The PRI has compiled a list of more detailed emerging solutions that have been discussed during the investor-CRA roundtables, aimed at improving the transparent and systematic consideration of ESG factors in credit risk analysis.

Some recommendations target both CRAs and investors, others are tailored to each stakeholder, and some apply to both. Some recommendations can be implemented quicker than others, which have a longer-term focus.

The list is not prescriptive and does not imply that ESG factors are more important than others from a credit risk perspective. As the PRI recognises that organisations are at different stages of ESG consideration and vary in size and available resources, it does not advocate a one-size-fits-all approach. The implications of ESG factors (current or potential) on issuer creditworthiness depend on the specific characteristics of each entity. Among institutional investors, credit-relevant time horizons may differ between AOs and AMs. Furthermore, some market players – notably the large, global CRAs, specialised players as well as advanced investors – have already made visible progress on many aspects of the recommendations, as documented in this report and its previous iterations. In this case, the list should be adopted as a guideline to continue or enhance current practices – but this does mean there is room for complacency.

Joint investor-CRA recommendations

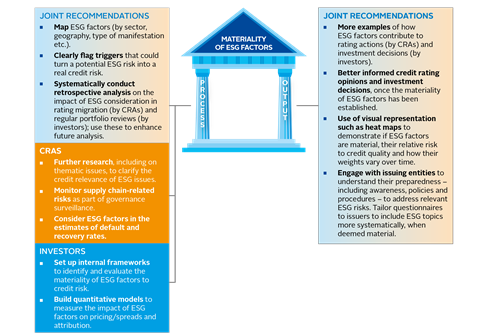

Categorise ESG factors

CRAs and investors should continue to work on clarifying how ESG factors are material to credit risk by type (event, trend or policy-driven) or by ranking them according to their relevance and urgency. Analytical tools that use colour coding, such as heat maps, can facilitate the ranking of the relevant ESG factors from a credit risk perspective, and their evolution.

Retrospective analysis

As more data become available, more sophisticated backtesting on the impact of ESG factors on credit risk, default and recovery analysis, and related changes over time, should be carried out. It is not always possible to identify historical trends to inform the analysis, and backtesting cannot capture emerging issues which need monitoring. Nevertheless, while the past is not always indicative of future trends, this exercise may help to improve forward-looking analysis, which remains a mix of quantitative and qualitative assessments. In the case of event-driven risks, assessing the entity’s resilience post-event (i.e. how it reacted and invested in better prevention and mitigation) may also be useful – a practice already adopted by some CRAs.

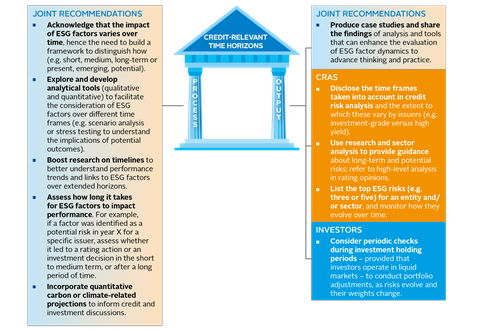

Recognise credit-relevant time horizons

Time horizons vary and depend on factors including investment objectives and the type of rated entities or instruments. While analysis must be based on the foreseeable future, a key question when assessing ESG factors – which are often linked to secular trends – is how to treat those that could have a material impact on long-term creditworthiness (such as physical climate risk).

To reconcile these temporal dimensions, “what if” analysis – through stress testing, and sensitivity and scenario analysis – can signal long-term risks, incorporate uncertainty and focus on drivers of potential outcomes, as well as help to understand an issuing entity’s level of risk awareness. This is the point at which an ESG factor turns into a credit risk factor can be demonstrated: if an ESG factor is not deemed credit-relevant at that time, the circumstances under which it could become relevant can be stated. European regulation already requires CRAs to give appropriate risk warning, including sensitivity analysis of relevant rating assumptions. Making ESG a bigger component of the sensitivity analysis that they already conduct would therefore also enhance transparency.

Engage with issuers and other key stakeholders

CRAs and investors should have regular conversations with issuers on ESG topics. While (in theory) both conversations could start with similar questions, it is important to note that CRAs and investors engage with issuers for different purposes. Investors may engage, individually or collaboratively, for fact-finding (insight) to make more informed investment decisions or with a specific objective (influence), such as through the investor initiative Climate Action 100+. CRAs, by contrast, cannot influence a rated entity’s policies or structure, and cannot provide professional or legal advice, but they should engage on ESG topics, when relevant, to assess how a rated entity’s management and governance could impact its creditworthiness.

Either way, having these conversations more frequently will help issuers to recognise that disregarding material ESG risks can result in suboptimal investments and ratings that could affect their cost of capital. Improved transparency with issuers around what investors and CRAs believe are the most material ESG factors to credit risk could also prompt indirect market benefits in terms of improved issuer disclosure and reporting, as well as fostering a market standard of comparable, meaningful metrics that facilitates relative analysis.

Beyond issuers, investors and CRAs should engage constructively and responsibly with other stakeholders such as policy makers, providers of ESG intelligence – e.g. international organisations such as the International Monetary Fund (IMF), and, for investors, with ESG research providers – and regulators. With ESG consideration under intensifying regulatory scrutiny, this type of engagement can support the effective integration of ESG factors, where appropriate. Engaging with independent ESG data providers to produce quality, objective research will be equally important in driving quality ESG integration.

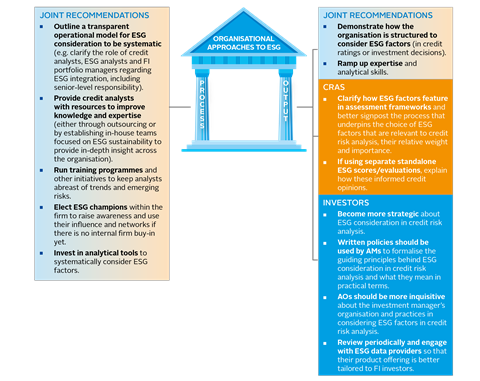

Continuously train credit analysts

Credit analysts must be equipped with the knowledge and resources required to conduct ESG analysis. Indeed, training by some CRAs has already started. This does not mean that credit analysts should replace ESG analysts. Rather, analysts should be trained on identifying links between ESG factors and cash flow generation, as well as signals that may alter credit risk and threaten the sustainability of business operations.

CRAS

Improve ESG factor signposting

CRAs need to continue proving that their methodology takes into account ESG factors in credit risk analysis. They need to be explicit in the press releases and commentaries that accompany changes in rating opinions or outlooks about how the materiality, likelihood and timeliness of ESG factors, when relevant, contribute to rating actions. While evidence of this is growing (see CRA examples), there is still room for improvement in providing clarity and guidance. For example, where material, CRAs could list the top ESG factors that have contributed to a rating decision or have a separate paragraph discussing them. They could also do the same for sector or industry analysis.

Clarify the credit-relevance of ESG factors

CRAs should continue to publish thematic, regional and sector research that explains how ESG factors affect credit risk. They should use these findings as an aside to the rationale behind whether and how ESG factors may contribute to credit rating opinions or related outlooks, as well as when having conversations with issuers. This top-level analysis could also provide long-term risk guidance, and flag the triggers that could alter the assumptions of the base-case scenario underpinning credit rating or outlook conclusions.

Increase outreach

CRAs have made great strides in expanding capacity, bolstering research and publishing notes that clarify how ESG factors have featured in their methodologies in recent years, particularly those with a global presence. Regional players are also making progress. Finally, new agencies – some of which are not regulated yet – now provide ESG-augmented analyses of creditworthiness. However, many investors are unaware of these developments. Therefore, CRAs should boost outreach and improve dissemination, so that investors use CRAs as well as other resources when assessing ESG factors in credit risk analysis.

Investors

Set up internal frameworks to systematically assess how ESG factors may affect credit risk analysis

This requires altering traditional credit risk models to reflect new data, the inclusion of new metrics in addition to traditional ones, a recalibration of weights and time horizon analysis. Some investors are already very advanced in this regard, but represent a minority.

Do not confuse the nature and purpose of credit ratings and ESG assessment services

Part two (p. 27-28) highlighted that there is considerable market confusion, particularly among FI investors, around the purpose of ESG consideration in credit ratings and the assessments made by specialised ESG service providers through ESG/sustainability scores. Credit analysts should use both tools to inform their views but appreciate that they are distinct products. They should think about what information included in ESG scores may be material to credit risk and over what time frame.

Be more proactive

Investors should be more inquisitive and take note of ESG-related research and commentaries issued by CRAs. They should engage more with CRAs and ESG service providers so that they are incentivised to enhance disclosure and improve their offerings. Finally, they should engage in public consultations or collaborative platforms to stay abreast of ESG policy initiatives, which are climbing up the agenda in several countries.

Below are more detailed emerging solutions, specific to each of the four action areas identified during the PRI forums as in need of further work. They are split between those aimed at improving the process and output of ESG consideration in credit risk analysis. As previously noted, market participants that have already demonstrated leadership in these areas should not rest on their laurels; as the ESG and regulatory landscapes evolve, credit risk assessments and pricing will need to be revaluated.

Download the report

-

Shifting perceptions: ESG, credit risk and ratings: part 3 - from disconnects to action areas

January 2019

ESG, credit risk and ratings: part 3 - from disconnects to action areas

- 1

- 2

- 3

- 4

- 5

Currently reading

Currently readingApplying theory to practice

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

- 14

- 15

- 16

- 17

- 18

- 19

- 20

- 21

- 22

- 23

- 24

- 25