Executive summary

The appetite for ESG integration in private equity has grown strongly since the 2nd edition of this guide in 2011. Limited Partners (LPs) and General Partners (GPs) realise that responsible investment can contribute to both value creation and risk mitigation in this asset class. However, given the relationship between the LPs, GPs and portfolio companies, there are certain challenges to implementing responsible investment in private equity.

This guide is for any LP seeking to develop its own approach to responsible investment with respect to its private equity investment strategy, including (but not limited to): venture capital, growth capital, mid-market, buy-out, mezzanine, coinvestments, secondary investments, distressed and special situations and funds of funds. It may also provide assistance to investors in other private market strategies if they use a private equity-style closed-ended fund structure, such as infrastructure and real estate.

This guide is not intended as a checklist, nor does it advocate altering a GP’s management role and discretion over decision-making. Some aspects may seem aspirational for some private equity participants. It aims to present insights and provide actionable ideas into how responsible investment can be implemented by a broad range of LPs and GPs.

Why integrate ESG factors into private equity investments?

In private equity, responsible investment is the practice of incorporating environmental, social and governance (ESG) factors into investment decisions and active ownership during the due diligence process, the investment holding period and upon exit. This process can create value and act as an important risk mitigator. Due to the arms length nature of the LP relationship with the portfolio company and the illiquid nature of assets, it is key that the LP has assurance that the GP is identifying and managing future ESG risks and opportunities. A focus on processes and practices helps to deliver that assurance.

Misconceptions about responsible investment remain. There is no one right way to practice responsible investment and this guide presents various considerations and options for LPs that might be tailored to their own investment approaches, beliefs and strategies. For investors just embarking on this journey, there are a few things they can do to build capacity within their organisation, including learning from others and leveraging existing industry knowledge and experience.

The current ESG landscape in private equity

The evolution of responsible investment in private equity has been driven by developments including new regulatory and legal guidance and the rise of issues such as board diversity and climate change. The level of uptake of responsible investment throughout the investment sector means that this approach is now widely discussed and broadly accepted.

Despite these developments, there are challenges to this process including: misconceptions around fiduciary duties and responsible investment, establishing a clear mandate to provide guidance to investment teams, a wide dispersion of ESG knowledge within both LPs and intermediaries and establishing a common dialogue and taxonomy across the industry.

As well as highlighting some of the current regulatory and legal developments, such as the EU’s sustainable finance taxonomy to improve disclosure, the guide seeks to dispel some of the more common myths associated with LPs wishing to introduce a greater level of engagement with GPs on responsible investing.

For those embarking on this journey for the first time, the guide details five steps, and associated objectives to build capacity and to leverage existing knowledge and processes.

Tools and techniques for ESG integration in private equity

This guide covers the private equity investment process starting from the fundamental underpinnings of investment policies and beliefs, through to the exit phase. It draws on PRI guidance on diligence, fund terms and monitoring as well as industry best practices and existing collaborative frameworks to summarise recommendations at each stage of the investment process.

2018 private equity snapshot report

Section 1: Responsible investment and private equity

This section outlines the key drivers of ESG integration in private equity: value creation and risk mitigation and covers areas including:

- How different private equity ‘processes’ impact the integration

- Links to a discussion on fiduciary duty and ESG

- The PRI Principles in private equity

- A table of myths and facts about responsible investment

- Five capacity building actions for investors new to managing ESG

The PRI defines responsible investment as a strategy and practice to incorporate environmental, social and governance (ESG) factors in investment decisions and active ownership1. In the private equity market, Limited Partners (LPs) - who are stewards of capital - have a fiduciary duty to ensure that committed capital is managed appropriately and in line with their interests & policies. To that end, responsible investment is a systematic approach to evaluate and integrate material ESG risks, opportunities and issues into asset selection & ownership and portfolio construction.

For investors, including LPs and General Partnes (GPs), the focus is increasingly not “if” they should integrate ESG but “where, how, and is it feasible?” and key drivers include value creation and risk mitigation.

Value creation

The opportunity for private equity can be expressed as the difference between the cost of sound ESG management and its resulting impact on costs, profitability, revenue and the balance sheet. Measures might include EBITDA during the holding period, exit multiples and the ease of exit.

For example, steps to address ESG that can benefit the bottom line include:

- Improved ESG performance can create operating efficiencies that translate into cost savings and improved financial performance

- Energy efficiency or employee / workplace plans can have a positive financial impact, with a short payback period that can be measured from the financial accounts

- Development of new products and improved innovation

- Compliance with environmental / social law reduce possibility of fines and penalties.

Figure 1; Approaches to creating portfolio company value through responsible investment

Myths and facts about getting started with Responsible Investment in Private Equity

Myth #1: Responsible investing necessitates an exclusionary approach

Fact #1: There are many responsible investing methods and strategies available outside of exclusionary screens. Investors are encouraged to select approaches consistent with their investment strategies.

The practice of identifying and assessing material risks - ESG or other - in a potential investment may lead a GP not to pursue a specific target. The avoided investment is a result of a systematic consideration of risk and return – not a value-based screen.

Myth #2: We cannot do ESG because we invest in a sector that has negative ESG impacts

Fact #2: Encouraging better practices in high impact sectors can result in mitigating or avoiding material risks.

Myth #3: If I ask about a GP’s ESG practices and principles, top quartile GPs won’t want me as an LP

Fact #3: ESG is already on the radar of, if not actively considered by, a growing number of GPs. One private equity survey reports that 81% of respondents report on ESG efforts to their board at least annually. 2 In fact, GPs play an important part in awareness-raising for LP investment teams: when leading PE firms talk proactively about the value of their responsible investing approach, they help convince LPs that this is a standard part of excellence in private equity fund operations.

From a global perspective, participation in responsible investment has grown to the point where ESG questions are no longer unusual. For example, the TCFD 3 has support from 833 organisations, including LPs. PRI signatories now number over 2,800 including 500 asset owners.

Myth #4: Looking at ESG factors is not part of my fiduciary duty. My goal is to deliver a certain rate of return or pay pensions, not to deliver social change.

Fact #4: Various country specific opinions (eg. The Freshfields 2005 report, 2015 ERISA guidance from the U.S. Department of Labor) are summarised in PRI’s ‘Fiduciary Duty in the 21st Century’. These determine that integrating ESG considerations is “clearly permissible and arguably required”. 4 Read more here.

Myth #5: We are a small team and it takes a lot of resources to be a responsible investor.

Fact #5: There is no standard format to implement responsible investing and getting started can be as simple as collecting information and putting questions to GPs. Additionally, there are many action items that can be done with minimal resources that leverage processes, people and relationships already in place.

Eventually, it may be necessary to acquire more resources, but this should not be done until the responsible investing beliefs and goals are defined and well established.

Risk mitigation

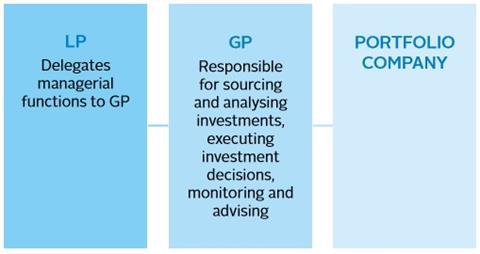

LPs generally remain at arm’s length from their private equity investments (See Figure 2). Often this means making a fund commitment decision largely based on the GP’s internal processes and systems. For LPs, it is therefore prudent to seek assurances that the GP will be able to manage future ESG risks within an investment or due diligence process.

Figure 2; LP, GP and portfolio company relationship model

There are also some considerations which are specific to private equity that will influence the introduction of ESG policies and processes by LPs and GPs.

Blind pool investing

Traditional fundraising in private equity requires LPs to make a blind pool commitment to a fund lifecycle of 7-10 years before the underlying assets are known. Private equity is a buy-to-sell model, not buy-to-own with the average holding period for a portfolio company is 3-7 years with all investments exited within the life of the fund. Therefore, LPs must undertake diligence of a GP’s responsible investment policies and procedures such as monitoring and reporting prior to fund commitments. If available, LPs may need to look to previous fund vintages for examples and engagement topics when doing their due diligence on the GP. If not, then there is a greater reliance on statements of intent and policies. See Section 3 module 3 for guidance.

Structure: Limited Partnerships

GPs have complete discretion over investment decisions and ownership activities for legal and practical reasons. However, a distinction can be made between influencing a decision and influencing a decision-making process. LPs should monitor and, where necessary, engage a GP about the policies, systems and resources used to identify, assess and make investment decisions with respect to ESG risk and opportunity. See Section 3 module 4 for guidance.

The role of intermediaries

When working with investment intermediaries—such as an Outsourced Chief Investment Officer firms (OCIOs), investment consultants or fiduciary managers - the onus remains on LPs to ensure the implementation of responsible investment strategies. Investment consultants play a key role in the formulation and review of investment goals, as well as the monitoring and oversight of investment managers. However, expertise and practice regarding ESG investing varies greatly even within a firm. LPs can address responsible investing during the selection process and in contracts.

Success with an OCIO can often be dependent on the Investment Committee’s commitment to prioritising responsible investing. For ESG integration across asset classes, investment Committees need to consistently and vocally express their interest. This may mean regularly asking about implications for long-term risks and highlighting areas of concern in order to encourage OCIOs to engage with managers. Increased monitoring by an OCIO can increase transparency provided by managers. LPs have found that this level of engagement prompts an OCIO to evolve their ESG approach.

Illiquid assets

Capital is usually deployed into a concentrated number of portfolio companies that are relatively illiquid versus other asset classes. Although the secondary market has matured significantly over the past ten years, an LP cannot easily sell its interests, and such sales often require permission from the GP. Any changes to the investment mandate may require negotiating with other fund investors. Actively reviewing a GP’s policies during the diligence phase can help to ensure ESG factors are incorporated into an investment process. LPs and GPs should also be prepared to change how ESG factors are managed, depending on prevailing market conditions and financial performance of portfolio companies when the capital is drawn down. See Section 3 module 4 for guidance.

Figure 3; A modern understanding of fiduciary duty

A modern understanding of fiduciary duty

As processes and approaches used to guide investment decisions5 have changed over time, so too has the notion of fiduciary duty.

Our report, Fiduciary Duty in the 21st Century: Final Report, puts forward a modern definition of fiduciary duty. This report describes how the integration of ESG issues into investment practices and decision-making is an increasingly standard part of the regulatory and legal requirements for institutional investors. Additionally, the report provides an overview of landmark studies on how ESG issues impact investment value. These studies can support LPs’ internal discussions on responsible investment.

Figure 4; Applying the PRI Principles to Private Equity

| PRI Principle | Actions for Limited Partners | Actions for General Partners |

|---|---|---|

| Principle 1: We will incorporate ESG issues into investment analysis and decision-making processes | Factor responsible investment considerations into fund selection, fund terms, and fund monitoring processes. | Identify material ESG factors in preinvestment processes that might affect returns. Ensure ESG is deeply rooted in investment approach by teams. |

| Principle 2: We will be active owners and incorporate ESG issues into our ownership policies and practices | Within limited liability status, set up parameters for how LPs might engage with portfolio company management. Also engage with the GP on ESG considerations in their corporate policies. Post-acquisition, LPs should remain engaged through appropriate monitoring and GP reporting. | Establish processes to understand and manage material ESG risks and opportunities in partnership with portfolio company management. |

| Principle 3: We will seek appropriate disclosure on ESG issues from the entities in which we invest | Request information from GPs about their responsible investment practices and the ESG characteristics of underlying fund investments. | Implement monitoring processes to assess portfolio companies’ management of ESG factors. |

| Principles 5: We will work together to enhance our effectiveness in implementing the Principles | Collaborate with peers and GPs to build consensus around responsible investment practices in private equity, leveraging PRI resources. | Collaborate with peers and LPs to build consensus around responsible investment practices in private equity, leveraging PRI resources. |

Capacity building for beginners

For an LP, we have identified five actions or first steps designed to leverage existing knowledge and processes.

1. Start a dialogue with your GPS

What this is:

To increase the organisation’s internal knowledge of the current ESG landscape and activities by investment partners, LPs have found it helpful to engage in dialogue with their GPs. GPs often have their own beliefs and goals with respect to responsible investing. These can span the range from merely addressing a specific issue within an existing fund vehicle, to creating individual segregated impact funds. The intent of this dialogue is to learn from the GP’s own responsible investing journey and become familiar with their existing responsible investing practices. For monitoring and assessing your GPs on responsible investing, please see Module 4: Monitoring & Reporting.

Objectives:

- Understand a GP’s approach to ESG issues

- Establish a baseline of understanding of current GP practices

- Build a long-term relationship with the GP on responsible investing

How to do this

Dependent on the strength & length of the relationship plus the GP’s resources, there are several ways to open a dialogue with your GP. Actions could include:

- Asking for the GP’s opinions on ESG standards, e.g., SASB guidance, or industry standards

- A review of any of the GP’s existing responsible investing-related documents or policies

- Raise questions at the Limited Partner Advisory Committee (LPAC)

Things to consider:

Dialogues with GPs can be an iterative process. An LP’s understanding of the GP’s responsible investment practices, as well as the LP’s own responsible investment beliefs and goals, will evolve over time. GPs responsive to LP requests may start to voluntarily include ESG material in their communications. The LP should be clear that they are not requesting changes to the GP’s investing or reporting practices, but are in the information gathering stage.

2. Leverage the work across an organisation

What this is:

There are transferrable principles and processes from other asset classes, investment processes and peers.

Objectives:

- Build information sharing networks between private equity teams and those of other asset classes

- Use insights from other asset classes to test ideas or as a basis for discussion with private equity GPs and other actors.

How to do this:

This is mainly an internal exercise for LPs who belong to larger investment organisations managing different asset classes. Knowledge sharing may either be informal (interaction between investment teams) or formal (official committees such as a responsible investing committee including all asset classes).

Things to consider:

Asset classes are traditionally siloed and have their own unique characteristics. Work is to identify and modify transferable lessons.

3. Engage with industry peers at other LPS

What this is:

According to recent reporting data, the number of LP PRI signatories exceeds 350, investing $1.1 trillion via externally managed private equity funds. This would indicate that LPs can gather and benefit from interaction with other LPs.

Objectives:

- Understand practices at other LPs and GPs

- Identify potential collaborations on responsible investing topics, such as GP engagement, reporting, documentation and due diligence approaches

How to do this:

Involvement in collaborative initiatives can afford the opportunity to network with peers and learn from their experiences. Another thing to keep in mind are other LPs on LPACs who have raised these issues in the past.

Things to consider:

Building a responsible investing relationship with fellow LPs may have the advantage of building stronger coalitions on LPACs. It may also afford you the advantage of knowing about emerging initiatives and the opportunity to take part.

4. Review resources and leverage existing tools

What this is:

Increased interest in responsible investing has also led to the development of several valuable public tools for different stages of the private equity investing process, from diligence to monitoring.

Objectives:

- Identify existing public tools and practices that can be adopted with internal resources

- Gather ideas for aspirational goals based on current market practices or internal processes

How to do this:

PRI and Institutional Limited Partners Association (‘ILPA’) are two main resources for RI in private equity. These complementary industry initiatives cover topics such as governance and provide tools and practices which might be tested with investment teams. Please see a list of resources in Appendix 2.

Things to consider:

While this approach is helpful for organisations with few internal resources, there will still need to be some internal work done to modify tools to suit the LP’s unique investment practices. While an organisation may not be prepared or want to use existing tools, they may provide ideas for future initiatives or new funds.

5. Identify and build current ESG processes

What this is:

Many investment practices that are not labelled “ESG” or “responsible investment” are still relevant as investment professionals realise that environmental and social issues are material or just good investment practice. In many cases, responsible investing practices have been spearheaded by individuals in companies who may be a sector expert or have a personal interest, but these practices have not been systematised across the organisation

Objectives:

- Engagement of internal personnel in the responsible investing discussion

- Demonstrate that ESG can be a good investing practice

- Explain terminology

How to do this:

A mapping out of company practices around typical ESG issues will often identify existing practices.

- Analyse existing practice among investment teams and committees

- Perform a gap analysis

Things to consider:

Investors may have preconceived ideas of responsible investing and may require effort to understand what practices fit into a responsible investing program.

Downloads

References

1 PRI (Jan 2020) What is responsible Investment?

2 PWC (2019) Private Equity Responsible Investment Survey

3 Taskforce on Climate Related Disclosures (June 2017)

4 Freshfields (2005), A legal Framework for the integration of ESG: UNEP FI (2015) Fiduciary Duty in the 21st Century: The Kay report (September 2011): CCLI (April 2018) Canadian fiduciary duties and disclosure obligations in the climate change contex

5 Uniform Prudent Investor Act (1994), 7B U.L.A. 16 (Supp. 1995)