The credit rating agencies (CRAs) to have signed the PRI’s Statement on ESG in credit ratings vary in size, history and service offering, as well as regional focus:

Global CRAs

This group contains the two largest and most established CRAs: Moody’s Investors Service and S&P Global Ratings.

Progress on ESG: Visible progress in complementing rating analysis with additional research publications on ESG considerations to refine and improve methodologies and transparency.

| MOTIVATION | FOCUS | INTERNAL CAPACITY | TRANSPARENCY | CHALLENGES |

|---|---|---|---|---|

| See signing statement as a reaffirmation of what they were already doing in terms of ESG integration and transparency. Client demand is increasing but still localised. | Publication of papers on how they integrate ESG into their criteria; exploring creation of additional ESG scores; recent research focus is evident primarily on climate change and “green” evaluation. | Expanding: hiring staff with ESG backgrounds as well as equipping existing credit analysts and rating committees with ESG expertise; providing new ESG evaluation tools; expanding analytics and sourcing expertise from third-party providers (e.g. S&P Dow Jones Indices’ acquisition of Trucost plc). | Both CRAs acknowledge there is scope for improvement. | Investor willingness to pay for non-rating ESG-orientated products and services; meeting growing demand for more extensive commentary on ESG issues for issuers beyond current credit ratings. |

Smaller/regional/specialist CRAs

This group represents a sub-set of the regional ones and includes Dagong Global Credit Ratings, China Chengxin and Golden Credit Ratings.

Progress on ESG: Younger; less developed in the publication of working frameworks than the global agencies, but demonstrating strong commitment to incorporating ESG factors as they grow.

| MOTIVATION | FOCUS | INTERNAL CAPACITY | TRANSPARENCY | CHALLENGES |

|---|---|---|---|---|

| Belief in the value of ESG and an interest in satisfying increasing investor demands in this area. | Most still at the development stage of formal measures and using them consistently in all ratings. | Nascent: as an example, a CRA has charged some of its most senior staff to establish a taskforce that will develop the necessary framework, processes, internal capacity and manage their commitments under the statement. | Internal methodologies are generally still being developed and transparency, besides high-level methodology papers, is limited. | As the smaller and regional CRAs are still relying mostly on issuers’ fees, they face more commercial pressure, potentially compromising ESG integration. |

Chinese CRAs

This group represents a sub-set of the regional ones and includes Dagong Global Credit Ratings, China Chengxin and Golden Credit Ratings.

Progress on ESG: Generally consider ESG from a green bond perspective.

| MOTIVATION | FOCUS | INTERNAL CAPACITY | TRANSPARENCY | CHALLENGES |

|---|---|---|---|---|

| Government policy in China has generated significant interest in green bonds and CRAs have responded by developing green bond rating processes. | Almost exclusively on the environmental impact of the projects rated. | Expanding to meet increasing demand for green bond assessment processes. | Remains an issue due to language barriers and significant discrepancies between ratings assigned by local agencies and global agencies for the same issuer (FT, 2017). | One CRA notes that the biggest challenge to its rating process is how to internalise environmental costs. |

ESG factors are not completely new to credit analysis

CRAs highlighted that ESG consideration has always been embedded in their rating analysis. Until recently, however, ESG factors may have not been labelled as such. But this is changing.

“ESG considerations are part of the holistic assessment of credit risk that we undertake for a rated entity. They are an important element in our assessment of an entity’s creditworthiness where they represent a material credit risk.”

Moody’s Investors Service

For instance, they are increasingly mentioned in, or are the focus of, CRAs’ publications. In 2015, Moody’s Investors Services published Environmental, Social and Governance (ESG) Risks – Global: Moody’s Approach to Assessing ESG Risks in Ratings and Research. The same year, S&P Global Ratings published ESG Risks in Corporate Credit Ratings – An Overview.

Since all rated entities operate in the natural and social worlds, we regard these risks as ubiquitous across the ratings spectrum…managing environmental and social risk is included in the business and financial risk profile assessment for corporate ratings, as applicable and when environmental and social risks are ratings significant.”

S&P Global Ratings

Meanwhile, CRAs are responding to growing client demand, although some noted that sensitivity to related issues is more established in Europe and still developing in other regions.

“In our more than 25 years of rating experience, ESG risk factors, where relevant and material, already feature in several of our rating methodologies or rating actions.”

RAM Ratings

The challenge is on disclosure

The main challenge for CRAs is on the disclosure and transparency front, not so much on putting in place an ESG integration framework, which they have already. They acknowledge, though, that there is scope to refine these methodologies, expand analytics and disclosure, as well as their internal ESG expertise and resources, and are working across all these areas.

Moody’s Investors Service has published ESG-related commentary where it sees these risks as material. S&P Global Ratings does this within its Key Credit Factors, which documents how the firm interprets its own general corporate criteria to take into account specific industry dynamics or factors. Key Credit Factors describes ESG risks that could be material to ratings for that industry unless the risks are already covered in management and governance criteria.

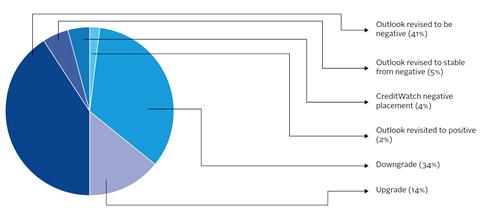

S&P Global Ratings also published a review of its global corporate rating actions since 19 November 2013 to assess the impact of extreme weather events and environmental and climate risks.

In reviewing all 38 corporate subsectors, it identified 299 cases in which these risks have either resulted in (or contributed to) a corporate rating revision, or were significant factors in its rating analysis. In 56 of these cases, environmental and climate risks had a direct and material impact on credit quality, resulting in a rating Outlook or Credit Watch action or adjustment - nearly 80% of which were negative in direction. The lion’s share of these ratings were in the oil refining and regulated utilities, as well as unregulated power and gas sub-sectors.

Both CRAs have published papers outlining their approaches to ESG in their ratings, and have delivered further research and related case studies.

Even younger CRAs – including Liberum Ratings, RAM Ratings and Scope Ratings – are beginning to make progress. For example, RAM Ratings published its first paper, Primer on ESG in credit ratings, in September 2016, and in general is demonstrating strong commitment to incorporating ESG factors as it grows and can commit additional resources.

Systematic ESG consideration

Demonstrating that ESG factors are systematically included in rating assessments is more difficult. Again, this is down to the choice of factors that CRAs deem to be material in their risk analysis.

“ESG factors are analysed at various points in ratings methodology. The incidence of environmental and social risks are most commonly addressed in the business risk profile, for example country risk issues connected with supply chains and the reputational risks that can arise for a rated issuer if the company’s corporate responsibility statements are contradicted by the emergence of contradictory facts. Industry risk and competitive position are the locations for comparative peer analysis on how industry risks are managed by the issuer, along with competitive advantages or disadvantages that arise from management decisions. Management decision making and the effectiveness of board oversight are further reviewed and assessed with the management and governance modifier in our ratings methodology, to ensure that both the incurrence of environmental and social risks and opportunities and their management and oversight by the board of directors receive a comprehensive review.”

S&P Global Ratings, Hazell

ESG in sovereign ratings

The share of government bonds with a AAA rating by the largest three global CRAs has been shrinking since the global financial crisis, as governments in many developed economies have been forced to bail out banks and public finances have been squeezed by weak economic growth. As global recovery has been slow and uneven, highlighting that cyclical as well as structural forces are undermining traditional growth paradigms, it has become even more compelling for investors and CRAs to assess the drivers of potential growth through an ESG lens.

“A sovereign’s economic score would be one category worse if its economic activity were vulnerable due to constant exposure to natural disasters or adverse weather conditions.”

S&P Global Ratings

A country’s competitiveness, its potential growth, governance and political stability are all important ingredients of prosperity as well as critical in reducing vulnerability to shocks and increasing resilience during economic downturns. When these occur, they can be more moderate and short-lived if the social and institutional fabric of a country is strong.

There are many factors to take into account in relation to how ESG considerations feature in sovereign credit: availability and management of resources (including population trends, human capital, education and health), emerging technologies, the distribution of growth dividends, government regulations and policies. Ultimately, what matters from a credit perspective is a government’s ability (and political stability) to generate enough revenues to repay its financial obligations — and it is becoming increasingly apparent that ESG factors may affect this.

| BROAD RATING FACTORS | RATING SUB-FACTOR | SUB-FACTOR WEIGHTING (TOWARDS FACTOR) | SUB-FACTOR INDICATORS | INDICATOR WEIGHTING (TOWARDS SUB-FACTOR) |

|---|---|---|---|---|

| Factor 2: Institutional strength | Institutional Framework and Effectiveness | 75% | Worldwide Government Effectiveness Index | 50% |

| Worlwide Rule of Law Index | 25% | |||

| Worldwide Control of Corruption Index | 25% | |||

| Policy Credibility and Effectiveness | 25% | Inflation t-4 to to t+5 | 50% | |

| Inflation t-9 to t | 50% | |||

| Adjustments to Factor Score | 0=6 scores max | Track Record of Default | 0=3 scores | |

| Others | 0=6 scores |

Download the full report

-

Shifting perceptions: ESG, credit risk and ratings (Part 1: The state of play)

July 2017

The ESG in Credit Ratings Initiative receives financial support from The Rockefeller Foundation

![]()

ESG, credit risk and ratings: part 1 - the state of play

- 1

- 2

- 3

- 4

- 5

Currently reading

Currently readingWhat rating agencies are doing on ESG factors

- 6

- 7

- 8