By Christopher Bruno and Witold Henisz, the Wharton School of the University of Pennsylvania

Local governments differ in the environmental, social, and governance (ESG) outcomes they provide their residents, such as rates and distribution of toxic emissions, incarceration, and health outcomes. These outcomes are related to the quality of life of residents within a specific geographic area and extend beyond standard fiscal health measures. The policy, expenditure, and revenue generating practices of local governments vary in the prioritization of these ESG outcomes.

Our research, developed in partnership with the Calvert Institute and Activest, highlights that worse aggregate ESG outcomes are associated with increased credit risk for investors in municipal securities, even when controlling for a variety of economic, fiscal, and bond risk indicators.

While investments in municipal entities that fund healthcare, education, safety, and public services may seem to have stronger links to ESG considerations than investments in for-profit firms, municipalities, just as their private and sovereign counterparts, vary in such outcomes. This variation exists in the levels and the distribution of outcomes across different groups.

Research on locational amenities predicts that people will migrate to regions with less pollution, stronger schools, better health outcomes, and greater safety over time. This spurs changes in tax revenues, and local governments that improve their citizens’ quality of life are rewarded with increasing income that can then be used to facilitate continued investment in public services.

Inequality in these outcomes can be a source of conflict and unrest within communities, which can also affect a region’s attractiveness to residents. It is therefore important to incorporate differences in the levels of ESG outcomes (and inequalities in their distribution) in the analysis of municipal credit risk, as these are material for investors.

How differences in ESG outcomes are correlated with municipal credit risk

We demonstrate that differences in ESG outcomes are correlated with municipal credit risk using a novel database collected from the following sources:

- US Center for Disease Control

- US Environmental Protection Agency

- US Department of Agriculture – Food and Nutrition Service

- US Census Bureau American Community and Decennial Census Surveys

- US Energy Information Administration

- US Bureau of Labor Statistics

- The Government Finance Database

- Vera’s Incarceration Trends (sourced from US Department of Justice Bureau of Justice Statistics)

- The Intercontinental Exchange Data Services

- SDC Platinum

- Moody’s

- S&P

We explore the association between variables from these sources (from 2001 to 2018) and credit risk (from 2001 to 2020) contemporaneously and over the ensuing five years.

We specifically examine the county or county-equivalent population rates near a toxic emissions facility, renewable energy mix, drug-induced mortality, all-cause mortality, incarceration, poverty, supplemental nutrition assistance program participation relative to poverty, fines and forfeits revenue, and public safety expenditures, as well as inequality between Black and White residents in housing values, population near toxic facilities, mortality, incarceration, and poverty.

Our analysis suggests that better ESG outcomes are negatively associated with credit risk even when controlling for economic performance and other varying factors, such as:

- median household income

- unemployment rate

- fiscal health (e.g., revenue from own sources and debt per capita as well as state aid)

Our analysis also controls for issuer- and county-level factors that do not vary across time, state- and coupon-level shocks over time and shifts across time in the attractiveness of bonds with a given time to maturity and credit rating.

Specifically, we found that, holding all of these factors constant, a one-standard-deviation decline in ESG outcomes across the 14 variables we tested, in aggregate, was associated with an approximately 5 bps higher municipal bond yield over five years.

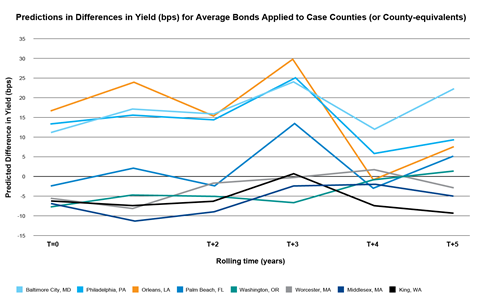

When we examined specific counties on the 14 variables holistically, we found that average predicted yield could vary between approximately 5 and 30 bps between a bond from a county with relatively high ESG outcomes (e.g., King County, Washington) to one with relatively low outcomes (e.g., Orleans County, Louisiana) – see Figure 1.

Potential implications

Our research suggests that ESG outcomes, and distribution therein, should be considered in the due diligence process of municipal securities. Municipalities have a direct connection to ESG outcomes, such as environmental remediation, health, welfare, education, and security.

A long-term focus on the benefits of investments in ESG issues for current and potential residents should be rewarded by investors concerned about a municipality’s fiscal health and strength.

The theory, main results, and supplementary analyses suggest that investments in affordable housing for disadvantaged groups, the clean-up of toxic waste that disproportionately affects such groups, reduced reliance on revenue sources that penalise them and on expenditure sources that treat social tensions primarily as a safety issue for the advantaged instead of addressing root causes of tension are not only philanthropic or ideological. They offer good economic investments.

Issuers that deliver on their ESG-related use of proceeds could be recognised for this in future transactions, not just via the issuance of more affordable green bonds, but also in the pricing and performance of every municipal bond.

For more information on ESG integration in sub-sovereign debt, please refer to PRI’s resources here.

About this paper

Our working paper builds on developing research on societal factors that impact municipal credit risk, such as the opioid crisis and climate risk, as well as work connecting ESG factors to the risk of sovereign and corporate debt. It was further motivated by recent research on investor biases with respect to race. For example, Dougal et al. (2019) found evidence that historically black colleges and universities pay a credit premium unrelated to their underlying credit quality, that is further exacerbated in the Deep South.

An earlier version was presented at the peer-reviewed UNPRI Academic Week Conference in September 2021 and is available on the PRI’s BrightTalk channel.

This blog is written by academic guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase research in support of our signatories and the wider community.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected]

References

1. Cornaggia, K. R., Hund, J., Nguyen, G., & Ye, Z. (2020). Opioid Crisis Effects On Municipal Finance. Working Paper, SSRN [SSRN Scholarly Paper]. https://doi.org/10.2139/ssrn.3448082

2. Crifo, P., Diaye, M.-A., & Oueghlissi, R. (2017). The effect of countries’ ESG ratings on their sovereign borrowing costs. The Quarterly Review of Economics and Finance, 66, 13–20.

3. Dougal, C., Gao, P., Mayew, W. J., & Parsons, C. A. (2019). What’s in a (school) name? Racial discrimination in higher education bond markets. Journal of Financial Economics, 134(3), 570–590. https://doi.org/10.1016/j.jfineco.2019.05.010

4. El Ghoul, S., Guedhami, O., Kwok, C. C., & Mishra, D. R. (2011). Does corporate social responsibility affect the cost of capital? Journal of Banking & Finance, 35(9), 2388–2406.

5. Goldsmith-Pinkham, P. S., Gustafson, M., Lewis, R., & Schwert, M. (2019). Sea Level Rise and Municipal Bond Yields. Working Paper, SSRN. https://www.ssrn.com/abstract=3478364

6. Gottlieb, P. D. (1995). Residential amenities, firm location and economic development. Urban Studies, 32(9), 1413–1436.

7. Li, W., Zhu, Q. (2019). The Opioid Epidemic and Local Public Financing: Evidence from Municipal Bonds. Working Paper, SSRN. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3454026

8. Massey, D. S., & Denton, N. A. (1985). Spatial assimilation as a socioeconomic outcome. American Sociological Review, 94–106.

9. Massey, D. S., & Mullan, B. P. (1984). Processes of Hispanic and black spatial assimilation. American Journal of Sociology, 89(4), 836–873.

10. Massey, D. S., Condran, G. A., & Denton, N. A. (1987). The effect of residential segregation on black social and economic well-being. Social Forces, 66(1), 29–56.

11. Painter, M. (2020). An inconvenient cost: The effects of climate change on municipal bonds. Journal of Financial Economics, 135(2), 468–482. https://doi.org/10.1016/j.jfineco.2019.06.006

12. Stewart, F. (2008). Horizontal inequalities and conflict: An introduction and some hypotheses. In Horizontal Inequalities and Conflict (pp. 3–24). Springer.