By Julia Anna Bingler, ETH Zurich, Mathias Kraus, University of Erlangen-Nuremberg and Markus Leippold, University of Zurich

The Task Force for Climate-related Financial Disclosures (TCFD) recommendations, and the voluntary disclosures they have led to, have been hailed as an effective measure of climate risk.

But many of the companies purporting to support the TCFD recommendations do so on a selective basis, often re-structuring existing information to fit the TCFD framework and cherry-picking what they report against based on the categories that require the least material disclosures.

Our paper, Cheap Talk and Cherry-Picking: What ClimateBert has to say on Corporate Climate Risk Disclosures, explores whether voluntary reporting has enough bite to effectively initiate a change in climate-risk disclosures, or if it needs to be made mandatory.

Supporting the TCFD to signal climate awareness

Published in 2017, the TCFD recommendations aim to achieve two goals: first, to enhance climate risk understanding, assessment, and management within institutions. Second, to improve disclosure of key climate risk information, allowing financial actors to account for these risks when assessing their investees and their lending and underwriting counterparties.

The TCFD recommends structuring the disclosures around four complementary categories – governance, strategy, risk management, and metrics and targets. Governance and risk management are about qualitative, structural, and process-related information, while metrics and targets and strategy cover specific qualitative and quantitative material information on actual and potential future downside risks and opportunities.

The latter categories are especially relevant for third parties. Without appropriate disclosures on strategy and metrics and targets, investors cannot properly assess and quantify their own current and future risk exposures towards the disclosing entity.

Today, more than 2000 companies and associations have officially endorsed the TCFD recommendations – supporting them has become a popular way for firms to signal to investors and stakeholders their preparedness for the challenges posed by climate change.

But does TCFD support really lead to enhanced climate risk disclosures, and as a result, to better climate risk management?

Analysing TCFD disclosures using ClimateBERT

We trained a context-based algorithm, ClimateBERT[1], to identify and extract climate-related financial information in company filings and reports, differentiated by the four TCFD categories – a task typically associated with immense manual work.

We trained it on more than 17,000 human-labeled sentences with climate risk content from company reports and more than 300,000 general language sentences from annual reports.

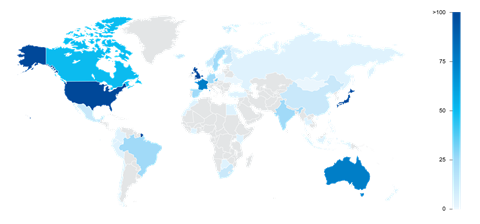

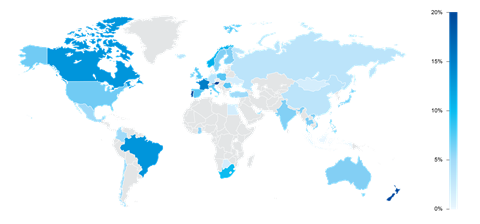

We then applied ClimateBERT to a sample of annual reports from more than 800 TCFD-supporting companies over the last six years, to assess whether climate disclosures improved after supporting the TCFD.

We explicitly included data that predates the introduction of the TCFD recommendations to create a baseline from which to analyse the development of disclosures by TCFD supporters, enriching the findings of the TCFD’s own status report by applying a quantitative measure instead of a simple yes/no assessment.

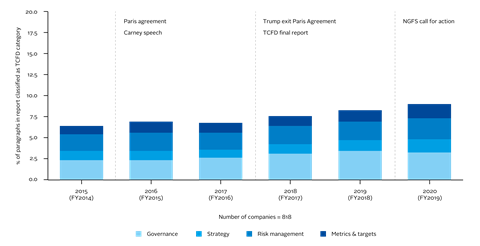

Overall, we observed only a slight increase (approximately 1.9 percentage points) in the information disclosed after the launch of the recommendations in 2017, until 2020.

Most of this was due to increased governance and risk management disclosures. Disclosures on strategy, and metrics and targets, are particularly low for all sectors except energy and utilities. These two categories are essential for assessing risk materiality, i.e., whether a firm is more or less exposed and whether it has an appropriate strategy to deal with the anticipated risks.

Our analysis reveals a much lower quantitative increase in information compared to the TCFD’s estimated 6.0 percentage point-increase in its assessment of whether firms (supporters and non-supporting companies) provide TCFD-aligned disclosure.

Since disclosures did not considerably increase, our findings suggest that TCFD-supporting firms might have simply re-structured existing information to comply with the recommendations.

As such, supporting the TCFD seems to be cheap talk, with companies cherry-picking which disclosures to make based on the TCFD categories that require the least materially relevant information.

Time for mandatory climate reporting

Given our findings, does voluntary reporting have enough bite to effectively initiate a change in climate-risk disclosures, or should climate disclosures be made mandatory?

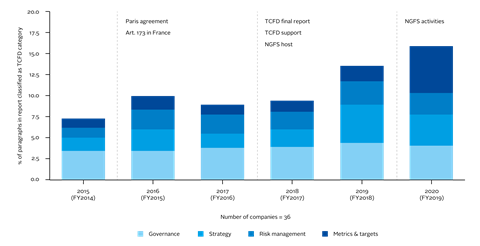

France provides a good example – since the implementation of Article 173 of the French Energy Transition Law in 2016, it is the only country with detailed mandatory climate-risk reporting for large financial institutions in force.

This is reflected in a much higher level of overall disclosures, and more importantly, a much more prominent representation of the strategy and metrics and targets categories as of 2020.

As such, converting voluntary reporting into mandatory disclosure requirements may resolve the issue of cheap talk and cherry-picking. Some countries are in the process of doing this already – New Zealand, the UK, and Switzerland have implemented or announced that they will implement mandatory TCFD reporting, while the EU is aligning its regulations, and the US might follow soon.

We plan to make ClimateBERT publicly available, so that financial analysts, policymakers, financial supervisors and other stakeholders can use it to track the amount and development of climate risk disclosures, particularly when mandatory requirements are introduced. We are also working on an updated version, ClimateBERT 2.0, to further home in on greenwashing.

Find out more about the PRI’s response to TCFD reporting by reading Climate reporting to the PRI, Climate change snapshot 2020 and climate change related activities.

This blog is written by academic guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase research in support of our signatories and the wider community.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected]

References

[1] ClimateBERT is based on the BERT (Bidirectional Encoder Representations from Transformers) model, a deep neural network currently seen as the state-of-the-art method for many tasks in natural language processing.