, and cement. In this context, while investor support for decarbonisation efforts is hugely important, more consideration must be given to the jobs and broader socio-economic development that those industries support. Failing to do so risks further exacerbating the already-high levels of poverty in the region. This could subsequently drive greater levels of inequality, political instability and unrest and undermine longer-term growth prospects.

Investors therefore have a significant responsibility to understand and help address these long-term challenges as they engage with governments and companies – from the perspective of facilitating the transition to a cleaner economy and of advancing human rights, an agenda that will grow in importance for investors in the years ahead .

The just transition and emerging markets

Investors need to be cognisant of the just transition, a concept incorporated in the 2015 Paris Agreement to signal the importance of minimising negative repercussions from climate policies and maximising positive social outcomes for workers and communities.

It involves adopting a holistic approach to transitioning to a climate-resilient, net-zero economy that takes into account the social implications on workers, communities and consumers.

This can be more difficult in emerging markets due to existing levels of inequality, limited social safety nets, and a lack of resources to support workers or communities to retrain or find alternative sources of income, as well as emerging markets’ broader and more pressing developmental needs.

“A lot of families depend on these jobs – so there is a conflict between environmental and social [factors] and you cannot take the traditional approach that investors in Europe or US may take. We are trying to learn from developed market experiences but also to adapt to our reality.”

Emerging markets-based asset owner

Developing the expertise internally to assess ESG factors in an emerging markets context – whether in a dedicated team or more broadly across the organisation – can take time and resources.

However, in the absence of widespread coverage of emerging markets by ESG data providers ( see ESG data in emerging markets ), this is regarded as a necessity by most emerging markets-focused managers.

Many firms use external consultants to support this work, although interviewees noted that environmental expertise is more prevalent than social and governance expertise among such third-party organisations.

Private markets investors also highlighted that frameworks such as the IFC’s Environmental and Social Performance Standards are an excellent starting point for work on identifying ESG risks and opportunities. Many other DFIs have similar frameworks of their own.

Assessing opportunities through an outcomes lens

Several organisations are using sustainability outcomes to further assess individual investments:

- The SDGs : One private markets investor interviewed cited an investment in a company providing temporary energy solutions for social infrastructure such as hospitals and schools. The investor used the SDGs to help identify the social benefits that the deal could deliver, while at the same time working with the company post-investment to mitigate the negative impact caused by using high-emission fuels, helping the investee transition to cleaner technology.

- The Nationally Defined Contributions (NDCs) : Another investor highlighted how it considers opportunities in the context of each individual country’s climate trajectories in their NDCs under the Paris Agreement. An investment in a (more developed) country may be rejected because its associated emissions are too high, but the same type of investment in a different (less developed) country may be accepted because the emissions fall within its climate trajectory, and because of the wider societal benefits the investment can bring.

“We evaluate across the SDGs and how an investment impacts on [them], both positively and negatively. We look to the opportunities to improve over time, by decreasing the negatives.”

Developed markets-based investment manager

Investing for impact – Norsad Finance

Norsad Finance invests for impact in the Southern African region (across the Southern Africa Development Community), providing direct debt financing of US$5m to US$10m to financial institutions and to mid-market companies for growth and development. Norsad’s principal objective is to contribute to private sector development by providing funding to enterprises that:

- are financially, socially and environmentally sustainable;

- create jobs with decent working conditions;

- adopt good governance practices; and

- contribute to economic growth and poverty alleviation.

To achieve this, all its investments go through a rigorous ESG and impact screening assessment, and it helps investee companies to formulate and implement adequate internal social and environmental policies. Norsad’s impact goals and objectives are selected to closely align with regional development priorities for the countries within the Southern African Development Community region, and with the SDGs. This means that any impact outcomes achieved should be appropriate to the local context and country needs.

Further detail can be found in Norsad Finance’s winning entry to the PRI Awards 2021 for Emerging markets initiative of the year.

Resources for assessing impact

Frameworks such as the IFC’s Operating Principles for Impact Management have been developed in recent years to support investors with their work on impact assessment and disclosure. Other tools highlighted through our research include:

- The SDG Index , which identifies and tracks countries’ progress towards the SDGs and which some investors are using to identify where to invest with impact; and

- The SDG Investor Platform , which provides data, information and insights on investment opportunities with potential to contribute to sustainable development.

Building on existing ESG practice

That ESG practice always lags in emerging markets is a common misconception. Interviewees highlighted that engaging with some emerging markets-based companies is easier, because they are aware that improving their business practices and generating good ESG performance can increase their access to foreign investment.

For example, Africa-focused private equity firm Adenia Partners acquired Mauvilac, a decorative paint company in Mauritius, in July 2014. It embarked on a transformation plan with the company to help it meet international sustainable standards and infrastructure, including developing Go-Green, the first range of environmentally friendly paints in Mauritius, implementing sustainable waste management and solvent recycling systems. According to Adenia Partners, Mauvilac is now in line with ISO 9001, ISO 14001 and ISO 45001 for quality, environmental and occupational health and safety management respectively. Furthermore, these initiatives led to strong interest from various strategic and financial buyers during an exit process that ultimately led to Mauvilac’s sale, in April 2020, to Akzo Nobel.

In private markets, the role of DFIs and/or donors as the traditional sources of much investment has also meant that many companies and projects in those markets have applied thorough ESG practices far longer than their developed market counterparts. These practices are a fundamental condition of development or donor capital and such investments often include significant technical support to ensure that the appropriate ESG standards are met.

Moreover, some private equity interviewees emphasised the importance of working with local venture capital or investor associations to provide training – for example, on responsible investment or on working with asset owners from developed markets – to help grow capacity at the investment manager level.

The PRI is developing its own mentorship programme to foster knowledge sharing and transfer on responsible investment between asset owners in developed markets and their counterparts in emerging markets.

Improving performance through active ownership

Improving the ESG performance of investees is an important part of being a responsible investor and interviewees stressed that potential holdings should not necessarily be dismissed as laggards if they do not meet certain standards or criteria – rather, investors should assess how they can improve.

This is particularly important given the poor ESG data coverage of emerging markets companies and investor perceptions regarding their potentially lower operating standards and business practices.

Going one step further, investors that want to align their approach with Active Ownership 2.0 could consider how their investments shape sustainability outcomes and the impact this could have on employees, communities and the broader economy, alongside returns. This reflects the PRI’s work on investors shaping SDG outcomes.

“[It is] much better to invest in companies not yet at the top but which have the potential to be best-in-class. The easy thing is to exclude; [in the] long term you should include and engage.”

Developed markets-based investment manager

Below we highlight some of the challenges associated with undertaking engagement in emerging markets, as well as some of the factors that can potentially mitigate these.

Lack of familiarity with engagement

The concept of engagement is not always well understood and investors may need to dedicate more time or resources to articulate the value they bring.

Regardless, responsible investors have a duty to be active stewards of capital. For PRI signatories, this is enshrined in Principle 2 .

If engaging individually is not effective or feasible, collaborative engagement provides another route for fulfilling this duty. [21] This is also a core component of the PRI’s Active Ownership 2.0 , which prioritises delivering outcomes on systemic issues. This can only be achieved through enhanced collaborative engagement, where investors coordinate on specific objectives while taking some actions individually.

Research on PRI-coordinated collaborative engagements between 2007 and 2017 found that success rates increased by about one-third when there was a lead investor heading the dialogue on behalf of a coalition. They were particularly enhanced when that investor was headquartered in the same region as the target firm.

It noted: “For maximum effect, coordinated engagements on ESG issues should have a lead investor that is well suited linguistically, culturally and socially to influencing target companies.” This is particularly important in emerging markets, given their diversity.

“The value that the investor brings, through the due diligence it does, its gap analysis against the IFC Performance Standards etc [needs to be] articulated … in a way that the [investee] can understand.”

Development markets-based investment manager

Ownership structures

The predominance of family- or state-owned enterprises can change the dynamics of an engagement, with investors potentially having to navigate a range of political or private considerations in the process. Company structures – including their boards – may not always be institutionalised, which can also affect investor engagement and its outcomes.

Nonetheless, according to research by Credit Suisse , family-owned businesses can have a longer-term focus compared to non-family-owned companies, which can contribute to their outperformance.

Emerging and frontier equities specialist East Capital points out in its annual sustainability report that its starting point for identifying potential investments (and the basis for its engagement activities) is to assess a company’s ownership.

It notes that the more personal nature of company management requires investors to have boots on the ground – “you have to meet the owners, virtually if not physically. While some shareholders may be reluctant to engage, those in it for the long haul will most likely be glad to establish a dialogue.”

Investment universe limits

Escalating an unsuccessful engagement with or divesting from emerging markets holdings may be harder than in developed markets, given the lack of potential alternative investment options. Divestment may also be difficult where a country or sector is financially significant to a portfolio or index.

As a consequence, one asset owner noted that it has developed a country engagement framework based on the salience of human rights issues and is using that to increase its engagement efforts with companies, including obtaining information on their processes for human rights risk management. This is aligned with the responsibility all investors have to respect human rights.

Active ownership and respecting human rights

Institutional investors have a responsibility to respect human rights, as outlined in PRI (2021) Why and how investors should act on human rights . Active ownership is one way that investors can meet this responsibility, by influencing investees to change wrongful practices that are contributing to or causing harm. Investors’ influence will vary across investment instruments and may be limited – further guidance on what they should consider in these circumstances are outlined in the paper. The PRI has also published a series of case studies outlining how signatories are considering human rights in their responsible investment practices, and a paper on the important role of sovereign debt investors in addressing human rights issues.

Next steps

To ensure that investment managers and asset owners can meet their return objectives while contributing to closing the funding gap in emerging markets, several challenges need to be addressed. This requires investors, multilateral institutions, service providers and governments to take concerted, collaborative, long-term action across the areas discussed in this paper.

Below we summarise some potential actions they can take, which we would like feedback on. The PRI will assess how it can support these by leading, facilitating or supporting relevant initiatives, particularly where greater collaboration between asset owners and investment managers is required.

Creating an enabling environment

Key challenges :

- The existence and implementation of sustainable finance policy frameworks varies widely between countries.

- ESG data provider coverage of emerging markets is weak.

Suggested actions :

- Institutional investors and multilateral institutions continue to engage with governments and local regulators on developing and implementing sustainable finance policy frameworks that align with the SDGs and the Paris Agreement.

- Standard setters, institutional investors, corporates and stock exchanges collaborate to improve capital market disclosure practices.

- Interested stakeholders collaborate to engage with ESG data providers to improve emerging markets data coverage and methodologies.

Asset allocation

Key challenges :

- Asset owners can lack expertise to assess emerging market risks and opportunities.

- Sustainability outcomes and ESG factors are not widely considered in asset allocation.

- Mainstream and ESG index composition can be problematic for emerging markets, affecting asset allocation decisions.

Suggested actions:

- Support investment consultants and asset owners develop strategic asset allocation frameworks that consider sustainability outcomes.

- Relevant stakeholders collaborate and engage with regulators, ESG data and index providers to expand emerging markets coverage and improve index and rating methodologies.

- Developed and emerging markets-based asset owners share their experiences to develop best practices.

Supply of investable opportunities

Key challenges :

-

Accessing opportunities and bankable projects that:

- adhere to green/SDG standards;

- meet investors’ liquidity and risk constraints.

- Poor signposting of green/SDG investment opportunities.

- Not enough private capital mobilisation by multilateral development banks and other public institutions.

- Emerging markets-based managers face significant barriers to attracting commitments from institutional asset owners.

Suggested actions:

-

Continue knowledge and capacity-building efforts to help institutional investors access:

- sustainable investment opportunities (such as green, social and sustainability bonds, blended finance);

- local partners, data and risk mitigation tools.

- Further align incentives between donors, development finance institutions and institutional investors.

- Investors seek out opportunities to participate in and/or support asset class-specific activities that aim to grow opportunities and capacity in emerging mar

ESG incorporation and active ownership

Key challenges :

- Cultural and structural differences in the understanding and application of active ownership.

- Insufficient local ESG and impact knowledge and experience, whether within the investment community or companies.

Suggested actions:

- Raise awareness about the different engagement approaches and how to identify critical sustainability issues in local contexts.

- International and local investors find opportunities to engage collaboratively, share information and develop best practice.

- Continue partnerships between development finance institutions and local emerging market partners (investors, government agencies, regulators etc) to provide ongoing technical support on responsible investment.

The PRI would welcome feedback from signatories on these suggested actions and what we can do to support them as we look to further develop our work programmes in this area.

Appendix

| IMF emerging and developing economies | ||

|

Afghanistan Albania Algeria Angola Antigua and Barbuda Argentina Armenia Aruba Azerbaijan The Bahamas Bahrain Bangladesh Barbados Belarus Belize Benin Bhutan Bolivia Bosnia and Herzegovina Botswana Brazil Brunei Darussalam Bulgaria Burkina Faso Burundi Cabo Verde Cambodia Cameroon Central African Republic Chad Chile China Colombia Comoros Democratic Republic of the Congo Republic of Congo Costa Rica Côte d’Ivoire Croatia Djibouti Dominica Dominican Republic Ecuador Egypt El Salvador Equatorial Guinea Eritrea Eswatini Ethiopia Fiji Gabon The Gambia

|

Georgia Ghana Grenada Guatemala Guinea Guinea-Bissau Guyana Haiti Honduras Hungary India Indonesia Iran Iraq Jamaica Jordan Kazakhstan Kenya Kiribati Kosovo Kuwait Kyrgyz Republic Lao P.D.R. Lebanon Lesotho Liberia Libya Madagascar Malawi Malaysia Maldives Mali Marshall Islands Mauritania Mauritius Mexico Micronesia Moldova Mongolia Montenegro Morocco Mozambique Myanmar Namibia Nauru Nepal Nicaragua Niger Nigeria North Macedonia Oman Pakistan Palau |

Panama Papua New Guinea Paraguay Peru Philippines Poland Qatar Romania Russia Rwanda Samoa São Tomé and Príncipe Saudi Arabia Senegal Serbia Seychelles Sierra Leone Solomon Islands Somalia South Africa South Sudan Sri Lanka St. Kitts and Nevis St. Lucia St. Vincent and the Grenadines Sudan Suriname Syria Tajikistan Tanzania Thailand Timor-Leste Togo Tonga Trinidad and Tobago Tunisia Turkey Turkmenistan Tuvalu Uganda Ukraine United Arab Emirates Uruguay Uzbekistan Vanuatu Venezuela Vietnam West Bank and Gaza Yemen Zambia Zimbabwe |

Downloads

References

[1] OECD (2020) Global Outlook on Financing for Sustainable Development 2021: A New Way to Invest for People and Planet

[2] See for example Advocates for International Development (2021) Understanding the developed/developing taxonomy

[3] These numbers exclude developed markets-based investors with a focus on emerging markets and some emerging markets-based investors that are registered outside their home country.

[4] OECD (2020) Global Outlook on Financing for Sustainable Development 2021: A New Way to Invest for People and Planet

[5] International Monetary Fund (2021) World Economic Outlook: Managing Divergent Recoveries

[6] All investor actions shape positive and negative outcomes in the world. Investors that are focused on sustainability outcomes should try to understand the outcomes their investments and related activities have and seek to shape them in line with sustainability goals such as the SDGs. We define impact as a change in outcome (i.e. an outcome shaped by an investor, in line with the SDGs).

[7] According to the World Bank, the latest market capitalisation to GDP figure for OECD countries is 131%, while it is 53% for Latin America and just 13% for Western and Central Africa.

[8] Research by Morgan Stanley estimated that global equity investors should allocate between 13% and 39% of their portfolios to emerging markets, based on an analysis of three asset allocation strategies. However, the average allocation is between 6% and 8%. Among pension funds, it is even lower (4%), according to Mercer.

[9] A quarter of publicly listed companies in emerging economies are state-owned compared to 4% in developed economies. For more detail, see Can State-Owned Enterprises play a role in global environmental engagement?

[10] As of July 2021.

[11] For example, see comments by Standard Chartered, a GISD member at the OECD’s Blended Finance and Impact week (Feb 2021).

[12] For an example, see SDG infrastructure case study from Actis.

[13] Putting sustainability outcomes at the core of allocation decisions has also received attention at a policy level. For example, in 2005 the OECD Journal on Budgeting published an article exploring how sustainability analysis can be built into national budget processes, while in 2015 Mark Carney discussed the idea of a carbon budget.

[14] Responsible Investor (2020) The unintended consequences of sovereign ESG benchmarks

[15] Raddatz et. Al, Journal of International Economics 108:413-30 (2017) International Asset Allocations and Capital Flows: The Benchmark Effect

[16] Bloomberg (2021) Passive likely overtakes active by 2026, earlier if bear market

[17] See Climate Bonds Initiative Data Platform.

[18] See the Sustainable Stock Exchanges Initiative database or the Climate Bonds Initiative Green Bond Segments on Stock Exchanges.

[19] Taken from the OECD definition – see https://www.oecd.org/dac/financing-sustainable-development/blended-finance-principles/.

[20] OECD (2021) Mobilising institutional investors for financing sustainable development in developing countries

[21] Institutional investors that wish to participate in collaborative engagement need to understand any potential regulatory requirements that their collaborative efforts may trigger in some jurisdictions. For example, see Acting in concert and collaborative shareholder engagement, South Africa.