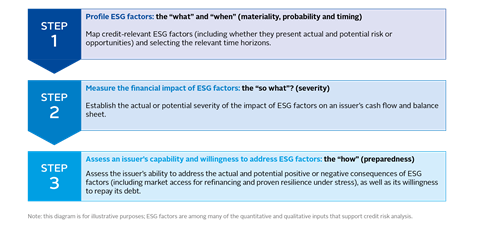

Roundtable discussions began considering the various steps that need to be taken to help build a more structured and systematic framework for ESG consideration in credit risk analysis. Three potentially significant steps have been identified so far.

Step 1: Profile ESG factors

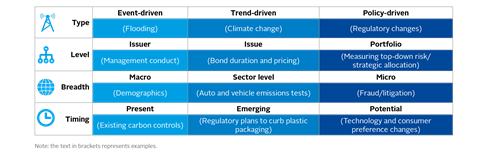

When it comes to risk profiling, credit practitioners have started to consider how to sharpen their focus on the different types of ESG factors to establish if they are relevant to credit and over what time horizon. Those listed below are a useful starting point for building a framework.

When it comes to assessing credit-relevant time horizons, it is worth establishing how visible the ESG factors are, how likely they are to materialise and how often, and, finally, their impact on creditworthiness, including the issuer’s balance sheet strength and whether, if possible, they have been mitigated.

Credit-relevant time horizons and “what if” analysis

There is no silver bullet to identify the time horizon over which to assess ESG factors in credit risk analysis. It depends on many factors, including whether analysis is conducted at the issuer level or at the issue level. For investors, it also depends on their investment strategies and objectives.

Part two highlighted that due to the multi-dimensional nature of ESG factors, difficulties in modelling non-financial factors and capturing data interdependencies were cited among the biggest obstacles to ESG consideration in credit risk analysis. Specifically, the interplay between the following factors was flagged as a major challenge: 1) long-term structural trends that tend to determine ESG risks; 2) the probability that ESG-related incidents will materialise and when; 3) the risk of these incidents reoccurring, and 4) their impact on an issuer’s credit fundamentals and its ability to adjust its business model by buying or selling companies and introducing or reacting to disruptive technology.

Scenario analysis emerged recurrently during the forums as a possible mechanism to make credit risk analysis more forward looking – not via long-term forecasts, but by considering how an issuing entity might perform in response to a range of hypothetical outcomes. It can help to assess the awareness of risks by bond issuers and their preparedness to address them. Importantly, it can highlight the causes that lead to specific outcomes. Part of the current popularity of scenario analysis is down to it being part of the Task Force on Climate-Related Financial Disclosures recommendations. New instruments to assess the exposure of financial portfolios to climate transition risk in multiple scenarios are also emerging9.

However, scenario analysis has its limitations when it comes to ascertaining plausibility (as this depends on how realistic the underlying assumptions are), as well as comparability and how many scenarios to consider overall.

There are other forms of “what-if” analysis, which can be helpful.

For example, sensitivity analysis would involve assessing the impact on the cash flow and balance sheet of an issuing entity of the change of a single ESG variable at a time (such as the cost of reducing CO2 emissions by different amounts). It can also be helpful to order the relevance of risks related to ESG factors. While estimates of sensitivities are not new to credit risk analysis, they are typically conducted through financial variables, as opposed to treating ESG factors as independent variables.

Stress testing, currently used in the financial sector for macroprudential oversight and to determine a bank’s capital requirements, can help to test an issuer’s cash flow and balance sheet resilience under one extreme scenario or a combination of severe scenarios, which are not necessarily correlated. It can therefore highlight vulnerabilities and help with planning.

All these types of analysis require quantitative skills as they often involve highly complex simulations. But they are becoming more manageable as analytical tools improve and models become more user-friendly. Analysis can be conducted by investors and CRAs, depending on their capabilities, or investors and CRAs can ask issuers if they use them as a tool to assess how aware they are of risks (and opportunities) and how prepared they are to address (or embrace) them. Either way, they can be useful to assess long-term risks, incorporate uncertainty, and focus on possible solutions to understand the implications of potential outcomes.

Step 2: Measure the financial impact of ESG factors

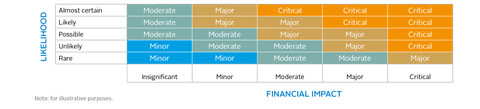

Once credit-relevant ESG factors and time horizons have been identified, another important step is to rank them in order of importance or urgency by linking an estimate of their severity to the probability of them materialising. Heat maps can be a useful synthetic indicator to prioritise material ESG factors and provide a relative assessment of their potential impact (in the form of risk or opportunity) (see below).

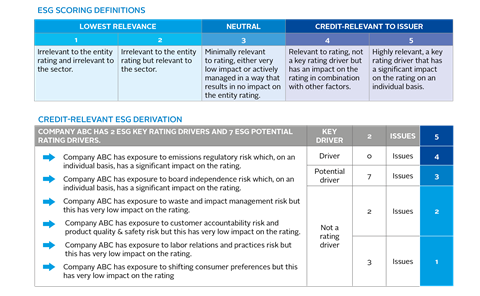

The example below shows how one CRA has started scoring and ranking ESG factors that play a role in its credit rating opinions (see below).

Step 3: Assess issuer capability and willingness

The final steps involve assessing an issuing entity’s awareness of ESG factors that may affect its credit quality and its ability and willingness to address them (see below). Evaluating this capability could be approached in numerous ways, including looking at how management has addressed the credit implications of ESG factors in the past (for example, recovery after a hurricane or adapting to a change in regulatory regime), or by conducting scenario analysis and stress tests. There could also be instances where ESG risks are visible but have no immediate impact on an issuer or issue, after the time frame and magnitude of these risks have been considered, relative to the underlying creditworthiness of the entity.

This is the stage where the analyst’s qualitative assessment has more of a role, focusing on management expertise, corporate culture, labour relations and factors such as reputation and intangible capital. It is also the phase where investors and CRAs (through engagement and outreach) can talk to issuers about ESG topics.

Download the report

-

Shifting perceptions: ESG, credit risk and ratings: part 3 - from disconnects to action areas

January 2019

ESG, credit risk and ratings: part 3 - from disconnects to action areas

- 1

- 2

- 3

- 4

Currently reading

Currently readingA transparent and systematic framework

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

- 14

- 15

- 16

- 17

- 18

- 19

- 20

- 21

- 22

- 23

- 24

- 25