By Amir Amel-Zadeh, Saïd Business School, University of Oxford; Rik Lustermans, Erasmus School of Economics, Erasmus University and ABN AMRO Bank; Mary Pieterse-Bloem, Erasmus School of Economics and Erasmus Research Institute of Management, Erasmus University, and ABN AMRO Bank

Do wealthy retail investors care about sustainability? According to our paper, they do. We find that European private wealth investors invest significantly more in assets with high sustainability ratings than low sustainability ratings. Moreover, we show that they react to changes in sustainability ratings by rebalancing their portfolios towards higher-rated assets.

Unknown sustainability preferences

Over the past decade, there has been a rapid rise in sustainable investment funds that screen companies based on environmental, social and governance metrics and an increasing number of institutional investors that have signed up to the Principles of Responsible Investments, pledging to consider sustainability information in all their investment decisions.

Growing academic evidence on institutional investors’ attitudes towards sustainability also suggests that professional asset managers increasingly prefer more sustainable firms, increasingly engage with portfolio companies on sustainability issues, and consider sustainability information, particularly related to climate change, important to their investments.

Surprisingly, little is known about retail investors’ preferences and asset allocation decisions with respect to the environmental and social impact of their portfolio assets. In our paper, we examine the sustainability preferences of wealthy private investors and the effect of sustainability ratings on their asset allocation decisions. We study wealthy investors as they have a disproportionately larger impact on asset demand and returns than the average household.

What does the data tell us?

To study the investment choices of wealthy households, we obtained access to a proprietary dataset of European private wealth investors’ investment holdings at ABN AMRO private bank – the third largest private bank in Europe, with more than 100,000 clients and almost €200 billion in assets under management. The data consists of monthly individual asset-level investment holdings from March 2016 to October 2019, grouped by investor type (i.e. whether they have access to an advisor at the bank or use the bank only for execution purposes) and country of residence (the Netherlands, Germany, Belgium and France).

We take advantage of three unique features of the data. We can distinguish between individuals who receive investment advice – and with that regular information about the sustainability ratings of their investment portfolio – and investors who use the bank solely for trade execution purposes.

We further observe that the bank’s sustainability reporting of investors’ portfolios varies between countries. While investors in the Netherlands and Belgium receive frequent updates of their investment assets’ sustainability ratings with their portfolio reports, sustainability reporting to investors in Germany is less frequent, and no sustainability ratings are included in investor reports in France.

The bank also changed the sustainability ratings provider during the time period we assess, which results in an increase in the number of client assets for which sustainability ratings are reported. As this increase in prominence of sustainability ratings for some assets is unrelated to their fundamentals or underlying sustainability characteristics, it allows us to measure investors’ response to the ratings themselves and to assess whether retail investment allocations change after the ratings become available.

Significant investment flows

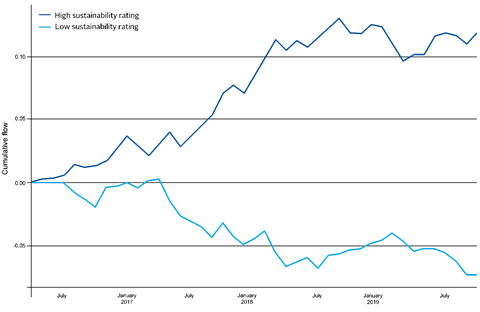

Our main results are illustrated in the figure below, which shows cumulative investment flows in our sample to assets with the highest and lowest sustainability ratings.

Over the course of our sample period, retail investors allocated more money to assets with a high sustainability rating and less money to assets with a low sustainability rating, compared to assets with a moderate sustainability rating.

The difference is economically significant, at 10% of the average monthly investment flow. In absolute terms, we document about €58 million per month in incremental investment into assets with high sustainability ratings, compared to those with low sustainability ratings.

Over our entire sample period, this results in about €2.5 billion being incrementally allocated to assets with high sustainability ratings by the retail investors at this bank. We further find this difference in flows to be larger for equities than for bonds and to predominantly stem from allocation decisions of investors that receive advice – those who more readily receive salient information about the sustainability ratings of their assets.

Figure 1. Cumulative investment flows by sustainability rating

To more confidently establish a causal link between sustainability ratings and retail investors’ investment allocations, we use the change in ratings provider as an experiment in which the visibility of the sustainability ratings for the underlying assets in investors’ portfolios increased for reasons unrelated to the assets themselves. We find significantly higher investment flows into assets with a high sustainability rating after this increase compared to those with a low sustainability rating.

Specifically, assets with a high sustainability rating enjoy almost double the monthly investment flows of those with a low sustainability rating. Economically, the average effect of the increase in prominence of the sustainability ratings is a roughly €800 million difference in investment flows between high and low-rated assets over the subsequent ten months.

Demand for higher-rated assets

We further investigate whether investors consider changes in the sustainability ratings of their portfolio assets. We examine whether investors reduce their exposure to assets that experience a ratings downgrade and increase their exposure to assets that are upgraded. We find that investors that receive more salient sustainability information (i.e. the advisory client group) react more strongly to these changes, by rebalancing their portfolios towards higher rated assets.

Our results suggest that sustainability ratings upgrades elicit significantly positive investment flows particularly by advisory clients and specifically by investors in countries that receive regular reporting of the ratings. That is, the sensitivity of investment flows to positive ratings changes is larger in countries, in which sustainability ratings are more visible to investors.

Overall, our study provides systematic evidence that private wealth investors consider sustainability information in their investment decisions and make economically meaningful allocations towards assets with higher sustainability ratings.

It has two broader implications. Our findings show that when given more visible information about the sustainability characteristics of their investments, retail investors take those characteristics into account in their asset allocations. This has implications for policy that intends to redirect investments into more sustainable assets.

Our results also point to the influence sustainability ratings have on investment flows. It is therefore important for investors to understand what these ratings measure and how nuances of environmental, social and governance issues are summarised into one ratings number.

The paper is available here.

This blog is written by academic guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase research in support of our signatories and the wider community.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected].