About the report

This report summarises the outcomes of the PRI collaborative engagement on corporate tax transparency, which ran from 2017 to 2019. The engagement sought to: create awareness within companies of investor concerns around aggressive corporate tax practices and expectations of responsible tax practice; improve company disclosures across tax policy, governance and financial reporting; and identify best practice. This document aims to support investors who want to take up this issue as an engagement priority. Specifically, the report:

- Evaluates the progress of target multinational companies in the healthcare and information technology sectors in the context of objectives of this initiative;

- Includes a summary of the engagement takeaways; and

- Sets out recommendations for investors on corporate tax responsibility going forward.

Introduction

Corporate taxation that is effective and fit for purpose can drive sustainable development, mitigate rising inequality and support inclusive growth and prosperity. In addition to financing much-needed public services, it can enable governments to fund social and environment programmes to address some of the pressing global challenges we face today. To meet these objectives, however, the global tax system must evolve and adapt, and businesses must embrace corporate tax responsibility.

In recent years, multinational companies have come under increasing scrutiny for their pursuit of tax avoidance, including through profit shifting, where they funnel profits to jurisdictions that charge lower tax rates instead of paying taxes where their earnings are generated. These tax practices can reduce tax revenues and cost governments globally between US$100bn and US$600bn annually.

Tax avoidance also presents governance, reputational and earnings risks for companies. Although companies may argue that such practices drive profits, this position is less defensible when tax practices are subject to scrutiny by tax authorities and consequently result in unexpected reputational damage, litigation costs and penalties. An overemphasis on minimising tax may also encourage poor decision-making by company boards. Furthermore, corporate tax avoidance results in social and macro-economic distortions in the market by affecting competition and reducing capital available for socioeconomic development, particularly in emerging countries. IMF researchers estimate the impact of tax avoidance on developing countries to be around US$213bn a year.

While global efforts led by the OECD are focused on curtailing tax avoidance, existing tax loopholes and outdated tax legislation have proved to be impediments. For instance, the slow phase out of preferential tax arrangements for large businesses and the ubiquitous corporate use of tax havens to minimise tax liabilities have undermined the integrity of our tax systems. Additional tax challenges are presented by digitalisation – for example, while some corporate business models are no longer dependent on brick and mortar operations, taxation continues to be based on physical presence.

In this context, there is an imperative for long-term institutional investors to understand aggressive tax practices within their investments, support a shift away from tax practices that are short-term and unsustainable, advocate the creation of a level playing field in tax policy matters and communicate expectations to companies in order to drive broader societal and economic objectives

Tax avoidance undermines long-termism by limiting government spending on critical services such as infrastructure and on addressing externalities like climate change. These macro-economic impacts make corporate tax responsibility an important systemic issue for universal owners, even if some parts of their portfolio may perform better in the short term due to tax avoidance.

Institutional investors have the means to steer companies to focus on genuine economic activity as opposed to tax behaviour that can negatively impact their profitability and sustainability and reduce wider portfolio returns.

Tax is a material issue for investors, given underlying investment risks and risks to wider portfolio returns. Through strong and deliberate action, they can respond to concerns about tax fairness and inequality from endbeneficiaries and deter companies from avoiding taxes, even when these practices may be perceived to be within the law.

Spotlight on corporate tax transparency

Given the compelling case for investor action, the PRI has worked with signatories since 2015 to provide guidance and support investors in achieving greater corporate tax responsibility. It has been evident in this work that the lack of corporate transparency on tax issues has impaired investment analysis and understanding of how companies are positioned on tax issues. The opacity around tax structures that companies tend to employ has added another layer of complexity to this technically challenging topic. Investors are therefore demanding more accurate, timely and meaningful corporate reporting to enable better assessment of tax risks and opportunities and to identify leading practices in their portfolio. At the very minimum, investors expect more public disclosure to shed light on companies’ stance on tax across all markets. They expect companies to employ governance mechanisms that enable implementation and appropriate oversight of a company’s tax strategy. And they expect disclosure of underlying economic and financial data that support any wider assertions made by companies concerning those practices.

With that said, enhanced tax transparency is a means to an end and does not in itself guarantee responsible tax practice. However, in the absence of standardised reporting, robust disclosure will help investors gauge companies’ positions on tax and facilitate assessment of their exposure to tax risks. For instance, meaningful disclosure could bring to light boardroom priorities and decision making around high-risk transactions. It could also help identify inconsistencies between companies’ public positions and actions, providing a valuable backdrop for discussions with companies on the development of responsible corporate tax strategies and relevant implementation practices.

Engagement agenda

Given the importance of tax transparency as outlined above, the PRI coordinated a collaborative investor engagement on the theme over 2017-19. The engagement built upon the work done by the PRI and a group of global investors in producing the Engagement Guidance on Corporate Tax Responsibility and the Investors’ Recommendations on Corporate Income Tax Disclosure to facilitate investorcompany dialogue on responsible tax and clarify investors’ expectations.

Through this engagement, 36 institutional investors (representing approximately US$2.9trn in assets under management) asked for improved disclosure from 41 portfolio companies with the aim of clarifying investors’ expectations of corporate behaviour and identifying leading practices in the following areas:

- Publication of a global tax policy that outlines the company’s approach to responsible tax;

- Reporting on tax governance and risk management processes; and

- Country-by-country reporting (CBCR).

The engagement specifically focused on multinational companies in the healthcare and technology sectors due to those sectors’ poor tax disclosures, despite the heightened risks they face, particularly relating to:

- Alleged use of tax avoidance strategies reported in the media, for example in relation to the transfer of intellectual property (IP) rights across jurisdictions to reduce tax burdens;

- Regulatory fines and new regulations targeted to address tax avoidance and close tax loopholes (e.g. for the digital economy); and

- Their high tax gap – that is, the difference between statutory tax rates and what is actually paid – relative to other sectors.

The engagement was informed by PRI-commissioned benchmark research which provided a view on the state of disclosure and identified gaps in the healthcare and technology sectors. The research findings from the assessment of 50 companies are discussed in detail in the PRI report.

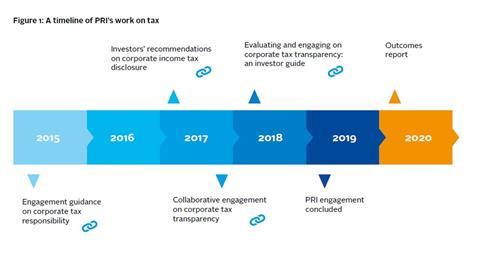

A final evaluation was also undertaken at the end of the engagement to determine how companies have progressed. This outcomes report summarises the key findings of this research and highlights relevant engagement insights in the context of these trends (see Figure 1 below for a brief timeline of the PRI’s tax publications).

In summary, the research found that:

- Companies most commonly report tax data that are required by regulations and accounting standards

- There are discrepancies between corporate disclosure and investors expectations. For instance, there is:

- A lack of evidence from companies of how their publicly disclosed tax policies are consistent with the overall strategic objectives of the organisation, and their broader sustainability commitments;

- Few concrete examples of how companies determine if tax transactions are in line with their risk appetite; and

- Insufficient explanation and granular data to validate corporate commitments to avoid aggressive tax planning.