The cost of bribery and corruption is immense.

Every year, corruption losses represent over 5% of global GDP (US$2.6 trillion) and bribes exceed US$1 trillion. This is a cost which can be brought to bear on companies and their investors, and one that is detrimental to governments and society. Corruption adds up to 10% to the cost of doing business globally and up to 25% to the cost of procurement contracts in developing countries.

Corruption is best understood as a shorthand reference for a wide range of activities that encompasses bribery as an important subset. Corruption scandals including bribery, fraud, rate and test rigging, can prove catastrophic to companies, as shown below.

| Company | Estimated losses (US$) | Date | Scandal | Impact |

|---|---|---|---|---|

| WorldCom | 107 billion | 2002 | Accounting fraud |

the biggest bankruptcy in US corporate history; 20,000 workers lost their jobs |

| Volkswagen | 87 billion | 2015 | 11 million cars worldwide fitted with a so-called “defeat device” that ran the car below normal power and performance when an emission test was occurring | impact of corruption scandal still unfolding; significant damage to Volkswagenfs brand and the wider automotive sector |

| Enron | 74 billion | 2001 | Accounting fraud | largest corporate bankruptcy in US history until WorldComfs bankruptcy; 5,000 workers lost both their jobs and the majority of their pensions which were invested in Enron stock |

| Petrobas | 21 billion | 2015 | Alleged diversion of billions of dollars from company accounts for their executives use, or to pay off officials | impact of this corruption scandal is still unfolding; significant damage to Petrobrasfs brand and to Brazilfs image as a destination for investment; service providers have downgraded the companiesf credit rating |

| Various international banks | 9 billion (in fines) | 2012 | Manipulation of LIBOR interest rate benchmark | fines and other prosecutions; public loss of confidence may drive down the wider finance industry profits for years |

| AIG | 3.6 billion | 2005 | Accounting fraud | largest quarterly loss in 2008; bailed out by US tax payers |

| Siemens | 3 billion | 2008 | Payment of bribes for contracts | significant loss of trust; focus on improvements appear to have helped rebuild the companyfs reputation |

| Olympus | 1.7 billion | 2011 | Accounting fraud | cut 2,700 jobs; scrapped around 40% of its 30 manufacturing plants globally (It is unclear how much of this restructuring was as a direct result of the corruption scandal). |

Furthermore, companies embroiled in corruption scandals can suffer from:

- damage to brand, reputation and share price;

- exclusion from potential business opportunities;

- liability to pay hefty fines;

- diversion of significant senior management time away from running the business to manage investigations and prosecutions. This is especially the case with Non Prosecution Agreements (NPAs) and Deferred Prosecution Agreements (DPAs).

Investors in turn risk reputational damage as well as reduced returns if they invest in companies that are implicated in corruption, particularly if the resultant scandal is poorly managed by the portfolio company.

Institutional investors’ fiduciary duty to act in the best interests of their beneficiaries means that they should encourage existing or prospective investee companies to have policies and practices that will reduce uncertainty over long-term returns.

Effective implementation of anti-bribery and corruption standards is not only a risk preventative or remedial measure, but can advantage businesses by increasing the size of the market too. For example, companies will benefit by receiving more revenue for products sold if money ‘leaked’ through corruption can be eliminated or significantly reduced from the purchasing process.

The regulatory risk is increasing across jurisdictions

Since 2010 the UK Bribery Act requires companies to demonstrate their provision of “adequate procedures” to prevent bribery (see Appendix B), and introduced strict penalties for offending individuals and companies alike. This legislation was a significant development for corporate liability, placing a greater burden of proof on UK companies operating abroad, as well as foreign companies doing business in the UK.

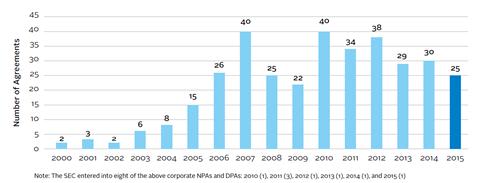

In the US, the use of non-prosecution agreements (NPAs) and deferred prosecution agreements (DPAs) has significantly increased in the last fifteen years and similar approaches are now being adopted in other countries. For example, in November 2015 the UK Serious Fraud Office (SFO) agreed their first DPA, and indicated that the “landmark DPA will serve as a template for future agreements… it also endorses the UK SFO’s contention that the DPA in this case was in the interests of justice and its terms were fair, reasonable and proportionate.” Other OECD countries and emerging markets are following the US’s lead in prosecuting international companies.

With the rapid development of new and tougher regulations on anti-bribery and corruption around the world and following the publication of the Yates Memo by the US Department of Justice in 2015, enforcement is increasingly likely to lead to criminal prosecution and imprisonment for individuals deemed culpable.

Deferred Prosecution Agreements

Under a deferred prosecution agreement (DPA), the US Department of Justice files a charging document with the court. It simultaneously requests that the prosecution be postponed to allow the company to demonstrate its good conduct. DPAs generally require a defendant to:

- agree to pay a monetary penalty;

- waive the statute of limitations;

- cooperate with the government;

- admit the relevant facts;

- enter into certain compliance and remediation commitments, potentially including a corporate compliance monitor.

Non-Prosecution Agreements

Under a non-prosecution agreement (NPA), the US Department of Justice maintains the right to file charges but refrains from doing so to allow the company to demonstrate its good conduct during the term of the NPA. Unlike a DPA, an NPA is not filed with a court but is instead maintained by the parties. The requirements of an NPA are similar to those of a DPA, and generally require:

- a waiver of the statute of limitations;

- ongoing cooperation;

- admission of the material facts;

- compliance and remediation commitments;

- payment of a monetary penalty.

There is an increased appetite in the international business community and beyond

Companies wanting to avoid risks to financial performance need robust anti-bribery and corruption policies and implementation mechanisms. Good governance attracts and retains ethically-oriented employees and builds trust between companies, consumers and other stakeholders. Companies that prioritise the right measures will be better placed to attract long-term capital from responsible investors. They will also be more likely to become the preferred partner for consumers who value ethics and transparency. All these reasons contribute to an increased appetite for stronger anti-bribery and corruption systems within the international business community.

The global profile of the economic and social costs of corruption has been further increased with the launch of the United Nations Sustainable Development Goals (SDGs). SDG 16 calls for “peace, justice and strong institutions” and indicator 16.5 explicitly asks signatories to “substantially reduce corruption and bribery in all its forms.” Companies are increasingly moving to integrate the content of the goals in their long term business strategies, and the private sector will be crucial to achieving the SDGs. Companies that implement the UN Global Compact’s 10th Principle against corruption – through a commitment and implementation of anti-bribery and corruption policies and practices, can also find themselves in a better position to address corruption issues and move forward toward advancing SDG 16.

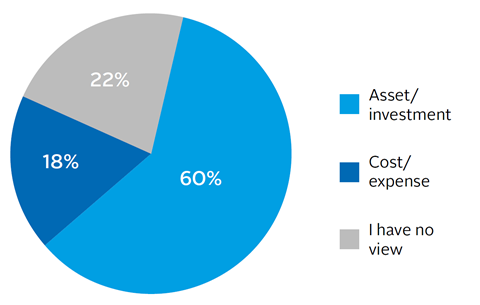

A majority of companies surveyed as part of a recent OECD study viewed money allocated to business integrity improvements as an investment rather than an expense. This is yet another indicator that companies see anti-bribery and corruption policies and implementation as more than just a preventative measure.

An opportunity for investors and companies to showcase their leadership

Dialogue with shareholders allows companies to showcase their leadership in this area, and demonstrate how they implement related programmes, building further legitimacy and trust with investors. This creates a competitive advantage for the company and helps strengthen its ability to generate long-term financial returns. Through dialogue, companies learn about new and evolving investor expectations, and global trends on anti-bribery and corruption and governance issues.

Both one-to-one and collaborative engagement (see definition below) enable companies to gather a more specific understanding of what investors are seeking in terms of transparency on anti-bribery and corruption policies and practices, as well as identifying any potential gaps that need to be addressed.

Investors, there is strength in numbers

Collaborative engagement is when a group of investors work together to approach investee companies on environmental, social and corporate governance (ESG) issues of concern. The PRI-led engagement which ran from 2013-2015 took this format, and benefits to this approach include:

- reduced cost of engagement;

- lower barriers to entry to access companies;

- boosted potential impact by sharing understanding of companies, engagement strategies and regional and sector expertise.

Downloads

Engaging on anti-bribery and corruption

PDF, Size 1.91 mb

Engaging on anti-bribery and corruption

- 1

Currently reading

Currently readingWhy engage? The business case

- 2

- 3

- 4

- 5

- 6

- 7

- 8