Understanding beneficiaries’ ESG and sustainability preferences is of increasing importance to asset owners.

The PRI has researched how beneficiary preferences have been understood to date and how our signatories seek to improve their understanding of this topic. A total of 14 signatories, primarily asset owners, have shared their views, including leading practices to follow, challenges they encountered and how these may be overcome.

This guide seeks to help asset owners learn about and incorporate beneficiary preferences, which should be a fundamental aspect of an asset owner’s investment strategy, policy and strategic asset allocation.

There are two sections to this guide:

Why incorporate beneficiary preferences? What is prompting asset owners to seek out and incorporate preferences, what are the benefits of doing so and what is known about preferences to date.

How to understand and align with beneficiary preferences

A four-step process for understanding the core values with which beneficiaries wish investments to be consistent and how asset owners can deliver.

Alongside this guide we have published a survey template which signatories can modify to fit their purposes and use to gather beneficiaries’ views.

Why incorporate beneficiary preferences?

Beneficiaries are major suppliers of capital that allow the financial system to function and the field of responsible investment to exist. It is paramount that investors understand their true interests and place them at the centre of investment decision-making. While beneficiary interests have often been interpreted as solely being about seeking a certain financial return, it has become clear that many beneficiaries have preferences related to the sustainability performance of their investments. They are also increasingly aware that these investments affect them in other capacities: as employees, consumers, community members and citizens.1

Increasing consultation with beneficiaries has been driven by several factors: an evolving regulatory landscape; an increased acknowledgment among asset owners that investments should reflect the values of their beneficiaries; the benefits realised by asset owners in doing so; and awareness among beneficiaries of the role and power their savings play in the world, informed by media coverage and campaigns.2

This shift presents asset owners with a significant opportunity to improve the satisfaction and engagement of beneficiaries by aligning investment practices with beneficiary preferences, thereby building a virtuous cycle where both parties see the benefits of engagement.

Regulatory trends

It is not yet commonplace for asset owners to be required to proactively incorporate the preferences of beneficiaries in their strategy or decision-making. However, recent trends indicate that greater consideration of beneficiaries’ preferences and holistic interests are likely to be a focus of sustainable finance policy going forward.

For example, as of 2019, the UK’s Investment Regulations require trustees of trust-based occupational pension schemes to specify the extent (if at all) to which they consider members’ views on non-financial matters, including sustainability, when it comes to the selection, retention and realisation of investments.3 A similar expectation is in place for the Independent Governance Committees of contract-based pension schemes.4 The Pensions Regulator expects trustees of defined contribution plans to take regular steps to “consider any information provided when determining investment options to offer to members and strategies for the scheme [including] preferences for particular approaches to investment (e.g. sustainable funds)”.5

Beneficiary preferences are also an increasingly common feature of voluntary stewardship codes. The UK and Japanese Stewardship Codes encourage signatories to consider beneficiaries’ interests and preferences. The CRISA Code in South Africa also encourages investors to engage with ultimate beneficiaries to “identify and understand information requirements”.

Within the EU, the European Securities and Markets Authority currently considers it “good practice” for investment firms to collect information on clients’ ESG preferences.6 Draft provisions of Solvency II, MiFID II and the Insurance Distribution Directive would require relevant entities to obtain the sustainability preferences of clients and potential clients and to offer products compatible with those preferences.

Benefits of incorporating beneficiary preferences

Engaging with beneficiaries on their preferences provides asset owners with the opportunity to improve beneficiaries’ understanding and perception of their investments, demonstrating how beneficiaries’ savings interact with their everyday lives and the positive outcomes to which those savings may contribute.

Particularly among pension funds, there is often a lack of engagement from beneficiaries with their retirement savings. Research indicates that the main reasons members give for their lack of interest include “pensions are too complex”, “pensions are boring”, “there are more urgent priorities”, and a general distrust of the finance industry due to negative media coverage.7 One interviewed pension fund emphasised the “development of a narrative of positive impact that resonates with beneficiaries” as one of the most valuable outcomes of better understanding beneficiary preferences.

Table 1: Benefits of engaging beneficiaries on their preferences

| Driver | Description |

|---|---|

|

Beneficiary satisfaction |

Many asset owners see understanding beneficiaries’ sustainability preferences as critical to building trust and maintaining social licence as fiduciaries, and an opportunity to increase the satisfaction and pride that beneficiaries feel regarding their savings and who is managing them. |

|

Increased contributions |

Better alignment with beneficiary preferences can lead to beneficiaries’ increased understanding of an investment’s positive impacts. As a result, beneficiaries may be more inclined to contribute additional monies to their investments, seeing it as a win-win. |

|

Competitiveness |

Many asset owners point to their beneficiary engagement as a competitive advantage, enabling them to appeal to beneficiaries who value sustainability as well as those who want a voice in how their savings are invested. |

|

Changes and trends |

Beneficiary sustainability preferences can reflect consumer preferences, which can have knock-on effects on investee companies. Activities that seek to understand beneficiary sustainability preferences are important in alerting asset owners to emerging sustainability themes and trends. |

|

Reputational risk |

Campaigns are increasingly targeting asset owners relating to their investments and their impact on the world. Consulting beneficiaries and addressing their concerns provides a strong defence to specific campaigns. |

|

Beneficiaries’financial literacy |

ESG issues can be used to educate beneficiaries on how their investments work and improve their financial literacy. This can improve their ability to make other decisions about their investments and reduce their susceptibility to scams and predatory practices. |

Evidence of sustainability preferences

Beneficiary interest in sustainable investment has “increased significantly” in recent years.8 Various surveys globally indicate that beneficiaries increasingly expect their money to be invested responsibly and, in some cases, express a willingness to forego financial returns to achieve sustainability impact.

Sustainability preferences around the world:

- In 2019, the UK’s largest ever survey on sustainable investing found 68% of savers want their investments to consider the impact on people and the planet alongside financial performance.9

- Two academic surveys saw 68% of respondent beneficiaries of a Dutch pension fund voting for intensified engagement based on the Sustainable Development Goals (SDGs). A majority of those who believed this would lead to lower financial returns still opted for the change.10

- A survey in the aftermath of the 2019-20 Australian fires found 4 in 5 Australians would like their super fund and banks to communicate the positive and negative outcomes of investments and savings.11

- A 2020 survey found 60% of New Zealanders would be motivated to save and invest more money to make a positive difference to the environment and society.12

- The median participant in a recent US study preferred a more sustainable fund option even if it meant sacrificing a 2.5% annual return.13

- A study found low levels of awareness regarding responsible investing of pension funds in Japan, but greater favourability among informed savers towards responsible investing.14

- A 2015 YouGov global survey commissioned by the PRI found over 90% of beneficiaries in Brazil and South Africa supported responsible investment, while most beneficiaries in these regions deemed it “very important” that their pensions were not invested in fossil fuel companies.15

Asset owners interviewed for this guide said beneficiaries are consistently in favour of considering sustainability factors and want more information on responsible investment. Many of these asset owners also seek beneficiaries’ views on their priority ESG issues: climate change is the most consistently cited issue, followed by human rights and labour rights. Traditional focuses of values-based screening, such as tobacco companies, are less prominent, though still a concern for some beneficiaries.

How to understand and align with beneficiary preferences

This section sets out the main methods for building an understanding of beneficiary preferences and how these preferences can be incorporated into investment practices.

Figure 1: The virtuous cycle of beneficiary engagement

Before entering an engagement process with beneficiaries, asset owners should understand what information they are seeking to obtain and communicate, and what changes to investment practices they are prepared to make in response to beneficiary feedback. Objectives may include:

- ensuring that investments are aligned with the values and interests of beneficiaries;

- improving beneficiaries’ financial literacy and ability to make decisions about their savings;

- communicating and explaining the asset owner’s responsible investment beliefs.

Interviewed asset owners emphasised the importance of making clear to beneficiaries that the investment committee and/or board will ultimately make any investment decisions, but beneficiary preferences can influence those decisions.

Fiduciary duties will dictate asset owners’ ability to act upon beneficiary preferences. For financially material ESG issues, preferences may be a consideration when considering which issues should be prioritised, for example, in an investor’s proactive stewardship activities. Scepticism from beneficiaries will generally not justify neglecting a source of long-term risk such as climate change, particularly where the issue is likely to affect future beneficiaries whose preferences cannot yet be obtained.

Different jurisdictions allow varying levels of flexibility to further incorporate preferences. Beneficiary preferences may act as a tie-breaker in investment decision-making where competing investments serve a plan’s economic interests equally well.16 Beneficiaries may also wish for certain sustainability outcomes to be achieved; some asset owners may seek to align with sustainability performance thresholds provided it does not risk significant financial detriment.17

The PRI’s Legal Framework for Impact, to be published later in 2021, will set out the extent to which investors are permitted or required to integrate sustainability impact in decision-making and will make recommendations for policy change.18

Research suggests that many beneficiaries are unaware that their savings are invested in the real economy, and that these investments can influence outcomes in the real world.19 Asset owners should therefore consider the level of knowledge their beneficiaries are likely to have on the mechanics of their investments and responsible investment, and whether any engagement with beneficiaries on their preferences should be paired with or preceded by an educational aspect.

In seeking to understand beneficiary preferences, there are four methods asset owners can deploy:

- Surveys, focus groups, interviews: Through proactive methods, asset owners can seek out specific and useful information on beneficiary preferences while improving beneficiaries’ knowledge and engagement levels.

- Beneficiary representation: By allowing beneficiary representation on trustee boards or relevant committees, beneficiaries’ preferences and concerns can be integrated regularly into decision-making.

- Research and data analysis: Pairing existing third-party data on public preferences on sustainability issues with demographic and other data about beneficiaries can enable an asset owner to make reasonable assumptions about their beneficiaries’ preferences at a low cost.

- Beneficiary requests and campaigns: Proactive communication from beneficiaries and organised campaigns can be a source of information on beneficiary preferences and priority issues.

A best practice approach may include a combination of inputs. For example, one interviewed asset owner surveyed its beneficiaries to understand their level of knowledge on responsible investment issues and their preferences. This was followed by a two-week sustainability forum comprised of a series of events that took beneficiaries on a journey from providing a basic understanding – “your pension is invested in companies” – to understanding beneficiary preferences on complicated issues such as, “Do you believe in a divestment or engagement approach?”

Figure 2: Methods of understanding beneficiary preferences

Table 2: Challenges and solutions of engaging with beneficiaries

| Challenges | Solutions |

|---|---|

|

Low levels of beneficiary engagement |

|

|

Low levels of financial literacy and knowledge gaps |

|

|

Inadequate data or unrepresentative sampling |

|

|

Insufficient capacity to engage |

|

|

Interpreting feedback – there is no clear consensus among beneficiaries |

|

Surveys, focus groups and interviews

Surveys are particularly useful for providing quantitative information on beneficiaries’ preferences and financial literacy. Surveys have low barriers to participation, and as such are more likely to provide a representative sample of the beneficiary base.

A template for a beneficiary survey is available here.

Table 3: Tips for designing a survey to understand beneficiaries’ preferences

| Survey practice tip | Explanation |

|---|---|

|

Include an educational introduction |

Give beneficiaries background information on what the engagement is about, why you are seeking their input and what you plan to do with the information you obtain. Consider also providing information on current responsible investment policies and past engagement successes. |

|

Clarify expectations |

Surveys should be clear that while beneficiary preferences will be used as a key input into decision-making, discretion must ultimately reside with investment professionals as to whether and how these preferences will be implemented. |

|

Avoid leading questions |

Avoid questions that begin with a statement indicating a pre-existing position: this can bias the beneficiary’s response. Similarly, avoid sequencing questions that may nudge responses in certain directions. |

|

Avoid jargon |

Use everyday language and avoid jargon. For example, the term “responsible investment” has been found to resonate better with pension beneficiaries than “”environmental, social and governance investment.”21 |

|

Aim to obtain a representative sample |

Avoid approaches that are likely to attract only highly engaged beneficiaries or a specific demographic. Disseminate the survey through multiple channels to increase the likelihood of reaching a range of beneficiaries. If particular demographic groups are not represented in initial outreach, consider a targeted approach for such groups. If you are unable to get a broad sampling of respondents, the engagement can still be used as a qualitative input. |

While surveys can provide high-level quantitative information from a wide range of beneficiaries, other approaches such as focus groups and one-on-one interviews can supply more in-depth, qualitative information. These can be standalone engagement tools or a complement to a survey, providing context to understand quantitative results.

Focus groups are typically composed of 10-12 participants. They discuss the topic with a facilitator who leads the conversation but remains neutral to ensure beneficiaries provide their honest opinions. Focus groups can enable beneficiaries to reach a common position by consensus.

One-on-one interviews are focused on a beneficiary’s reflections without external influence.

Both approaches allow for open-ended information gathering rather than starting from a hypothesis. They also allow for idea generation, a testing of multiple scenarios and are an opportunity to educate beneficiaries and see how this education affects their preferences in real time.

- Define key objectives early to help inform the type and structure of engagement.

- Allow third-party service providers to assist in designing a survey or facilitating qualitative engagement.

- Use a combination of qualitative and quantitative approaches where possible.

Beneficiary representation

In certain circumstances, a representative governance model can support trustees, existing governing bodies and investment decision-makers in incorporating beneficiaries’ interests.

Beneficiary representation can take place through the governing board, investment committee or the creation of beneficiary panels22 where beneficiaries can provide insights on important issues and asset owners can test their understanding of beneficiary preferences. Such an approach is common practice in Canada, South Africa, parts of Europe and Latin America, and amongst some superannuation funds in Australia, where member representatives constitute up to half of the trustee board.

Another approach can be a beneficiary Annual General Meeting (AGM), which is common practice among Danish pension funds. Through this forum, beneficiaries can submit (non-binding) proposals in advance, which the beneficiary base vote on, in-person or by letter, and those attending the AGM can put questions directly to the trustee board and administrators. Beneficiary AGMs are promoted heavily through various communication channels and often see several hundred members attend.

Industry practice tips

- Ensure that appointed representatives reliably portray beneficiaries’ sustainability preferences. Consider the experience of the representative(s) in the sector, their position, exposure to other beneficiaries on a regular basis, and membership of common groups such as industry trade unions.

- Communicate widely who the member representatives are, what they do and how they can be contacted.

- Establish online and offline spaces where beneficiaries can come together and exchange views, submit resolutions and potentially converge on a common position.

Research and data analysis

For asset owners who are unable to undertake the beneficiary engagement methods set out above, utilising existing third-party research on preferences of the general public (or more narrowly defined groups) is a low-cost step to building an understanding of beneficiary preferences. Industry associations are also likely to have research that may shed light on the most common preferences, particularly amongst specific demographics.23 Care should be taken that research used is reliable and objective.

Such research can be combined with existing data that asset owners may possess with respect to their beneficiaries, allowing asset owners to identify unique characteristics of their beneficiaries and make more informed decisions about likely preferences. For example, where a large proportion of beneficiaries are low paid, they may be more likely to favour engagement on living wage issues and decent work. Where beneficiaries are disproportionately young, they may be more likely to favour affordable housing.24 Beneficiaries in the healthcare profession may be more likely to oppose investments in tobacco companies.25

Caution is however required to ensure that asset owners comply with privacy laws, and that they obtain informed and express consent of the individuals involved, as well as provide clarity on how the beneficiaries’ information will be used.

Beneficiary requests and campaigns

Asset owners are increasingly subject to proactive requests and organised campaigns by activist groups and public interest organisations, which can sometimes include significant proportions of beneficiaries. Campaigns can take the form of petitions (such as change.org), social media and email-targeting campaigns, and publicly visible activities such as protests.

Such targeting may be the symptom of a misalignment between the current investment practices of an asset owner and their beneficiaries’ preferences and may be a source of reputational risk.

Beneficiary requests and campaigns can reveal emerging ESG issues that have been omitted from a responsible investment policy. Public sentiment can evolve rapidly and being receptive to these concerns can allow investors to anticipate changes in corporate behaviour or public policy with respect to issues such as racial justice, labour rights or corruption. At a minimum, beneficiary requests and campaigns can be indicative of the need for an asset owner to be more communicative and transparent regarding its responsible investment approach, as well as highlighting educational gaps and potential misconceptions that should be addressed.

Asset owners should ensure they are not being unduly influenced by a minority of unrepresentative beneficiaries, though a campaign may be a prompt for proactive engagement with the wider beneficiary base.

Industry practice tip

- A good understanding of beneficiary preferences can assist in interpreting whether campaigns represent broader views.

Evidence of clear sustainability preferences of beneficiaries creates a strong mandate for asset owners to reflect these preferences in the investment strategy. There are several ways in which these preferences may be put into practice, including divesting from certain sectors, dedicating further resources to engagement on priority issues and shaping sustainability outcomes.26

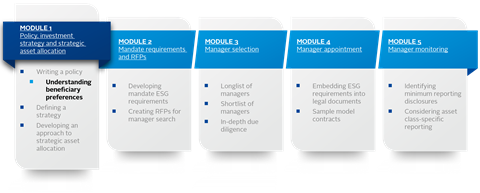

While some asset owners will be able to make the necessary changes to an investment strategy themselves, many will be reliant on investment managers and service providers to support the integration of beneficiary preferences into investment practice. Asset owners should ensure they communicate the key priorities identified from beneficiary engagement to their service providers and embed consideration of beneficiary preferences into the investment manager selection, appointment and monitoring processes.27

Trustees and relevant parties should not take beneficiary preferences as instruction, but rather as a key input into an investment strategy. It falls to asset owners and their service providers to determine the most practical path for achieving these objectives in a manner that is compatible with their fiduciary duty.

Figure 3: Responsible investment approach of asset owners

Investment Allocation

Where beneficiary preferences are substantially aligned on certain issues, the asset owner should use this information to develop and influence a default investment option and/or asset allocation.28 Where beneficiaries strongly express ethical or sustainability concerns, this may give asset owners a basis to exclude, divest or alter sector weightings. Beneficiary preferences on real-world outcomes may provide asset owners with a mandate to intentionally reallocate capital to influence those outcomes. For example, investors may use the strategic asset allocation (SAA) process to prefer portfolios with higher positive SDG outcomes and lower negative SDG outcomes.29 There have been instances where non-financial benefits to beneficiaries’ own communities have been incorporated into asset allocation decisions, for instance the investments by New York City pension funds in local rebuilding efforts after Hurricane Sandy.30

Where there is no or limited consensus among beneficiaries, preferences may be fulfilled through provision of fund options or products (see Benefit and Product Design below).

Stewardship

The PRI defines stewardship as “the use of influence by institutional investors to maximise overall long-term value, including the value of common economic, social and environmental assets on which returns and beneficiaries’ interests depend”. Stewardship can take different forms, including company engagement, voting at shareholder meetings, filing shareholder proposals, direct roles on investee boards and committees, and engagement with stakeholders such as standard-setters and policy makers (see Policy Engagement and Advocacy below).

For asset owners with significant exposure to equity investments, shareholder voting activities provide a clear opportunity to align with beneficiary preferences. Where voting is conducted in-house, the asset owner’s voting guidelines or voting principles should align with preferences, and beneficiaries’ priority issues should explicitly be addressed.31

Asset owners should consider escalation strategies, such as voting against board members or submitting shareholder proposals, where portfolio companies are underperforming on key issues identified by beneficiaries. New technology solutions are emerging that allow beneficiaries to educate themselves on companies they are invested in and express voting preferences for upcoming shareholder votes – that information is fed back to the investor to help inform their decision-making.32

Where voting is undertaken by third parties, such as investment managers or proxy advisers, asset owners should engage with these groups to ensure they are aware of any overarching principles impacted by beneficiary preferences, and that voting is exercised in a manner consistent with preferences. If default voting guidelines prevent substantial alignment with preferences, asset owners should consider developing a custom voting policy with their proxy adviser or exploring whether their investment manager can offer split-voting in pooled fund arrangements.33

Beyond voting, asset owners should use the other stewardship tools at their disposal. Asset owners should identify portfolio companies that perform poorly on ESG or sustainability issues that are important to beneficiaries and engage with these companies. Where these concerns are shared by other investors, engaging collaboratively may be more effective and resource-efficient.

Industry practice tips

- When revising or updating voting guidelines or principles, this may be a timely opportunity to obtain beneficiaries’ up-to-date preferences.

- Asset owners can refer to their experience of beneficiary engagement to show evidence of good stewardship activities, for example under stewardship code reporting.34

Policy engagement and advocacy

Public policy affects institutional investors’ ability to generate sustainable returns, create value and it impacts upon the stability of financial markets. Institutional investors engaging in policy is therefore a natural and necessary extension of an investor’s responsibilities and fiduciary duties to beneficiaries.

Policy engagement may be particularly appropriate where regulation plays a significant role in issues that are important to beneficiaries. For beneficiaries invested in passive investment strategies, policy engagement and advocacy on ESG issues may be the key route to improving long-term returns and real-world outcomes.

Policy engagement and advocacy can take various forms such as responding to public policy consultations, penning open letters, commenting in the media and participating in government working groups. Many asset owners collaborate with others through industry bodies, which asset owners should ensure are aligned with beneficiary preferences on key issues.

The PRI has found that investors significantly underestimate the positive role that the responsible investment industry can play in encouraging policy change. As part of our work with investors in the post-pandemic recovery, the PRI has proposed a seven-part framework that should support investors in pursuing their policy objectives.35

- Undertake policy engagement, aligning engagement and investment objectives.

- Work to the timetable of the policy maker, not the investor.

- Leverage arguments based on technical expertise.

- Engage at all levels of the policy process, as well as through the media.

- As far as possible, work together and speak with a coherent voice, especially where there is consensus.

- Better understand the relevant dynamics of policy decision-making across committees and groups.

- Be clear about who investors represent and how policies impact beneficiaries.

Benefit and product design

In markets where beneficiaries can opt into funds that differ from the default investment strategy, asset owners may offer beneficiaries the chance to move their investments to a product that aligns more closely with their sustainability preferences and financial needs. This is particularly useful in circumstances where beneficiaries are divided on how far their investments should pursue positive outcomes but where a minority of beneficiaries demonstrate a strong appetite for more sustainable investments.

When it comes to the design of investment products that are aimed at beneficiaries which desire more sustainable investments, engagement with beneficiaries beforehand is valuable. This can ensure such a product targets the positive outcomes that are most important to beneficiaries. Beneficiaries should be provided information which allows them to compare the product with the default fund based on financial performance, fees and sustainability outcomes.

Industry practice tips

- Ensure that switching funds is sufficiently straightforward considering the typical inertia of even the most engaged beneficiaries.

- Widely held preferences should be addressed in the default investment strategy wherever possible.

- For dedicated products, include sustainability objectives that are consistent with the preferences of targeted beneficiaries.

Communicating with beneficiaries about the results of an engagement and implementing beneficiary preferences is critical. It will confirm to beneficiaries that participation in any information-gathering activities was worthwhile. It can also contribute to a virtuous cycle where periodic engagement increases the beneficiaries’ sense of ownership over their savings while keeping the asset owner abreast of changing trends and preferences.

Asset owners that engaged with beneficiaries on their preferences consistently reported that beneficiaries:

- need clearer communications and transparency around how their money is invested;

- want more transparent reporting on the outcomes to which their investments are contributing;

- want further information on local community investments, where relevant.

Reporting back to beneficiaries also presents an opportunity to address any knowledge gaps identified in the initial engagement, ensuring that beneficiaries will be better placed to provide more valuable insights in the future.

Downloads

Understanding and aligning with beneficiaries' sustainability preferences

PDF, Size 2.12 mbSurvey Template

PDF, Size 0.38 mb

References

1 RI Quarterly (2014), The voice of the beneficiary

2 For example, https://makemymoneymatter.co.uk/

3 Regulation 2(3) of the Occupational Pension Schemes (Investment) Regulations 2005 (UK)

4 Financial Conduct Authority (2019), PS19/30 Independent Governance Committees: extension of remit

5 The Pensions Regulator, Code 13: Governance and administration of occupational trust-based schemes providing money purchase benefits

6 ESMA, (November 2018) Guidelines on certain aspects of the MiFID II suitability requirements, ESMA35-43-1163; para. 28

7 Pensions Policy Institute and Ignition House, (2015), Transitions to Retirement: Supporting DC members with defaults and choices up to, into, and through retirement), pp.19 to 34

8 Defined Contribution Investment Forum, (2020), The key to unlocking member engagement

9 Department for International Development, (2019), Investing in a better world

10 Bauer, Rob and Ruof, Tobias and Smeets, Paul, (2019), Get Real! Individuals Prefer More Sustainable Investments

11 Responsible Investment Association Australia, (2020), From values to riches 2020: Chartering consumer expectations and demand for responsible investing in Australia

12 Responsible Investment Association Australasia, (2020), Responsible Investment: New Zealand Survey 2020

13 University of Cambridge Institute for Sustainability Leadership, (2019), Walking the talk: Understanding consumer demand for sustainable investing

14 Research Institute for Policies on Pension & Aging, (2018), Research on the Public’s Awareness of ESG Investing of Pension Funds

15 YouGov, (2015), Executive Summary - Responsible Investment

16 See, for example, US Department of Labor, (2020), Final Rule on Financial Factors in Selecting Plan Investments

17 In the UK, for example, pension funds may act on broadly shared beneficiary concerns provided there is no risk of “significant financial detriment”. See Pension trustees’ duties when setting an investment strategy: Guidance from the Law Commission

18 PRI, A legal framework for impact

19 See e.g. Nest Insight, (2020), Responsible investment as a motivator of pension engagement

20 The Law Commission (Law Comm No 350), (2014), Fiduciary Duties of Investment Intermediaries, p.121

21 IPE Magazine, (2019), Should DC schemes drop the term ‘ESG’?; Nest Insight, (2020), Responsible investment as a motivator of pension engagement

22 For example, UK pension fund NEST has a member panel (established by statute) that is consulted on the asset owner’s investment principles

23 See, for example, the studies set out on p.13 of a report from ShareAction, (2018), Pensions for the Next Generation: Communicating What Matters

24https://www.hbf.co.uk/news/new-survey-shows-home-buyers-financial-worries-and-the-changing-attitudes-of-young-people/

25 See, for example, the origins of Tobacco Free Portfolios

26 PRI, (2020), Investing with SDG outcomes: a five-part framework

27https://www.unpri.org/investment-tools/asset-owner-resources

28https://www.unpri.org/investment-tools/asset-owner-resources/strategy-policy-and-strategic-asset-allocation

29 It is important to note that individual investors reallocating capital does not always shape outcomes in the real world – in some cases only changing which outcomes that investor is exposed to. See PRI, (2020), Investing with SDG outcomes: a five-part framework, p.17

30 IPE Magazine, (2013), “New York pension funds to invest $500m in Sandy Redevelopment”

31 PRI (2021), Making Voting Count

32 For example: https://www.tumelo.com/

33 AMNT, (2020), Bringing shareholder voting into the 21st century

34 For example, Principle 6, UK Stewardship Code (“Signatories take account of client and beneficiary needs and communicate the activities and outcomes of their stewardship and investment to them”)

35 PRI, (2020), Sustainable and inclusive: COVID-19 recovery and reform