By Matthew Orsagh (@MattOrsagh), Director, Capital Markets, CFA Institute

- Many people perceive that environmental, social, and governance (ESG) integration means sacrificing performance because they believe that ESG integration is the same as screening out companies and sectors from their investment universe.

- Understanding is low regarding the different ESG issues, the ESG criteria used to assess issuers, and what is considered to be good versus bad ESG performance.

- Knowledge sharing, training, case studies, and investment practice guidance not only improves awareness and understanding but also improves the culture. Generally, once portfolio managers learn about ESG integration, associated issues, and opportunities rather than just risk, portfolio managers buy in more fully to ESG.

CFA institute and the PRI released their fourth and final report on the state of ESG integration around the world with the publication of ESG integration in Asia Pacific: markets, practices and data. After holding 23 workshops in 17 markets over the past two years, a key takeaway on the state of ESG integration is that we are far from agreement on the definition of ESG itself and, by extension, ESG integration.

No matter where we went, nearly a quarter to one-third of those in the room equated ESG integration to simple negative screening—that is, screening out undesirable securities from an investment universe. ESG integration has grown a great deal from decades ago when negative screening was the predominant method of ESG screening. In fact, ESG integration is the most popular ESG incorporation approach—performed solely or in combination with screening—and is what CFA Institute teaches in its curriculum to the more than 200,000 people who sit for the CFA® exam each year, which includes ESG topics.

For those at the forefront of ESG integration, it can mean including material ESG factors into the investment process. That approach has a lot of wiggle room, as investors don’t always agree on what is “material.” In the CFA Institute and PRI report, Guidance and case studies for ESG integration: equities and fixed income, we defined ESG integration as “the explicit and systematic inclusion of ESG factors in investment analysis and investment decisions.” Again, this definition is subject to different interpretation.

The confusion around a shared understanding of ESG integration generally focuses on four areas (see the table below):

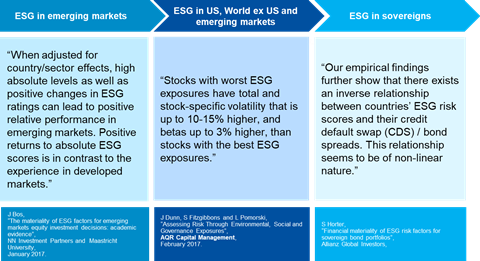

- Evidence of investment benefits. Despite the huge library of academic research and practitioners’ research proving otherwise (see figure 1, which refers to recent research by three practitioners), many people still perceive that ESG integration means sacrificing performance because they believe that ESG integration is the same as screening out companies and sectors from their investment universe. An understanding that ESG integration is complementary and additive to fundamental analysis will debunk this myth, but that will take time. Jacob Messina, CFA, head of SI Research at RobecoSAM, argued that “for a long time, people were concerned that sustainable funds would underperform, but the industry has proven its ability to generate returns in line with mainstream peers. However, simply integrating ESG information is not a panacea for creating alpha. You have to be a diligent investor with great people, processes, and philosophy around valuation to remain competitive. If you do that in sustainable investing, then you can compete with mainstream funds with the same attributes.”

- ESG issues. Understanding is also low regarding the different ESG issues, the ESG criteria used to assess issuers, and what is considered to be good versus bad ESG performance. For example, one investor may think auto electrification is a plus; another investor may think that it requires more platinum, which means more mining and high ESG risk. Where should we draw the line?

- Materiality. Portfolio managers, ESG professionals, companies, and other stakeholders can have different definitions of materiality, as highlighted by Sebastien Thevoux-Chabuel, portfolio manager at Comgest, who notes “the issue with materiality is most of the time people do not ask, ‘which ESG issues are material and to whom?’ This is because materiality can differ a lot depending on the perspective; it is really in the eyes of the beholders. So what could be material for the employees, could be quite immaterial for clients; what is truly material for the shareholders can be totally immaterial for NGOs.” This is fine, as is the case that not all managers or analysts apply the exact same weighting of current metrics in their fundamental analysis. This learning curve on materiality needs to tackled, however, and it can be with proper training and resources.

- ESG integration practices. Integration speaks to the crux of the issue. Wherever we traveled, much of our audience just wanted us to tell them “how” to best integrate ESG data in the investment practice. As noted, unfortunately, no one ESG integration method or ESG data point can work for everyone in every case. ESG integration is a mixture of art and science. Investors need to decide for themselves what is material, what ESG resources they have at their disposal, and how best to integrate ESG data in the investment process.

Four main areas of misunderstanding surrounding ESG integration

| Barriers | Concerns Raised at the Workshops | Solutions |

|---|---|---|

|

Evidence of investment benefits |

• Both investors and clients need to be educated about the return and risk benefits of ESG integration. |

• Knowledge sharing • Training |

|

ESG issues |

• Definitional issues hinder investors and companies from discussing ESG issues. |

• Knowledge sharing • Training • Materiality frameworks |

|

Materiality |

• What is the threshold for calling it material? • Is it a price change of 1%, 2%, or more? • Or is it a percentage difference between the intrinsic value and the market value? |

• Kn owledge sharing • Training • Case studies |

|

ESG integration practices |

• Difficult to understand what practitioners are actually doing to integrate ESG analysis. |

• Training • Case studies • Investment practice guidance |

Ultimately, the solutions to these problems include the following:

- Knowledge sharing and training for all staff:

- Knowledge sharing not only improves awareness and understanding but also improves the culture. Generally, once portfolio managers learn about ESG integration, associated issues, and opportunities rather than just risk, portfolio managers buy in more fully to ESG. A recommendation shared by Sudip Hazra, head of Sustainability Research at Kepler Cheuvreux, was to be flexible on labeling the issues as ESG issues: “The biggest area of traction that we have had with mainstream investors has been to focus on ESG as risks and opportunities in specific timeframes. When we present research with ESG themes as a risk- and opportunity-focused thematic report, we find it much easier to get access to portfolio managers who already are looking at an ESG issue/theme but don’t necessarily think in ESG terms. Though there is a definite increase in interest occasionally, the term ‘ESG’ still needs explaining.”

- There is a talent gap. ESG teams often lack professionals with investment experience and application, and investment desks largely consist of professionals with limited ESG knowledge and research skills (for more insights, read this blog). To raise the ESG knowledge on the investment desks, Masja Zandbergen-Albers, head of ESG integration, illustrates that at Robeco, “there is a champion within every investment team who is responsible for making sure that we integrate sustainability, that we innovate, and that we think of new products. These champions lead bi-monthly meetings, where they share best practices and discuss implementation issues and new things that we have developed.”

- Materiality frameworks for ESG issues:

- Investors are creating their own materiality frameworks. Emily Chew, global head of ESG at Manulife Investment Management, says, “Frameworks are really critical for trying to get your arms around a fairly expansive and potentially vague space. They need to be reviewed and updated over time. Ideally they need to be sufficiently flexible that as social norms evolve, as environmental issues emerge, as corporate governance norms evolve as well, the frameworks can incorporate those new issues.”

- If you want to develop your own, some investors use the SASB (Sustainability Accounting Standards Board) materiality map as a starting point to develop an internal, proprietary materiality framework.

- Case studies for materiality and practices:

- Case studies are needed for every sector, issue, and market.

- In the CFA Institute and PRI Guidance and case studies for ESG integration: equities and fixed income report, we provided 33 case studies across many markets and sectors that share ideas about how investors integrate ESG issues into equity and fixed-income investments.

- Investment practice guidance:

- Hopefully, the ESG integration framework developed by PRI and CFA Institute will provide this guidance.

More thorough consideration of ESG factors by financial professionals can improve the fundamental analysis they undertake and ultimately the investment choices they make. We are in the early days of ESG integration, however, and are just at the beginning of the ESG integration learning curve for most practitioners. The good thing is that practitioners do not need to worry about which ESG integration process works best for everyone, but rather they should focus on what works best for them and their clients.

This blog is written by PRI staff members and guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase some of our research and other work that we undertake in support of our signatories.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected].