By Natasha Buckley, senior manager - Private equity, PRI

In July this year, the PRI co-facilitated a workshop with SASB in New York to explore how SASB metrics can support PRI monitoring and disclosure resources for private equity. This is a summary write-up of the workshop - a way of sharing some practical reflections and take-aways with PRI signatories that could not be there in person.

Background

The PRI started the workshop by presenting on the convergence of private equity reporting initiatives over the past five years:

- The ESG Disclosure Framework for Private Equity was a cross-industry initiative that established Limited Partner (LP) objectives for ESG disclosure during (i) fundraising, and (ii) during the lifetime of the fund.

- Building on Section 1 of the ESG Disclosure Framework, the PRI published the LP Responsible Investment Due Diligence Questionnaire; an adaptable list of questions that LPs can give to General Partners (GPs) when fundraising – or GPs can proactively include their responses in their data room or PPM. The PRI LP Responsible Investment DDQ establishes a GP’s intended approach to ESG for their new fund, covering policy, process, resourcing/responsibility and reporting practices; it has been incorporated into the ILPA Due Diligence Questionnaire.

- Building on Section 2 of the ESG Disclosure Framework, the PRI (and its signatories) worked with ERM to develop an ESG Monitoring and Reporting Framework for disclosing ESG information to LPs during the lifetime of a fund – across the three pillars of Policy/People/Process, Portfolio and Material ESG Incidents. By using the framework to collect and organise ESG data, the GP will be able to respond to LP requests for information, and of course the annual PRI Reporting Framework obligation.

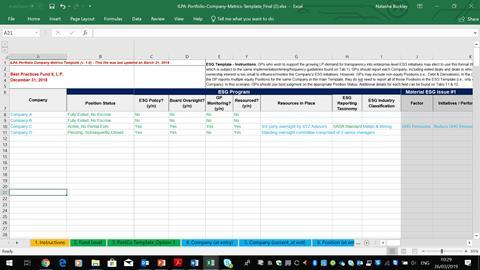

- This year, ILPA published its Portfolio Company Metrics Template which includes a voluntary ESG section. The PRI and its Private Equity Advisory Committee advised ILPA on the construction of this template to ensure alignment with the work that has gone before it. If the GP is following PRI guidelines on reporting, they should have the suggested “framing” data for each portfolio company in place (does it have an ESG/sustainability policy? Is it being monitored on ESG by the GP? Is there resource in place at the portfolio company to implement the policy?).

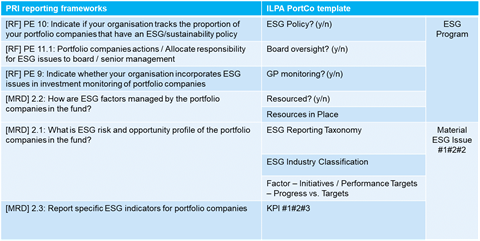

See below a chart that cross references the items in the ILPA template with PRI reporting resources (RF = PRI Reporting Framework, Direct – Private Equity module; MRD = PRI/ERM guidance on ESG monitoring, reporting and disclosure in Private equity – or see one pager):

Where the ILPA template goes further, is to ask the GP to specify the ESG reporting taxonomy being used to monitor ESG data at the portfolio company level – it could be SASB, or a bespoke checklist – and to ask the GP to specify which targets are in place and to record KPIs and objectives for those targets.

All the cross-industry work that has been done so far has been done with the intention to set standards and build a common dialogue whilst streamlining the ESG information exchange between LPs and GPs. The PRI-SASB workshop was an important moment to bring further convergence to this work by discussing how a framework such as SASB can be used to bring the different reporting practices across due diligence, portfolio monitoring and LP reporting together for GPs.

Notes from the workshop

SASB metrics are ESG-specific factors that are deemed to be financially material to the operating performance of companies, according to their industry classification.

Investment due diligence

Workshop participants talked about how relevant ESG factors can be used to enhance the effectiveness of due diligence. In alignment with the PRI-ERM framework for ESG Monitoring and Reporting, SASB presented on the two aspects to this: bottom-up and top-down.

Both LPs and GPs benefit from a bottom-up understanding of the materiality of ESG risks to the portfolio company’s business. Looking at the business through an ESG lens can help with managing the inherent risk of a company’s operating environment, while identifying ESG risks can also offer opportunities to protect or even enhance value.

The idea that identifying risks can offer opportunities works from the top-down perspective too, as both business strategy and business efficiency can be improved by considering ESG issues. A sector-based ESG analysis can help uncover risks and opportunities that might otherwise go unnoticed, while intersecting ESG risks may affect the assessment of investment targets.

Workshop attendees generally agreed that a systematic approach is needed to gather ESG data during due diligence, which may inform the investment decision itself and/or inform the post-investment action plan for the target acquisition.

- GPs agreed that the SASB framework could be used as a starting point for investment due diligence, noting that they appreciated its flexibility and how it can be adapted to bespoke internal frameworks.

- One GP explained how they built a bespoke framework, paring down the SASB materiality indicators to tailor it to the five sectors that their investment strategy focuses on. The GP uses a web-based platform to collect the bespoke datapoints from portfolio companies on an annual basis.

- Another GP explained that they do not have a systematic data collection system in place, but will sit down with target companies and use the SASB risk factors to support broader conventional due diligence.

- Another GP noted that investment due diligence is not the optimal time for them to engage on materiality of ESG factors – apart from the identification of “red flags” (which can be identified using SASB Materiality Map or third party advice) - as it tends to be a rushed process and often does not allow for access to pertinent information. This ESG expert prefers to raise issues during the control phase, when they have the information and the leverage that they need to really work on the issue and extract value from that process.

- A fund of funds said they found the SASB framework helpful for guiding ESG due diligence on co-investment opportunities. They use the PRI LP Responsible Investment DDQ to evaluate the practices of the firm, and the SASB framework to do a deep-dive on the actual investment.

- One GP specialising in private debt said while it was not in a position to influence portfolio companies, they find the SASB framework useful as part of an annual screening programme to monitor underlying risk.

- There was general agreement that the rigour of the SASB standards helps convince investment teams it is worth integrating these ESG issues into their process.

Portfolio monitoring

In alignment with the PRI-ERM framework for ESG Monitoring and Reporting, SASB divided types of GP disclosure into two: core and additional disclosures.

- Core disclosures should include the ESG risk and opportunity profiles of the portfolio companies, as well as showing any changes to those profiles in response to emerging ESG issues. In addition, GPs should disclose how ESG factors are being managed by portfolio companies in the fund.

- Additional disclosures could demonstrate any additional value added by ESG management, such as positive impact to margins, brand and reputation, as well as growth in terms of new products and services.

And asked the questions:

- For LPs, what information is needed to monitor ESG within funds and across the portfolio?

- How can GPs ensure monitoring and reporting contribute to value protection and enhancement?

- How can we solve the divergence between portfolio-wide reporting on LP-identified factors and a bottom-up financially material approach to monitoring and reporting – without burdening portfolio companies?

- What happens when an LP wants reporting that is not necessarily financially material to a specific portfolio company?

- What is the cost for GPs to collect this data?

While the workshop participants said most LPs tend to be satisfied with materiality-based assessments, some LPs are prescriptive on KPIs.

- One LP said they found it useful to challenge themselves on what information they find really meaningful, in order to direct GPs on what reporting can be most useful.

- A secondary investor explained that, as they are “stepping into the shoes of another LP” with limited ability to influence, they have to view ESG from a risk perspective and focus on screening for risk. This screening has in the past led to divesting some interests from a portfolio on ESG grounds.

- One participant framed the reasoning for ESG monitoring as: are the outcomes reasonable and is there potential to achieve them? What is the underlying burden or cost to the portfolio companies to report against the outcomes? They advised that the investor has to “get comfortable” with the information that the GP is able to gather, as long as it is valuable enough to realise the planned-for outcomes.

- One GP said they found the incentives for reporting unclear unless factors are linked to financial levers and impact the bottom line, so it is helpful that SASB metrics are factors that can be linked to capex (amongst other factors influencing corporate financial performance).

- Collecting KPIs can be outsourced. One GP that does so said they found the service reasonably priced relative to the fund’s operating costs.

SASB and other reporting requirements

SASB closed the workshop by presenting on how their standards can support reporting against:

- Recommendations of the FSB Task Force on Climate-related Financial Disclosures (TCFD);

- Reductions of negative impacts according to the framework established by the Impact Management Project (IMP);

- Identification of which underlying targets to the UN Sustainable Development Goals (SDGs) can be linked to the financial and operating performance of companies – the SASB SDG Materiality Map is currently scheduled for release in Q4 2019;

- ESG Guidance for Disclosure for publicly listed companies – a consideration for IPO strategies; SASB is referenced in 45% of the 42 major stock exchanges that have established ESG Guidance for Disclosure.

The workshop was introduced by Natasha Buckley, Senior Manager – Private Equity at the PRI, and presented by Jeff Cohen – Institutional Product Strategist at SASB. Please contact Natasha Buckley [email protected] with queries regarding PRI frameworks and guidelines. Please contact [email protected] with any queries relating to the implementation of SASB standards.