Case study by LocalTapiola Asset Management Ltd

- Signatory type: Investment manager

- Region of operation: Finland

- Assets under management: US$12.2bn

Why a multi-period SAA approach outpaces a static strategy

Strategic asset allocation (SAA) is key for every long-term investor. It is the critical decision which will define whether an investor achieves her long-term investment goals or not. In comparison, tactical asset allocation and asset selection, while still important, explain less variation in long-term investment performance.

SAA is also a complex and investor-specific decision. An investor must consider the financial assets available, their expected returns and risks, as well as investor-specific preferences and circumstances, including investment horizons and regulation.

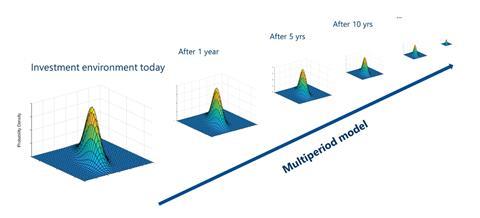

For a long-term investor, it is not enough to just consider expected returns and risk today, but also how they develop over time when the investment environment or investment opportunities change. Obviously, a longer investment horizon increases the likelihood that these changes will occur.

In addition to long-term investment goals, long-term investors also often need to consider period-by-period performance in their SAA. That is, even if only long-term performance ultimately matters, many investors, and their stakeholders, also still care about the short-term. That’s because of various reasons such as annual reporting, benchmarking and cash flow needs.

This combined with the fact that the investment environment is constantly changing implies that SAA decisions can best be tackled by dynamic multiperiod models rather than using a static one-period model.

A more realistic starting point for SAA is to consider long-term portfolio choice using intertemporal portfolio models. In these models, multi-period portfolio choice is solved under different conditions and preferences. It is often argued that multi-period models are too complex to be used in practice, a criticism that has been previously partly justified. However, academic research on multi-period portfolio choice as well as computing power and numerical methods has advanced to the point where approximations to multi-period solutions can be efficiently utilised.

Figure 1: strategic asset allocation and time-varying investment opportunities

Importantly, even if an investor eventually decides to use a single-period SAA model, they should still recognise the multi-period nature of their decision. That is, the investment environment will change during long investment horizons, and most often, the ones that matter most for performance are unexpected shock-type events that are difficult to forecast. Two recent examples of this are the US-China trade disputes and the Covid-19 pandemic, including the unprecedented actions of central banks to stabilise the financial markets and protect the economy.

To summarise, we should consider in our SAA that the investment environment changes over time and that for many long-term investors both short- and long-term investment goals matter.

How we developed a multi-period SAA model

Our aim is to help internal and external clients enhance their decision making on long-term portfolio choice and financial investment planning. Our SAA model’s theoretical background is anchored in academic work and built by keeping focus on investors’ practical needs and real-life requirements.

In the model, an investor-specific multi-period portfolio solution is obtained by assuming that the investment opportunities can change over time and that long-term investors, depending on their preferences and circumstances, may want to hedge their portfolios against these changes. The aim is that the expected performance of their portfolios will match their short- and long-term investment goals. In our case, changes in the investment environment relate to levels of economic growth and inflation as well as the level of market stress and interest rates.

Example: climate change and long-term scenarios

We have built a flexible model so that it can be extended and modified without changing it every time we want to analyse a new issue or phenomenon. Otherwise, we could end up in a situation where we have multiple SAA solutions that are not comparable with each other, or even with the standard model.

The model can be used to generate long-term macro simulations, which is a standard modelling exercise conducted for our clients. These simulations also allow us to, for instance, analyse how climate change may affect portfolio performance and asset allocation over time.

From a SAA point of view, climate change is an interesting issue to analyse as it affects the investment environment in the long-term but also takes place gradually from period-to-period in a non-linear fashion. That is, we have a multiperiod phenomenon which has an influence on investment opportunities over time. Financial markets will adapt to unexpected as well as expected changes as they happen or become known, but it is also likely that, sooner or later, there will be jump-type changes in the investment environment that are difficult to forecast. In both cases, relevant changes can happen, for instance, in regulation, taxation, policy, investors, technology or physical risks.

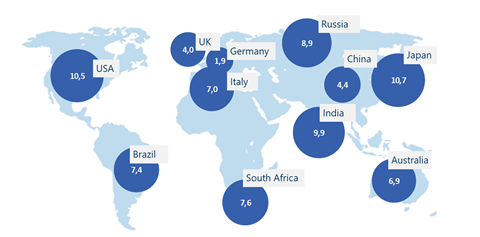

We concentrate on analysing how climate change may influence economic growth and, consequently, asset returns and risks. Climate change can affect the level of output or an economy’s ability to grow in the long-term. We do not model the economic effects of climate change by ourselves but use pre-existing (stochastic growth) models. We measure percent loss in GDP per capita over different time horizons caused by climate change under the Representative Concentration Pathways (RCP) scenarios of greenhouse gas concentrations, constructed by the Intergovernmental Panel on Climate Change (IPCC). Currently, we are using the RCP 2.6 and RCP 8.5 scenarios. Given the flexibility of our model, we could use alternative growth models or extend the analysis to include market stress by assuming different scenarios.

Figure 2: an example of estimated percent loss in GDP per capita by 2100 under RCP 8.5 scenario

Source: Kahn et al. (2019): Long-term macroeconomic effects of climate changes: a cross-country analysis: NBER Working Paper No. 26167.

In addition to quantitative simulations, we augment our results by qualitative analysis. This is important given the complexity of quantitative analysis and the high model dependency. To illustrate the latter, it is useful to consider how difficult it is to measure the economic costs of carbon emission. To do so you must obtain estimates of three distinct relationships. First, scientists must measure the relation between carbon dioxide emissions and concentrations in environment. Second, scientists must estimate the relation between carbon dioxide concentrations and temperature. Third, economists must estimate the effects of rising temperature on economic activity. What makes it even more difficult, is the reverse causality problem. That is, rising temperatures can affect economic activity, but also vice versa. This makes it important to use various competing models and qualitative analysis to assess the effects of climate change.

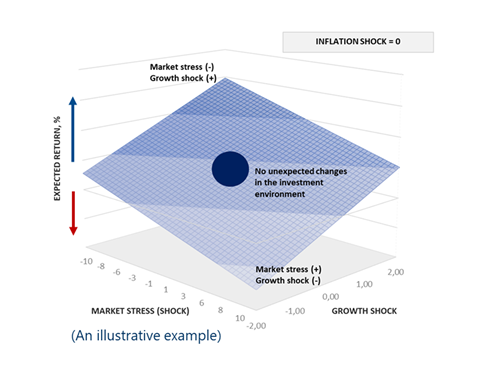

Figure 3: an example of SAA sensitivity to growth shocks and market stress

We have noticed that among our clients there is growing interest and need for this kind of analysis and our work is ongoing. The results will be considered in SAA between different asset classes and geographical regions. They should help us prepare for unexpected scenarios and strengthen our risk management. It is important to understand the limitations of ultra-long simulations based on various assumptions on the phenomenon that is very difficult to model. Nevertheless these simulations provide valuable information on how climate change may influence asset returns and risks over time and how SAA should take this into account under different investment horizons. Equally important is to estimate the magnitude of what might happen under different scenarios. This helps to understand how and how much climate may affect financial returns compared to other issues we are facing, such as demographic or globalisation changes. In the end, it is important to form an objective overall picture for SAA, not consider different phenomenon in isolation.