How investors can manage ESG issues when analysing public companies and constructing listed equity portfolios.

Overview

- This introductory guide summarises how investors can manage environmental, social and governance (ESG) issues when analysing public companies and constructing listed equity portfolios.

- It introduces different investment approaches across the active-passive spectrum and the concept of stewardship in listed equities.

- For more information on anything in this guide, or on responsible investment more broadly, please get in touch ([email protected]).

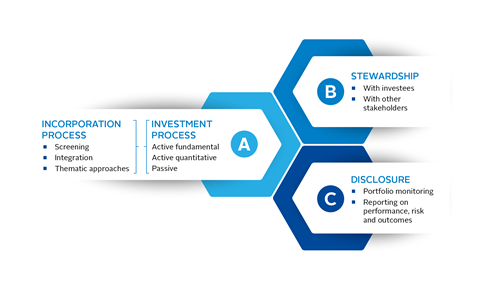

The guide is split into three sections:

The PRI defines responsible investment as a strategy and practice to incorporate ESG factors in investment decisions and active ownership. Responsible investing complements traditional financial analysis and portfolio construction techniques.

Responsible investors can have different objectives. Some focus exclusively on financial returns and consider ESG issues that could impact these. Others aim to generate financial returns and achieve positive outcomes for people and the planet, while avoiding negative ones. We are working with signatories to develop a framework to reflect these different approaches through Pathways.

Note on Pathways

It is clear from recent PRI signatory consultations that a growing number of signatories wish to advance their responsible investment practices in more relevant ways. In response we are developing Pathways, a framework that acknowledges the varied contexts in which signatories operate and allows them to differentiate their activities based on their duties and objectives. For more on this, please see below where we outline examples of how investor intent can influence investment practices in active fundamental, active quantitative and passive strategies, respectively.

A: Incorporation and investment process

Principle 1: We will incorporate ESG issues into investment analysis and decision-making processes

There is no one-size-fits-all approach to incorporating ESG issues into listed equity investment strategies. Approaches can include a combination of screening, integration and thematic approach based on the investor’s desired intent or to meet client or beneficiary preferences – such as risk-return profile, ethical considerations or to drive capital towards specific environmental and / or social goals. These approaches also apply to various investment strategies across the active-passive spectrum.

Table 1: Strategies across the active-passive spectrum

| Investment strategy | |||

|---|---|---|---|

|

Incorporation methods |

Active fundamental strategies |

Active quantitative strategies |

Passive investing |

|

Screening |

Application of rules based on defined ESG criteria that determine whether investments are permitted in a portfolio. Rules can be:

|

||

|

ESG integration |

Material ESG issues are identified and analysed as part of fundamental analysis, forecasting, valuation and portfolio construction. Includes assessing how the issuer manages ESG risks and opportunities.

|

ESG factors can be integrated into quantitative investment strategies. ESG factors can be built into the design of factors or can be added to and used alongside other ‘traditional’ factors such as value, quality, size or momentum. |

Investors can select ESG-focused or ‘sustainable’ benchmarks. Alternatively, custom benchmarks can be created by applying selection and weighting criteria to reflect client objectives. |

|

Thematic approaches |

The screening and integration process is used to identify and analyse companies and build portfolios that provide exposure to particular sustainability themes while meeting reward, risk and, where relevant, outcomes criteria. |

The screening process identifies companies with exposure to a desired theme, alongside other desirable factors. The portfolio is then constructed using pre-determined rules reflecting objectives and risk constraints. |

Indices are chosen or constructed to reflect a particular environmental or social theme, such as clean technology or microfinance. |

PRI resources

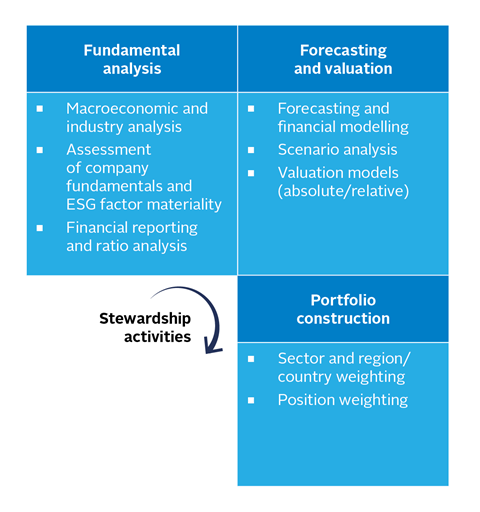

Active fundamental strategies

Fundamental analysis, forecasting and valuation

In active fundamental strategies, analysts or portfolio managers identify and assess issuers’ material ESG risks and opportunities, as well as how they relate to the wider sector and broader economy. This research complements assessment of the company’s competitive position and financial performance. A wide range of information can be used to analyse each issuer, including the company’s disclosures of financial and sustainability information, data and analysis from external sources as well as techniques such as machine learning and artificial intelligence to utilise unstructured data.

Having carried out fundamental analysis of the economic environment, the industry and the company, the investor will make forecasts of the company’s prospects, profitability and cash flow scenarios. In turn, this forecast will then be used in valuation models to estimate the companies’ intrinsic value.

Investors may use probability-weighted estimates of the financial costs of ESG risks being realised.

Various tools can help investors to understand the likelihood of different future scenarios and the extent of the impact of each scenario on individual issuers. Valuation models, such as those based on present values of future cash flows or dividends, or those based on valuation multiples, can be adjusted to reflect ESG factors.

Portfolio construction and stewardship

While the portfolio construction process and position sizing decisions are unique to each institution, the issues to consider include aggregate portfolio risk / return and ESG metrics, style factors and alignment with portfolio mandate.

Research findings can help managers to identify and prioritise stewardship activities, such as voting and engagement, on material issues with portfolio holdings.

Figure 1: Active fundamental investment process: a summary

How investor intent can influence integration practices: An active fundamental scenario

An analyst at an asset management firm is considering recommending purchasing shares in an industrial company. Through the manufacturing process, the company emits significant levels of greenhouse gases. The analyst believes the company has adequately managed material ESG related risks, has credible future decarbonisation plans and is in a good position to cover the cost of GHG emission permits. She is confident material ESG risks and opportunities are reflected in her financial forecasts that underpin the valuation model. The intrinsic value calculation suggests there is meaningful upside to the share price.

See below for how the investment team may act next depending on their intent.

|

Incorporating ESG factors |

The investment committee reviews the investment rationale. Assuming no better investment opportunities are available, the investment committee approves adding the stock to the portfolio. |

|

Addressing drivers of systemic risks |

The investment committee reviews the investment rationale and the impact of the potential purchase on the sustainability outcomes of the portfolio, namely compliance with the asset manager’s netzero commitment. Assuming no better investment opportunities are available, the committee approves adding the stock to the portfolio. |

|

Pursuing sustainability impact |

The team responsible for managing impact strategies ensures that the due diligence phase considers whether the investment meets eligibility and strategic alignment criteria. Focusing on the company’s product output, if the team fails to identify any meaningful positive impact on an environmental or social challenge, the stock is not added to the portfolio. |

Active quantitative strategies

Strategy design, testing and evaluation

ESG issues can be incorporated into quantitative, rules-based multi-factor strategies as factors, or characteristics. These factors are based on empirical evidence and statistical analysis, and can make use of a growing amount of ESG-related data.

Some investors have started to include ESG factors such as greenhouse gas emissions alongside more traditional factors, such as value, size and momentum. Other investors have been enhancing the design of the quality factor by incorporating issuers’ social or reputation characteristics. Strategies should be and typically are back-tested, or Monte Carlo simulations are performed, to ensure the strategies would have delivered the desired results (usually in the form of risk-adjusted returns) in the past or in simulated future scenarios.

Portfolio construction

The first stage in portfolio construction is often introducing constraints or screens, such as ensuring a company receives a minimum score on a range of ESG factors. Optimisation techniques can be used to enhance the portfolios’ ESG risk profiles. Once the strategy is launched, the rules-based strategies run automatically, rebalancing the portfolio in regular intervals.

Figure 2: Active quantitative investment process: a summary

How investor intent can influence integration practices: An active quantitative scenario

A quantitative equity investment team is managing multi-factor strategies to maximise portfolios’ Sharpe ratio. They have found a statistical relationship between listed companies’ employee satisfaction rates and the companies’ share price performance. They are looking to incorporate such financially material factor into an existing ‘quality’ factor that has been based on measures of issuer profitability and earnings volatility. The enhanced quality factor would then feature in the multi-factor strategy alongside the other traditional factors. The team then backtest the redesigned multi-factor strategy.

See below for how the investment team may act next depending on their intent.

|

Incorporating ESG factors |

Following successful back-testing, the asset manager adapts the existing multi-factor strategy. |

|

Addressing drivers of systemic risks |

The firm is committed to net-zero targets across all portfolios, and the revised strategy design reflects this commitment. Having incorporated such constraints into the revised strategy design, backtesting shows if the strategy meets risk-return expectations and netzero commitments. If successful, the strategy will be adopted. |

|

Pursuing sustainability impact |

The firm seeks to make a positive contribution to social impacts; however, using active quantitative investment processes to achieve positive measurable impact is likely to be challenging. The firm could manage its exposure to sustainability outcomes by adapting the systematic strategy to select securities by companies that meet desired employee satisfaction rates. The selected securities may also be checked for relevant negative impacts and complementary stewardship actions may be considered. |

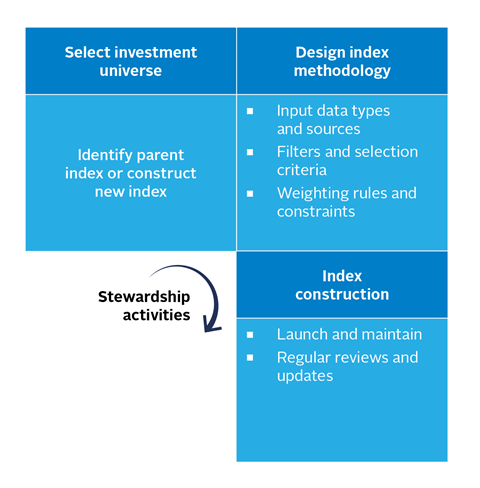

Passive strategies

Selecting an investment universe

Passive strategies in responsible investing involve choosing an existing (ESG) index or designing a new custom index with desired ESG characteristics. This decision is normally undertaken by the asset owner or adviser and will depend on client expectations in terms of including ESG factors and portfolio risk-return expectations. Available index choices have increased dramatically over recent years, from climate-aligned and thematic-focused benchmarks to those using ESG scores to rank constituent companies.

Designing and constructing an index

Constructing a new index can start from an existing ‘parent’ index to which the investor applies exclusions or a ‘tilting’ process to increase or reduce particular exposures. Alternatively, one can construct a new index by determining the starting investment universe, deciding on sources and types of data, and applying weighting techniques.

Figure 3: Passive index design

The approach that is selected from the investment strategies laid out above should be informed by the investor’s intent and expectations.

How investor intent can influence integration practices: A passive scenario

An asset owner’s investment committee allocates part of its public equity investments to passive strategies. The organisation wishes to invest globally and in line with its responsible investment policies, which state that exposure to certain sectors or industrial activities must be avoided, especially with regard to climate transition risk.

See below for how the asset owner may act next depending on their intent.

|

Incorporating ESG factors |

The asset owner identifies an ESG index that aligns with specified criteria and the required exposure to global equities. If no suitable index is available, the asset owner engages an asset manager or index provider to design a suitable benchmark. |

|

Addressing drivers of systemic risks |

The asset owner identifies a relevant ESG index that provides exposure to global equities, excludes certain exposures or sectors and helps meet the firm’s commitment to short, medium and long-term net-zero targets. If such an index is found, an asset manager with index replication capability is appointed. If no suitable index is available, the asset owner engages an asset manager or index provider to design a benchmark that meets the desired characteristics. |

|

Pursuing sustainability impact |

Achieving positive impact relating to the climate transition is likely to be challenging under a passive strategy. The investment team may improve its exposure to positive climate outcomes by allocating to or constructing an index whose constituents are companies offering products or services that support clean power or apply renewable technologies to other industries while avoiding negative outcomes. Such an index may differ significantly from mainstream indices in terms of its return, volatility, degree of diversification and factor exposures. The investor may also pursue a well-resourced stewardship strategy to support positive outcomes. |

Table 2: Examples of PRI signatories’ approaches to ESG Integration: Robeco and Invesco

|

Active fundamental approach – Robeco Source: Sustainability integration – Approach and Guidelines 2023 |

The ESG integration process follows a three-step approach: Step 1: Identify relevant factors that differ per industry and are based on materiality research of the sustainability research team. Next to financially material issues, impact material issues like climate change strategy and contribution to the Sustainable Development Goals can also be considered. Step 2: Using several sources (mostly developed in-house) the financial analyst assesses the impact of the material ESG factors on the business model and value drivers of the company. Step 3: The fundamental equity teams quantify the impact of the company’s ESG performance on material issues. They will adjust the business drivers: sales growth, margins, risk, capex and competitive advantage period in their models. In this way the ESG analysis is explicitly incorporated in the valuation of the company. |

|

Active quantitative investing – Invesco |

Invesco’s quant team has developed an approach based on the thesis that material ESG-related risks and opportunities will impact equity valuations. Their in-depth systematic analysis and portfolio construction capture that thesis while optimising the risk and return profile and reducing carbon intensity. Companies with controversial business areas and negative ESG momentum are excluded from the investable universe. The strategies also apply a best-in-class approach based on a scoring system to assess a company’s energy transition measures and only consider those that actively commit to making a positive impact on climate change. ‘Quality’ factors that have a direct link with governance and help identify companies with the potential to outperform their peers are also included. Excluded stocks with attractive quality and value characteristics are replaced by a mix of assets with similar factor exposures from other sectors. |

B: Stewardship

Principle 2: We will be active owners and incorporate ESG issues into our ownership policies and practices

We define stewardship as the use of influence by investors to protect and enhance overall long-term value, including the value of common economic, social and environmental assets, on which returns and client and beneficiary interests depend.

Stewardship can be conducted by listed equity investors across a range of active, quant and passive investment strategies but options and tools will vary depending on the strategy. The drivers for investors to undertake stewardship activities include:

- better managing material ESG-related risks by issuers;

- improving issuer disclosure on ESG issues;

- meeting client expectations such as net-zero targets; and

- improving issuer practices to promote financial or non-financial objectives.

Academic research commissioned by the PRI shows that successful engagement can contribute to better corporate financial performance, improved shareholder returns and strengthened relationships between investors and companies.

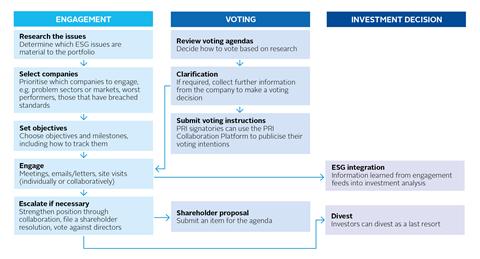

Investors can use their position (and associated legal rights) as partial owners of listed companies to influence corporate practices. Engagement with investees is one mechanism of fulfilling stewardships commitments.

Engagement activities are often based around interactions and dialogue between an investor, or their service provider, and a current or potential issuer. This might also extend to a non-issuer stakeholder such as a regulator. The ultimate objective of either activity may be to improve practice managing ESG-related risks, progress on sustainability outcomes or improve public disclosure.

For listed equity investors, engagement typically involves communication with the issuers, dialogue at the company AGM or other shareholder meetings, such as earnings calls or roadshows, as well as (proxy) voting decisions and filing or supporting shareholder resolutions. Investors can also escalate stewardship activity when initial efforts are unsuccessful by, for example, divesting selected issuers or taking legal action against the company or its board.

Figure 4: Interaction between engagement, voting and investment decision

Proxy voting

Voting on agenda items at annual general meetings (AGMs) is a core engagement tool for listed equity investors. Company boards will typically propose a set of resolutions to the AGM, including director nomination, approval of accounts, and remuneration. Investors concerned about the management of specific ESG issues may look to:

- vote against re-electing a specific director due to mismanagement of ESG issues, for example, voting against re-electing the chair if board diversity targets are not met;

- nominate alternative director candidates for election; and / or

- propose shareholder resolutions on ESG-related issues.

The voting process involves: setting policy to outline voting objectives on issues such as board independence, remuneration etc; conducting research to inform voting decisions; and communicating reasoning and justification with investee companies before and after the AGM. Public reporting of voting decisions is also common, for example through the PRI Resolution Database.

Many investors outsource parts of or the entire voting process. Outsourcing may be especially important for investors with large, diverse portfolios in multiple geographies. However, it is considered better practice for responsible investors to make their own well-informed voting decisions rather than automatically accepting recommendations from advisers.

PRI resources

C: Disclosure

Principle 6: We will each report on our activities and progress towards implementing the Principles

Portfolio monitoring

Investment managers monitor their portfolios to ensure the strategies follow the intended objectives and comply with constraints and requirements agreed with clients or set by regulators.

This monitoring may include ensuring, and reporting on, compliance with screening rules. It may also include measuring and reporting portfolio metrics, such as exposure to climate-related risk.

Investors also analyse their investment decisions to see how they have performed and how they fulfil responsible investment commitments.

Reporting on risk, performance and outcomes

It is important to report on portfolio positioning, risk / returns and, where relevant, outcomes: clients want to see this information and investors can thereby demonstrate how effective their responsible investment policies are.

Client and stakeholder reporting is often governed by regulation in certain jurisdictions, particularly for retail financial products. In recent years, there has been an emergence of rulebooks governing whole classes of investment products wishing to market themselves under green, sustainable or ESG labels. The EU’s Sustainable Finance Disclosure Regulation and Sustainable Finance Taxonomy require particularly detailed disclosures of ESG data to clients.

The CFA Global ESG Disclosure Standards for Investment Products are the first global voluntary standards for disclosing how an investment product considers ESG issues in its objectives, investment strategy, and stewardship activities.

Downloads

An introduction to responsible investment: Listed equity

PDF, Size 1.08 mb