By Emirhan Ilhan, Zacharias Sautner and Grigory Vilkov, Frankfurt School of Finance & Management

Scientists broadly agree that strong regulatory actions are needed to avoid the potentially catastrophic consequences of climate change. Climate change is mostly caused by the combustion of fossil fuels, so any regulation will have to aim at significantly curbing firms’ carbon emissions. However, whether, how, and when regulatory climate policies will be implemented is highly uncertain. Regulation to limit carbon emissions could be enforced via carbon taxes, cap-and-trade schemes, or emission limits, all of which have different impacts on firms. Even in the case of carbon taxes, it is highly uncertain what the price for carbon emissions should be. Climate policy uncertainty is further amplified by a fundamental lack of clarity about how strongly emissions must be reduced to limit global warming.

Climate policy uncertainty has varied effects across firms in the economy. Uncertainty is likely to be most relevant for carbon-intense firms, as such firms will be most affected by policies that aim to curb emissions. For such firms, regulation that limits carbon emissions can lead to stranded assets or a large increase in the cost of doing business. Carbon-intense firms may also experience financing constraints if banks reduce funding because of climate-related capital requirements. Yet the timing and the extent to which carbon-intense firms will be affected by regulation is highly uncertain. This makes it difficult for investors to quantify the impact that future climate regulation will have on firms, in terms of large drops in stock prices or general increases in volatility.

A new policy is more likely to be adopted if its positive impact on firms’ profitability is higher and if the political costs associated with it are lower. Different policies will affect firms in unique ways and with varying degrees of uncertainty. The uncertainty about a new policy is only fully resolved when it is adopted, but political events (e.g., the 2015 Paris Agreement or the 2016 US presidential election) contain valuable information for investors about whether, how, and when future climate policies would be implemented. For this reason, insurance against tails (i.e., extreme events) should be more expensive when general political uncertainty is higher.

In our paper, we test whether climate policy uncertainty is priced in the option market. Specifically, we explore whether the cost of option protection against downside tail risks is larger for firms with more carbon-intense business models. Options-based measures provide a good reflection of market participants’ future expectations of subjective and perceived risk.

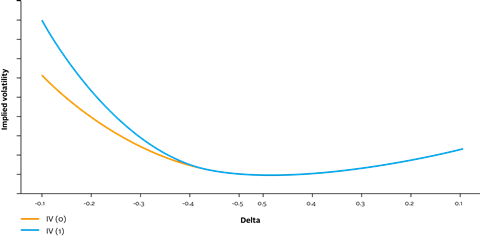

Our analysis is performed for S&P 500 firms and for the economic sector components of the index. Our main option market measure, SlopeD, identifies downside tail risk. It reflects the steepness of the implied volatility slope and is on average positive, since far out-of-the-money (OTM) put options are typically more expensive (in terms of implied volatilities). An increase in SlopeD indicates that deeper OTM puts become more expensive, which reflects a relatively higher cost of protection against downside tail risks. We focus on measures constructed from options with 30 days to maturity.

An illustration for the SlopeD measure is provided in Figure 1. Options with deltas to the left of -0.5 are OTM puts, while options to the right of 0.5 are OTM calls. A shift from IV(0) to IV(1) makes deep OTM puts more expensive in implied volatility terms. Therefore, SlopeD is higher for IV(1) than for IV(0), indicating a higher cost of downside protection.

Our main measure is the natural logarithm of a firm’s industry carbon intensity, which we calculate as Scope 1 emissions of all reporting firms in the industry divided by the market value of all reporting firms in the industry. We use this measure in our tests because:

i) carbon intensities are primarily driven by industry characteristics; and

ii) recent evidence also indicates that industry characteristics drive investor screening and the sensitivity of stock returns to Scope 1 emissions.

We find strong evidence that climate policy uncertainty is priced in the options market. A one-standard-deviation increase in a firm’s log industry carbon intensity increases the implied volatility slope (SlopeD) by 0.014 (10% of the variable’s standard deviation). We confirm our finding for sector exchange-traded fund (ETF) options. Overall, our estimates suggest that options written on carbon-intense firms are relatively more expensive, as they provide protection against downside tail risks associated with climate policy uncertainty.

We also investigate whether the effect of carbon intensities on downside tail risk is amplified when public attention to climate change is high. Our underlying assumption is that high public attention to global warming increases the probability that pro-climate policies are adopted, due to public scrutiny. Importantly, as a policy change becomes more likely, so does uncertainty about which specific new policies will be selected and what their impact on firm profitability will be.

While this implies more certainty that a regulatory change will occur, pro-climate policies are characterised by large uncertainties in terms of their impact on firm profitability, as such policies represent larger deviations from current practices. The cost of option protection against downside tail risk should therefore be magnified at times when public attention to climate change spikes. We find that the effect of carbon intensities on SlopeD is aggravated when there is more negative climate change news.

Finally, we use the election of President Trump in 2016 as a shock that reduced climate policy uncertainty in the short term. The 2016 US presidential election produced a significantly unexpected outcome for the market and it featured two candidates with opposing views on climate regulation. President Trump signalled in his campaign that prevailing climate policies would not become stricter; on the other hand, his opponent Hillary Clinton promised pro-climate policies. Hence, President Trump’s election meant little change in the status quo of US climate regulation, whereas Clinton’s election would have implied the opposite if she were elected. The cost of insurance against downside tail risks associated with climate policy uncertainty should therefore have declined after President Trump’s election, especially for carbon-intense firms – indeed, SlopeD for highly carbon-intense firms decreased by 0.025, relative to less carbon-intense firms – a decline equal to 12% of the SlopeD’s standard deviation during the event window.

Our paper is available for download here.

This blog is written by academic guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase research in support of our signatories and the wider community.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected].